Navigating Long US Equities Amid Persistent Geopolitical Tensions

Why the Risk Premium Creates the Opportunity... Eventually

First thing I want to lay out is that today’s inflation print was never going to be the catalyst. Not for rates, equities, or FX. All eyes are on geopolitical tensions, and until there's clarity there, the market couldn't care less that inflation is moving lower on a 3m and 6m speed basis. What it does care about is how the energy component transmits into the upcoming MoM and YoY prints, and how that ripples through the broader economy.

Posted about this on X. The core idea is simple.. find the underlying drivers of FX, equities and rates, then tie them to what catalysts could confirm or shift the view. If everything is currently tethered to geopolitics, a CPI print is noise. The upside macro foundations are blocked by oil-driven rate repricing until war clarity emerges.

See my recent report on the macro regime as I am building on these ideas:

The question worth asking is, what if the oil shock ISN’T transient? If oil stays elevated for 6+ months, the Fed's reaction function potentially stops cuts, or pushes terminal rate expectations even further out (both highly unlikely, but possible).

That’s the scenario the market is beginning to price. And it’s the scenario that’s driving every cross-asset move you’re seeing right now.

Even with labor continuing to soften, growth, inflation and liquidity are sitting in a place that structurally gives upside in equities, downside in the dollar, and ranged bond price action (upside at best). Duration risk is the only reason I wouldn’t say bonds are firmly skewed higher from here.

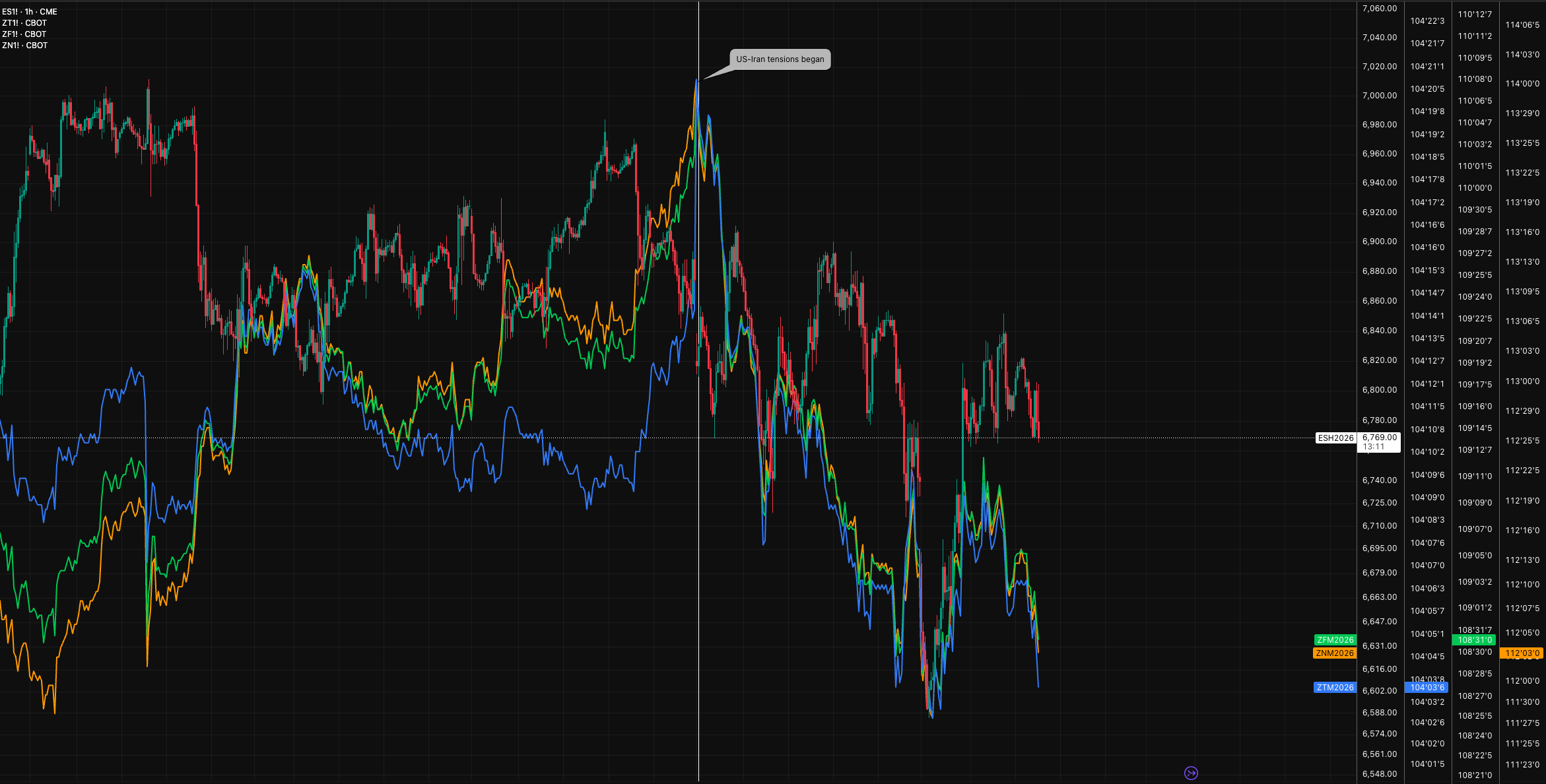

What matters for getting long the index is whether the underlying drivers unwind or persist, and that depends entirely on the correlation structure. If the driver is war > oil prices > equity vol, in that order, then everything is directly connected to how the war develops. Right now we’re seeing bonds move in lockstep with equities, both lower. That matters, because it CONFIRMS this move is macro-driven. This is the reflation story driven DIRECTLY by the rise in oil prices.

To be long the index, I want to see a break in the bonds/equities lockstep lower. Right now it’s confirming oil-rate transmission dominance. I want to see equities outperform bonds on cross-sectional momentum.

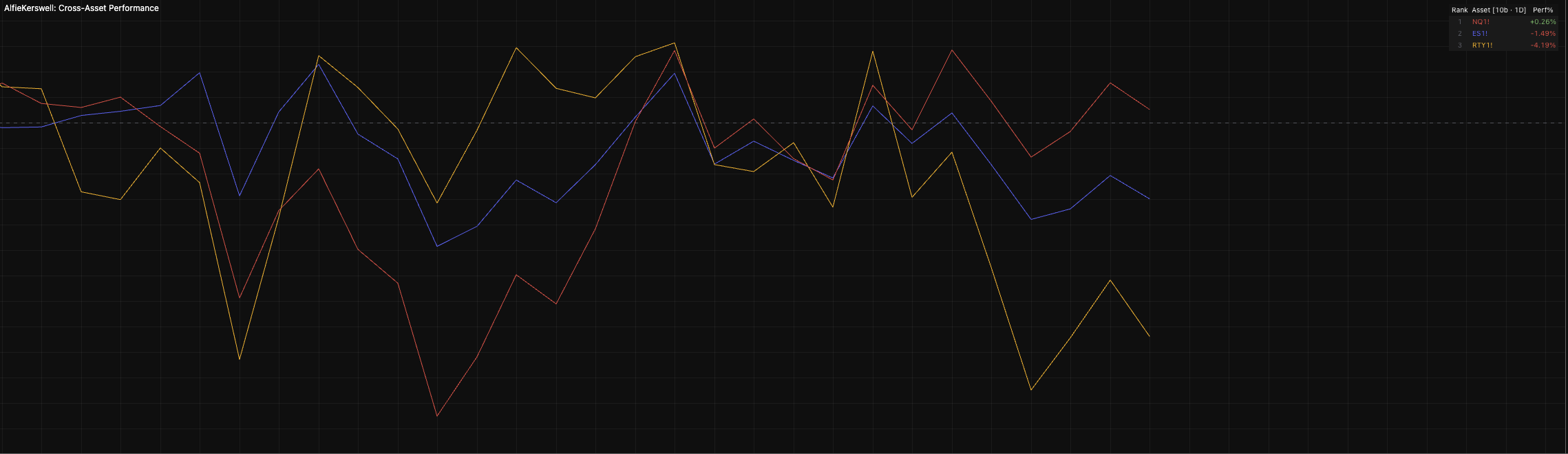

Just another key note.. if this were a growth shock, we would NOT be seeing NQ outperform ES on a 10d lookback. NQ is arguably the most sensitive index to inflationary pressures and Fed repricing. If growth were that much of an issue, and this inflationary tail risk persists, we would be seeing ES > NQ > RTY leadership in that order, with all indexes returning massively negative over the past two weeks, but we're not seeing that.

Bonds and equities moving together confirms it's a rate repricing event sourced from oil (which is sourced from geopolitics). So the question becomes: if oil/war is the single function controlling rates, and rates are the mechanism transmitting through to equities, what do I need to see to get long the index when the macro regime is otherwise supportive?

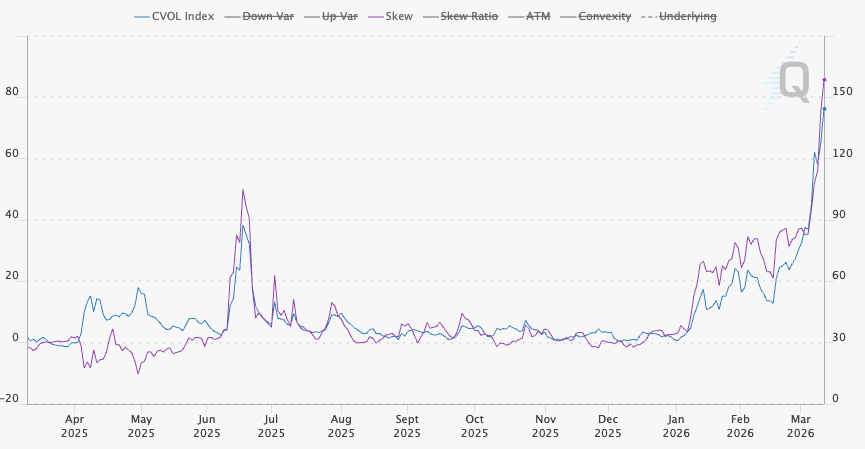

Firstly, oil needs to form a top in both skew and implied vol. That's the direct function controlling rates moves, which is transmitting through to FX and equities. For every tick higher in oil vol and upside skew, we've seen downside pressure in bonds and equities as the dollar trades higher on STIR repricing. Long entry in the index requires oil stabilisation confirming reflation peak, oil staying below $80, and a decline in both front-end rate vol and crude futures vol. The correlation intensity between those two (front-end & crude vol) is what confirms transmission persistence.

Oil headlines now have MORE sensitivity to rates than they did two weeks ago. The OPEC+ production decision Sunday is partly in my focus. A production increase shows a supply response to the war premium, then crude falls marginally and lowers the impact of the inflation transmission chain. But the danger is that they release more supply in response to the war, the war premium gets added straight back a day or so later, and whatever OPEC just did is immediately mitigated.

Duration sensitivity magnifies the rate lockstep we're seeing, but positive growth and liquidity conditions are the offset, if oil lets them breathe. If NQ begins to outperform ES, that's evidence the market is starting to look past duration sensitivity and the oil transmission story (we’re already seeing this).

The front-end is anchored by softening labor. The oil spike forces hawkish repricing risk in near-dated cuts, which is why the range will likely persist until war and oil resolve the inflation transmission path. ZF has the highest risk/reward once (and if) the war fades before growth deteriorates further, in my view. The belly could reflect labor softening while avoiding duration risk, especially if the oil repricing is already reflected in the curve by then. I'm not in that trade yet. I have no informational edge on geopolitical timing, and I won't front-run it.

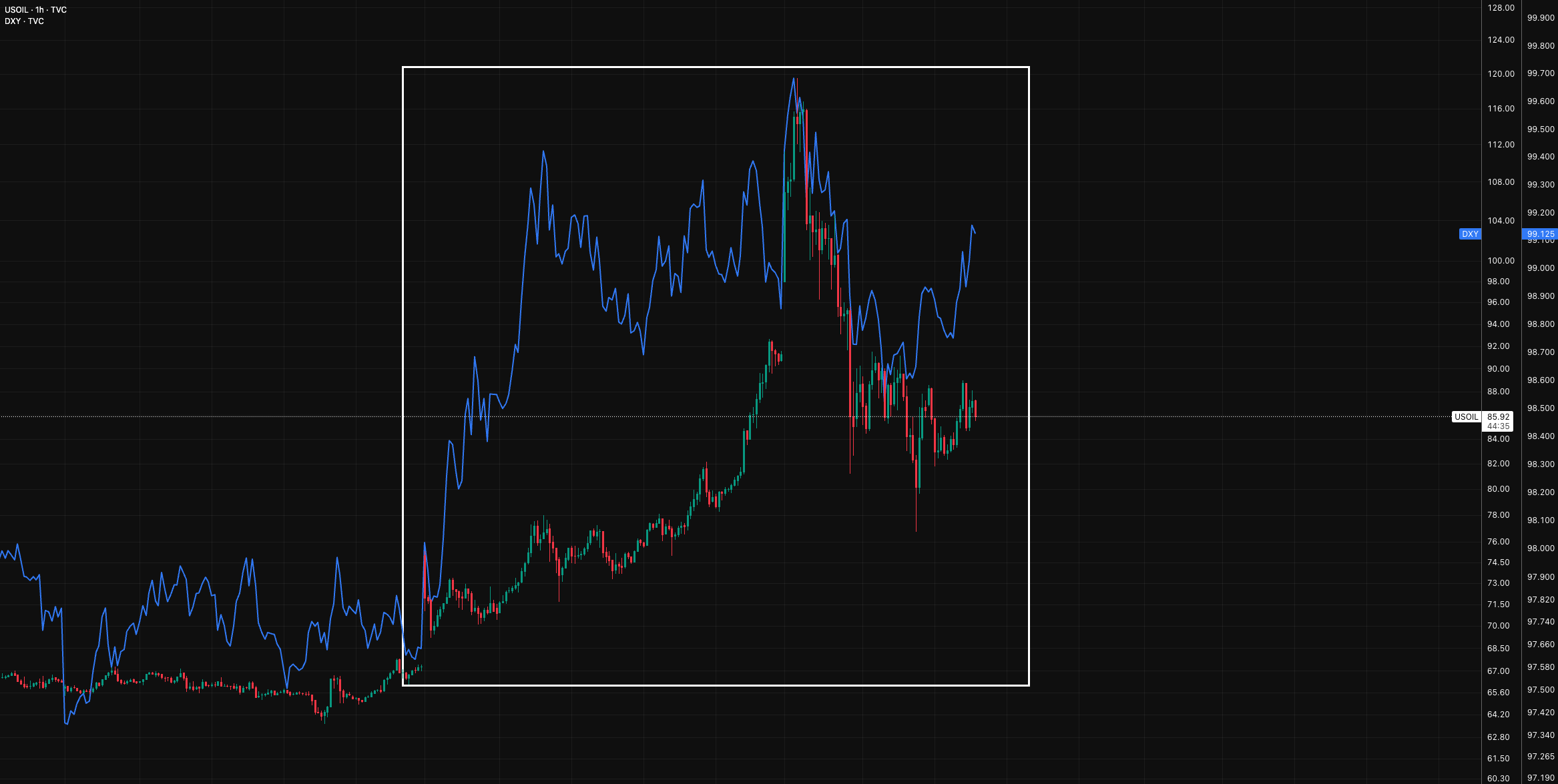

The dollar has moved in lockstep with the blowout in oil prices. The first thing I want to see break when the index bottoms is the dollar-oil positive relationship fracture. I want to see both trade lower, but with the oil move carrying more momentum than the dollar. Equal magnitude dollar weakness isn't that posiitve for equities in my view. An outsized dollar selloff is actually a risk, foreign capital repatriation at pace would send the index lower (I also don’t think this is likely, but possible if the dollar moves lower at speed). The structural disinflation story should overwhelm the transient energy shock bid in time, if geopolitical issues wrap up soon.

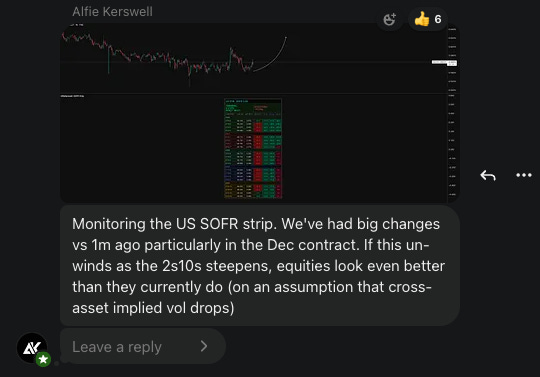

Another KEY show of hand will be if/when SOFR reprices. Front-end rates normalise back toward the cuts that were priced in Dec 26 prior to this blowout (around 60bp, the 2-3 cuts range). Terminal rate has moved to Z7, I want to see it backtrack toward the June-Sept 27 range to show real normalisation.

I hate to be a central bank speech watcher.. BUT Fed speech that dismisses the oil spike as transient while emphasising labor softening could be a catalyst to reprice SOFR. It likely creates a bottom in the forward curves, likely a top in the dollar, and firms the picture for being long the index (if war and oil prices have also deescalated to the point where implied vol in both drops).

We’re not in a regime where the Fed has direct control over where rates land (in my view), I think the market has forced their hand repeatedly across the last 6-12 months. Even knowing the equity blowout is war-driven, the repricing of the forward curve has direct valuation impact on equities, so Fed communication is a co-catalyst.

One more thing to anyone fearmongering a recession, the labor market can soften without a recession. There’s a plausible scenario where the Fed cuts enough to stabilise labor while US growth continues to outperform the RoW. That remains in the mix.

I also mentioned how if we see curve steepening, I think that gives upside in equities only if the energy component is fading. If the long end sells off because duration risk continues to increase on inflation uncertainty, the picture is more ambiguous. Mild, equities can shrug it off. Aggressive, the discount rate on future earnings rises, you get multiple compression, and the long thesis weakens.

The steepening I want to see is bull steepening, front end falling on repriced Fed expectations. But if labor continues to deteriorate simultaneously and credit spreads widen, even bull steepening doesn't give you clean upside in equities.

My base case is still that the transient oil shock fades, SOFR reprices at least 60bp into the Dec 26 contract, and the curve bull steepens.

Thanks all!

Great work Alfie ,fully follow great framework

The oil situation is now a little more complex then Trump announced on Monday ,Iran attacking oil tankers today

When you say the “want to see implied vol drop” what are you measuring? A number? Continuous dropping for a certain number of days? % move down?

Same question with credit spreads