FOMC, The War & The China Play

How Monetary Policy, Geopolitical Risk & Strategic Rivalry Are Reshaping the Global Macro Landscape

I want to start by speaking a little on the geopolitical issues, that I have laid theses out for across the last 2 weeks now, see both reports below directly connected to US-iran and oil situation:

The ongoing war

I think the most interesting part about the position equities, rates & FX are in right now is the fact that even as we get headlines and progressions on tensions BUILDING (e.g. more strikes on embassys etc), we’re having less of a downside in equities, less of an upside in rates and less of an upside in the dollar, it just shows me that we’re at an extreme in price and for any leg lower there’d need to be even more of an extreme that isn’t yet priced (e.g. other countries involved heavily, heavily more attacks etc).

For example, these types of headlines below were creating outsized moves in the first few days of the war, but like anything, the market begins moving to an extreme and pricing the most extreme scenario.

I like monitoring the reaction and cross asset correlations as we trade through these headlines/events/catalysts because it gives you an idea of exactly what is being priced. The last thing you want to start doing is taking bets on what’s already priced (e.g., if you’re going to bet on a continuation of this US-Iran war, you could probably be flushed out UNLESS there’s an extreme because we’ve already priced this)

This was the headline:

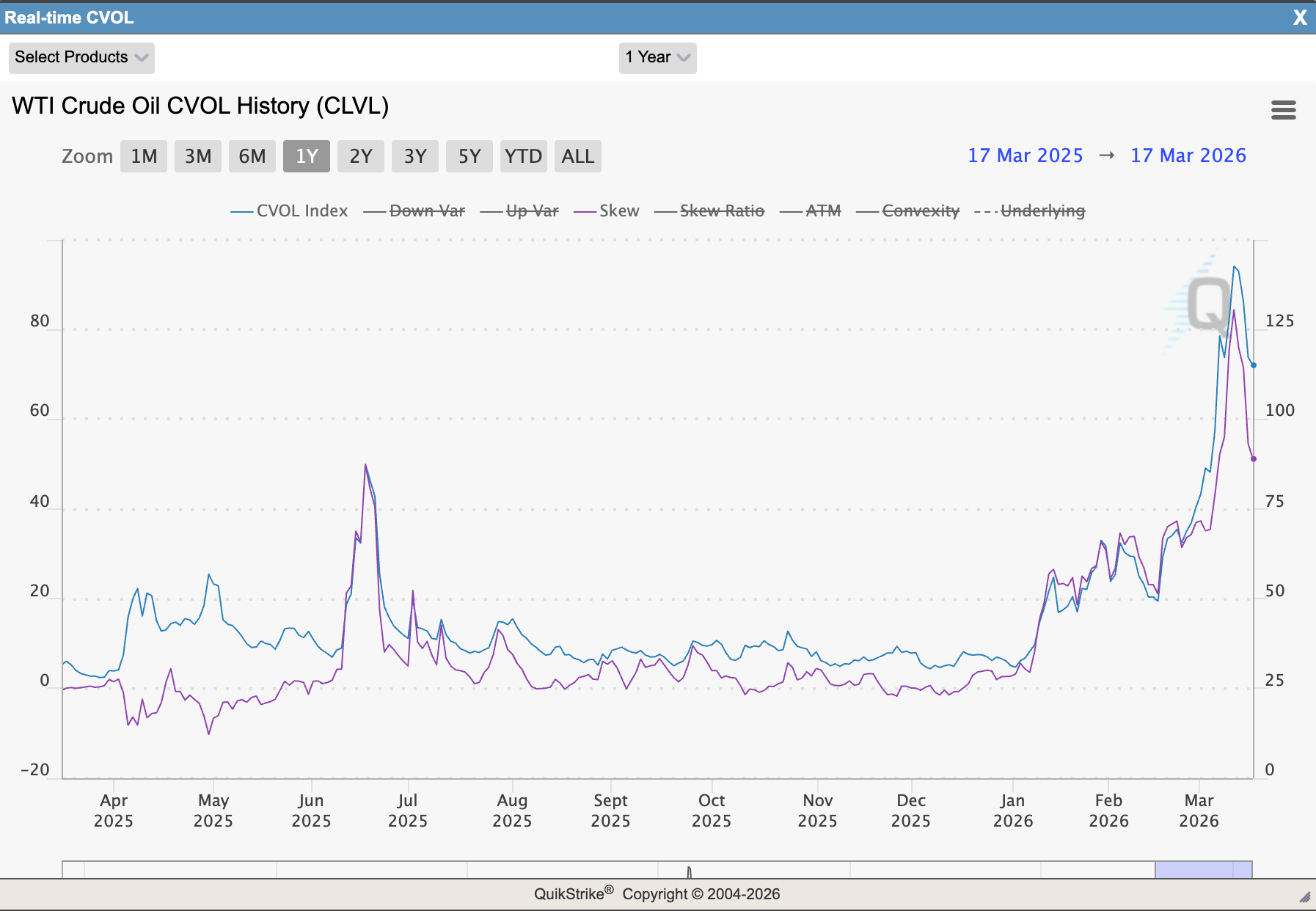

Oil, which has been the main component that has caused outsized moves in equities, rates & FX, now looks to have created a top in implied vol as skew is rolling over. If oil continues to trade at these extremes as vol drops significantly, its the market accepting this price as the new reality for oil but what is key to watch is that if a de-escalation happens (likely in my view), then there will be outsized moves in oil relative to other markets.

Edge is most found when you see dislocations in correlations, right now we've seen implied vol move in lockstep with oil, but as implied vol has ticked down we haven't seen oil prices move lower to the same degree (dislocation). Basically, if you take the other side of this dislocation (e.g. being short oil), then the move lower will be asymmetric IF oil re-correlates with implied vol. I'm also not saying its time to be short oil, I don't necessarily have an edge there but I definitely WOULDN'T be long.

I think if oil stays above $90 as implied vol and skew normalises without any breaks, I’d be worried because that means oil is trading on markets implied pricing rather than a geopolitical premium. Same for equities, if we start seeing vol drop massively and a de-escalation in the war with no meaningful upside, I’d definitely be closing the long exposure I have (which is in NQ right now, also laid that out in those previous reports tagged at the top).

By no means would I ever base a thesis on historical data, I think that’s a massive limiting factor and doesn’t provide any context, but I think its very interesting that when you run a historical test on the S&P price action in the following 1D, 5D, 1W and 1M after conflicts, has been an extremely positive outcome. Initial reaction is mixed: 6/10 conflicts positive 1D (avg 0.22%). But the 1m outcome is historically constructive: 9/10 positive (avg 4.29%). It seems like markets tend to look through geopolitical noise within 3-4 weeks. The only caveat was the Soleimani 2M (-8.68%) is distorted by COVID-19 rather than the strike.

It’d be unwise to assume that there isn’t also moving parts UNDERNEATH the surface of this war. Moving parts as in, the US gaining leverage to global partners, think just how Trump used tariffs as a direct negotiation tool, this is more indirect and he understands the power the US can hold by proxy in this US-Iran war. Do I think he’s bombing Iran ONLY for the sake of these underlying power gains? No, but it sure plays a part.

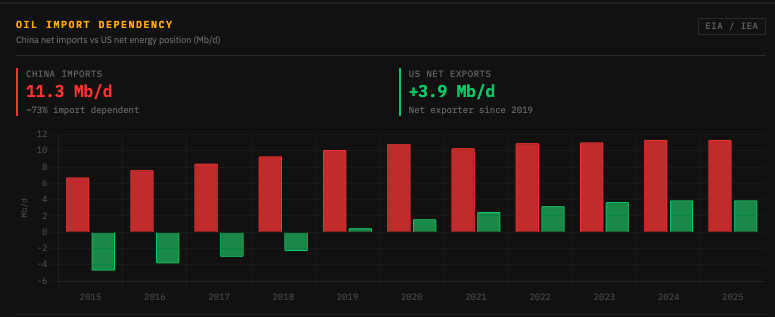

I’d say it’s the most significant leverage plays the US has had over China in years (tariffs were tit for tat, China can’t respond here). Hormuz carries roughly 20% of global oil supply and with it effectively closed right now, China, the world’s biggest oil importer, is taking a SERIOUS economic hit. The US doesn’t have that problem, it’s mostly energy independent and absorbs this far better than Beijing can.

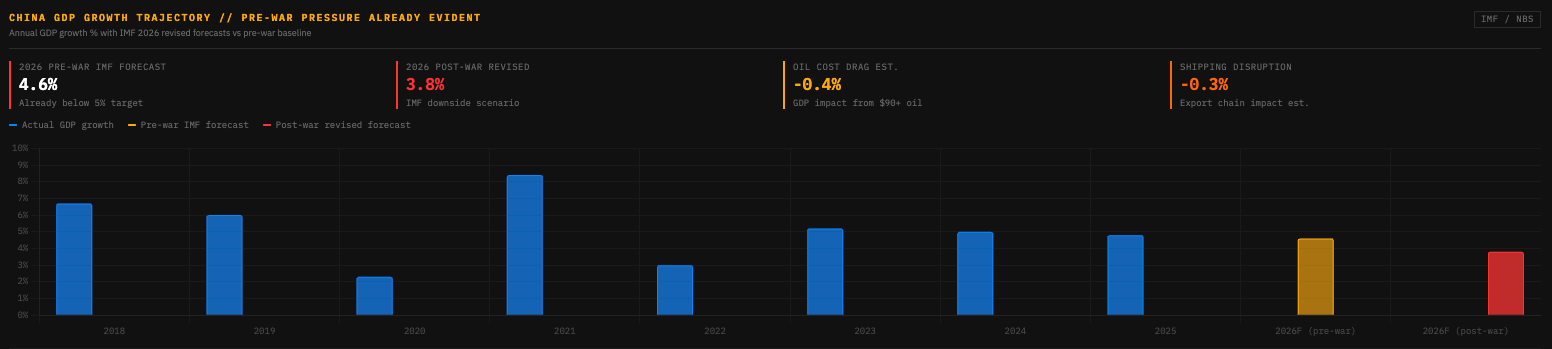

What people are missing is that Iran was one of China’s most important non-Western partners. The US has essentially neutralised one of Beijing’s most important geopolitical functions in the region. We also must remember there is a lot that goes UNSEEN. Just because Trump is explicit in his actions, doesn’t mean that there isn’t deals/negotiations going on behind closed doors, I seriously do think there’s some type of deal he could be trying to strike with China during this time, especially when China’s growth has been DOWNGRADED as a direct result of the war.

Whether you think that’s justified or not, Beijing is watching VERY closely, especially with Taiwan always in the background. China simply cannot afford to test the US right now while it is in a hot war and clearly willing to act. Trump even pushed back the Xi meeting because of the conflict, which is a pretty clear signal that China’s cooperation is something the US expects. Every week this drags on is another week of economic pain for an economy that was already under pressure domestically, with Gulf shipping disrupted and China’s export chains running right through that region.

It also seems pretty consistent that the dollar actually weakens after these types of conflicts (once again, I’d NOT recommend using history as your sole thesis)

Why does that matter? If the Trump administration can directly make the USD weaker, they are gaining another advantage in the power play of exports against China (making exports cheaper so gaining some leverage over China).

FOMC

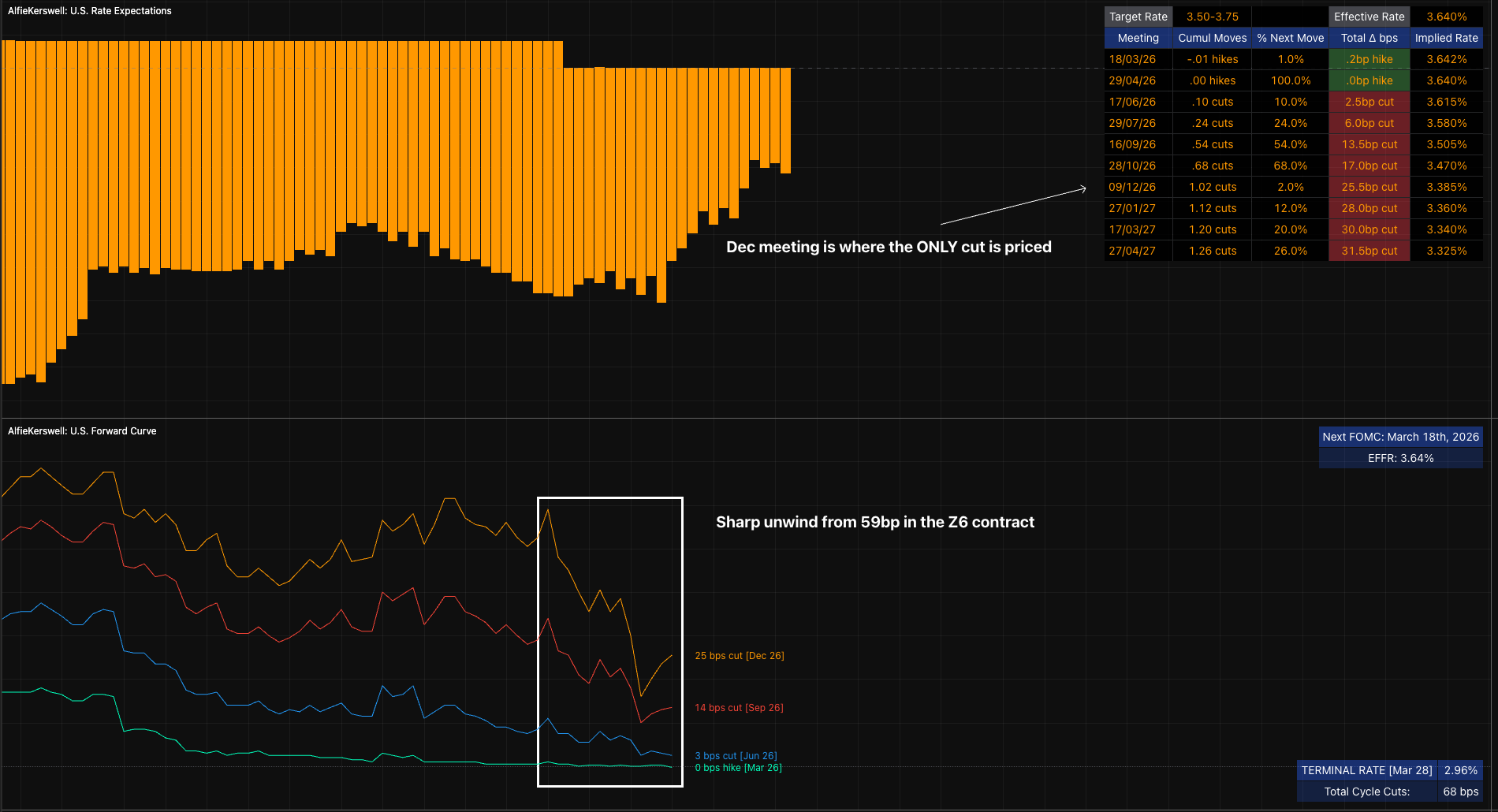

Now there’s two catalysts that can DIRECTLY unwind positioning in FX, rates and equities which is now what I’m shifting my focus on. Which is 1) news about a de-escalation/the war is over from US/Israel/Iran with a potential deal between them. 2) the FOMC meeting today. Now the outcome is already SEEN and known for the meeting, we’re likely to get a pause and that’s not where my focus is given the pricing. If I’m currently taking the other side of market pricing (e.g. I’m long NQ as geopolitical issues are apparent), then I want to see the Fed’s stance also take the other side of market pricing.. but what does that look like?

If Powell comes out and identifies this spike in oil as transitory and that he is not worried, there could be massive shifts in positioning and the function that begins this would be in rates as the curve likely reprices in 10-15bp+ initially and adds as the weeks go on.

The reason I like this view as being the one that unwinds positioning is because I think even if Powell comes out saying that the rise in oil prices could transmit into the economy and that inflationary pressures are a massive worry…. I don’t think that shifts much in rates (and therefore equities and FX), simply because I believe this extreme is already priced. Now the only rhetoric that would swing rates higher, equities lower and the dollar another leg higher would be if Powell comes out so aggressively saying they expect hikes this year, maybe mentions their base case is 1-2 hikes this year.. but I mean, how likely is that scenario? Very unlikely, I’m happy to take the other side of that given the extreme of the forward curve right now:

The reason I say this is unlikely because what sense would it make to hike or keep rates here for the rest of the year given the slowdown we’ve seen in the labor market, considering that there’s a likely probability that oil prices unwind (based upon de-escalation and Trump’s goal to drive oil prices lower). So in my view, IF the FOMC speech is going to be a catalyst for equities to go higher and rates to go lower, Powell would likely need to signal the fact that oil prices are transitory.

People will probably say that the base case is for Powell to sit on the fence and say this could transmit etc, but that still wouldn’t cause downside in equities, and if it doesn’t cause downside in equities then implied vol will probably unwind as hedges close, so that makes it implicitly bullish equities. If he takes the other stance and says oil could transmit into inflation, that still doesn’t give the hawks a new catalyst, and if there’s no new catalyst for downside = vol unwinds = implicitly bullish equities. The bar to be more bearish than current positioning is already extremely high.

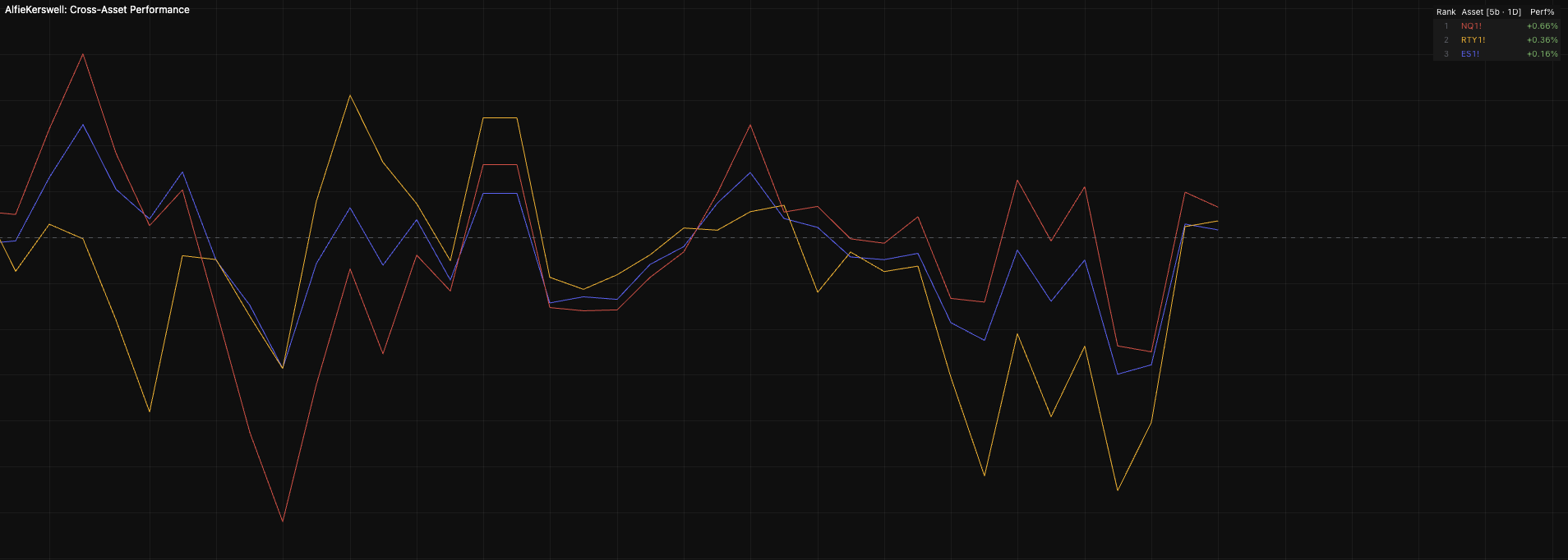

The unwind is already partially being seen in US equities, but I think it could unwind WAY faster. If there were some type of imminent threat or major escalation that everyone was hedging for, NQ wouldn’t be outperforming the S&P on an outright basis across the last 5 trading days. As usual, if an extreme is priced, we now need to be SHOCKED for markets to even move. A shock in this instance can come from two inputs discussed above, yet both are highly unlikely.

So on the assumption that the war is at its extreme (not saying it is, just laying a thesis), then the focus shifts back to the domestic setup, which has mostly been centred on growth, which in my view is not in a position where we're going to see a massive downturn/recession (all these ideas suporting a recession are blown way out of proportion given that everyone is ONLY focusing on NFP). I'm not discounting the importance of NFP but I will say that the economy can likely operate effectively and grow even without massive amounts of jobs being added, so until we see noticeable shifts in real consumer spending, I'm really not worried about growth here and I think it's likely that the Fed cuts twice this year, and we will start normalising in NFP figures (or at least stop this level of slowdown).

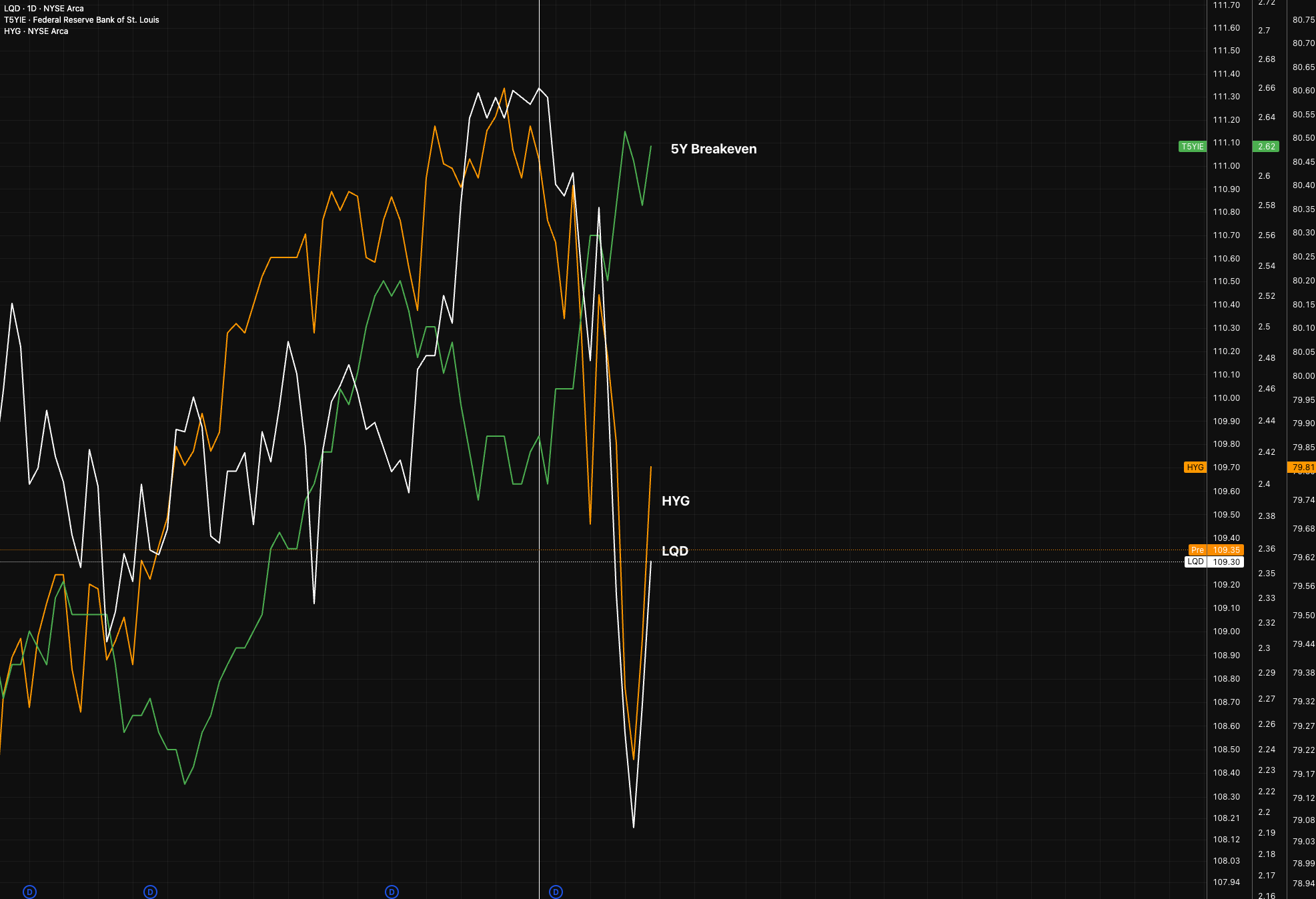

The most likely curve regime we'd see if we were heading into a recession or growth scare would be bull steepening as credit spreads would be compressing directly in line with lower growth prints, which is NOT happening. The only compression we're seeing in credit spreads is directly from breakevens/the tail-risk to inflation through the energy component. That means if there is de-escalation (and oil starts moving lower), then breakevens will likely start ticking DOWN and credit spreads tighten with momentum, which will give upside to equities as credit spreads is one input into the equity return picture (NOT the full picture).

Thanks

Alfie

Alfie

What's Your take on FOMC