Equities, bonds & FX: What's next?

How the war could transmit across equities, FX and bonds

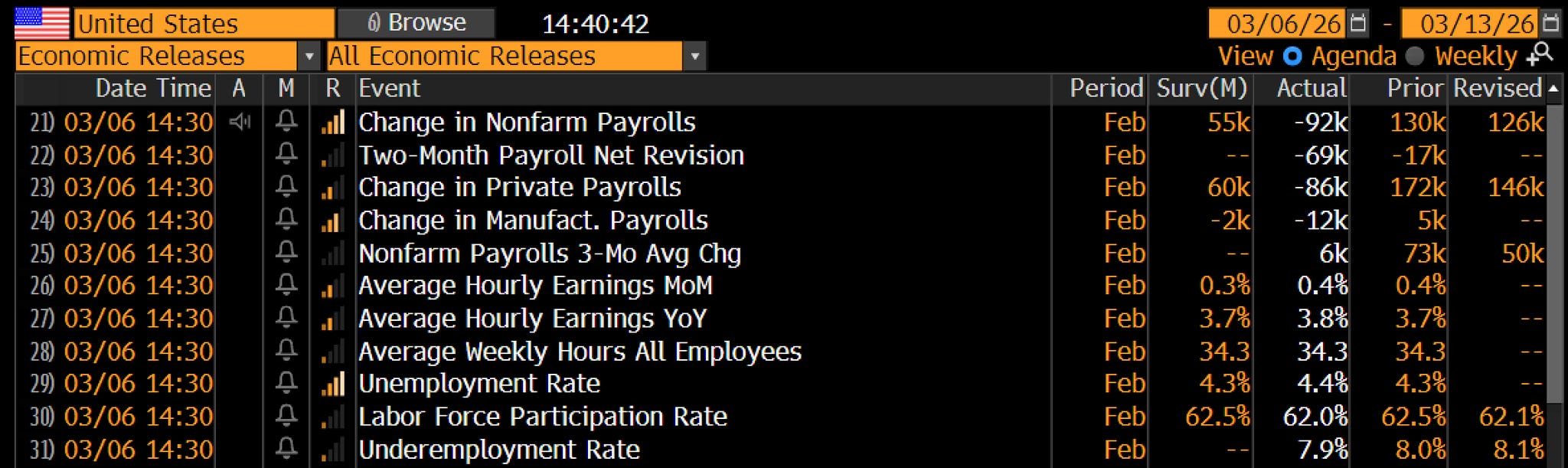

I want to first start by addressing NFP figures from friday and how im thinking about them.

So there’s emphasis on jobs data but there is no direct labor risk risk being expressed in bonds, FX or equities, all of this movement is driven directly by the US-Iran tensions.

Jobs data no doubt has a transmission effect from consumer spending, all the way through to corporate revenue, but we're simply not there yet. Given the interest rates the US has seen across the last 2 years, its a given that jobs data has direct pressures like this. If there were an immediate growth risk, we would not be seeing positive 3m & 6m annualised speeds across most growth metrics as rate cuts get priced out in my view (which will likely unwind). I’d say that the jobs data we're getting is important but the transmission won’t be immediate, we certainly wouldn’t be seeing corporate earnings smash estimates if growth was CURRENTLY an issue.

We're seeing MAJOR tail-risks with the US-Iran war right now as oil traded through $100 this morning, yet equities are 4.3% off ATHs (as I type). I believe that any fast slowdown in growth will be an existential risk (like major negative developments with this war) rather than any domestic action inside the US that sends them into a recession, it’s simply not a base case for me.

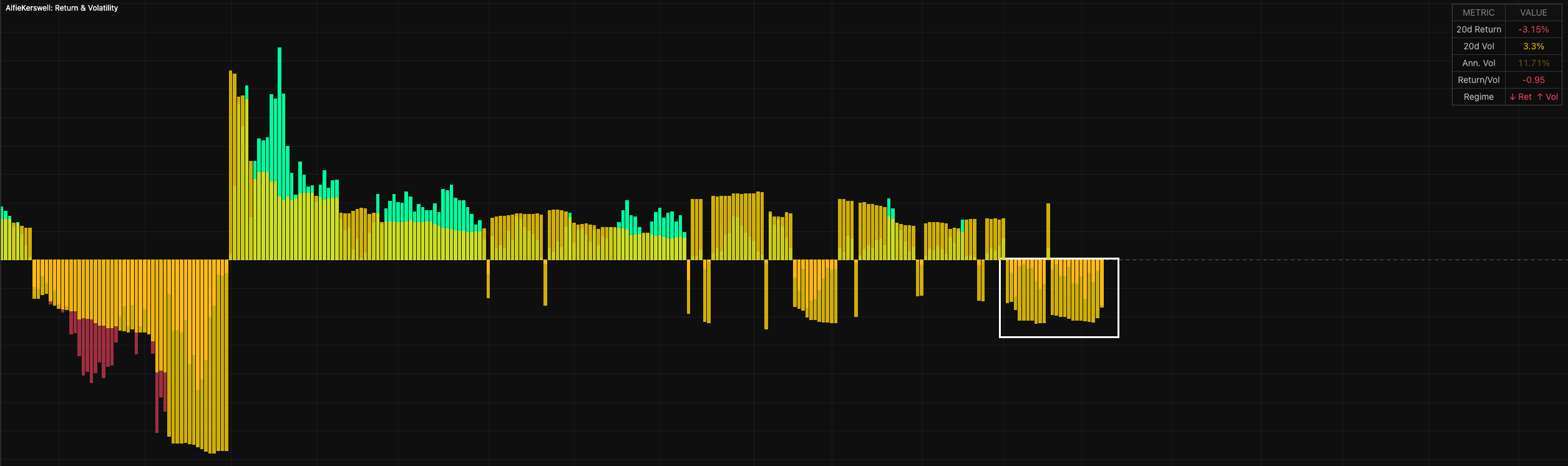

Equity vol has blown out in massive proportion and in my view, equities themselves haven’t reacted to the same degree. What I think the likely scenario is, is that as equity implied vol unwinds, then we will see an outsized move to the upside across EVERY sector. Why do i think this? Well, for every tick higher we have been getting in equity implied vol, the index fails to move lower to the same degree. When you run a historical test on this, you’ll be able to see how much the index typically moves for every 1 unit higher in vol (I will share this once the dashboard is debugged), we have seen LESS of a move lower in the index for every tick unit higher in vol which means there is a higher sensitivity to the UPSIDE in equities for every unit LOWER in equity vol.

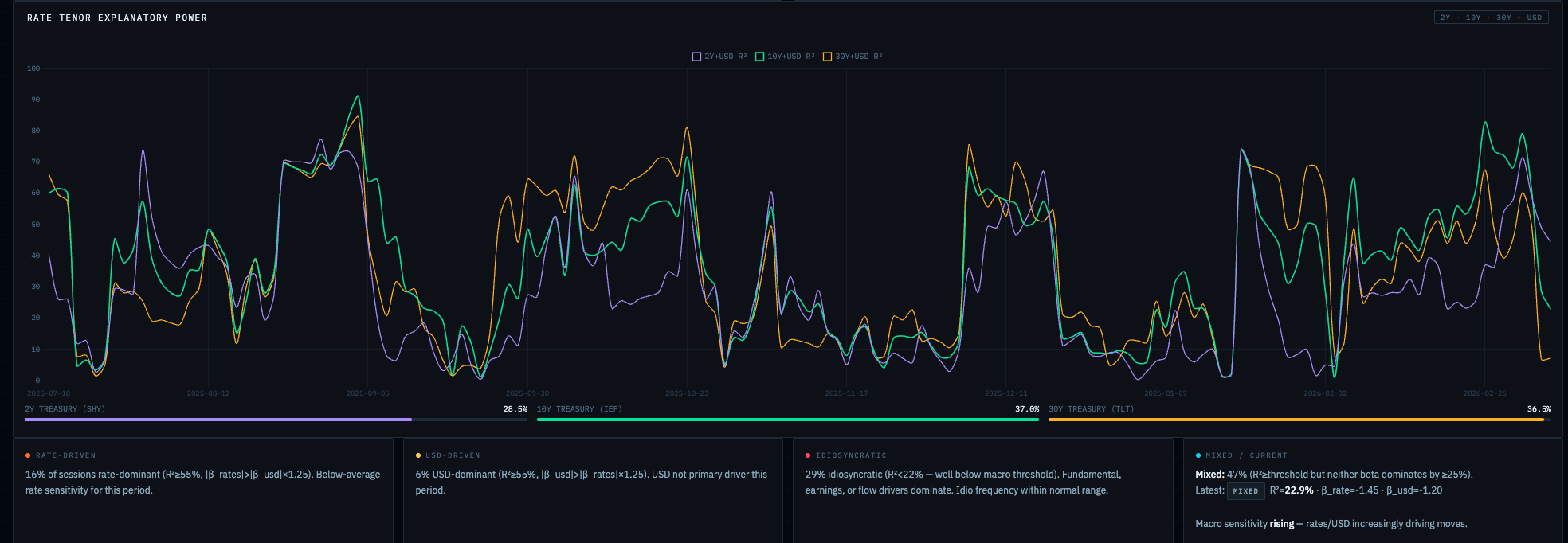

Rates are the control point. They are being driven heavily by inflation directly through the energy component, which can be unwound VERY fast in comparison to if the inflation component was being driven by something like services, which isn’t the case here. I’m monitoring the sensitivity rates have to oil in particular and have a few models running which will show me when a decorrelation occurs, then the rates regime moves away from inflation driving the market through the energy input. But I don’t expect to see that across the next week or two, not at least until oil creates a top and SOFR creates a bottom.

What's key to watch is that we've been sitting in this negative returns, high implied vol regime where there is LESS upside given such a premium in vol. When we begin to see this unwind on a 5d lookback (positive returns, lower vol), we'll have likely created a bottom and heading towards another leg higher in my view.

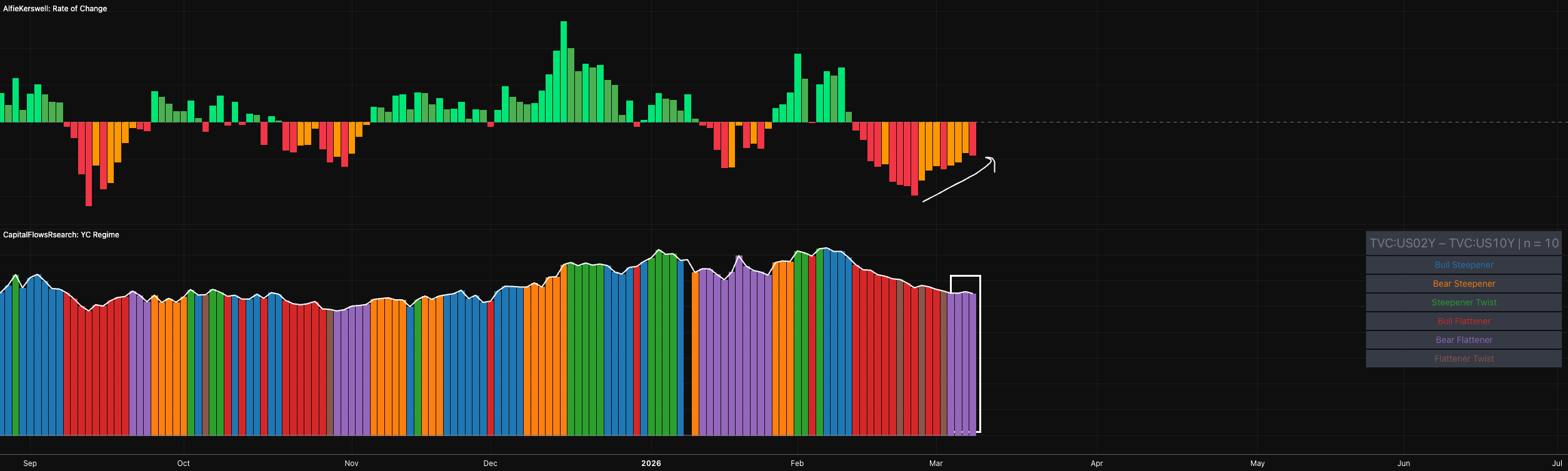

Now inflation risk is larger than growth risk (coming directly from energy), so the energy component is the direct source that will determine the next regime we step into. It is likely that for as long as oil fails to create meaningful pressures to the downside, a case for stagflation persists and the 2s10s is evidence that inflation risk is larger than growth risk as the curve bear flattens on repricing in SOFR.

BUT.. 2s10s has a negative RoC but at a diminishing pace so if we begin to see steepening in the curve as cuts start getting repriced in (likely), then ultimately I'll be more sure that we're not heading into any imminent slowdown. What I DON’T expect is sustained bear flattening acceleration, that would completely invalidate the oil-driven inflation peak thesis, and if the long-end sells off despite a front-end rally, that breaks the steepening narrative entirely through either breakeven deanchoring or fiscal concerns.

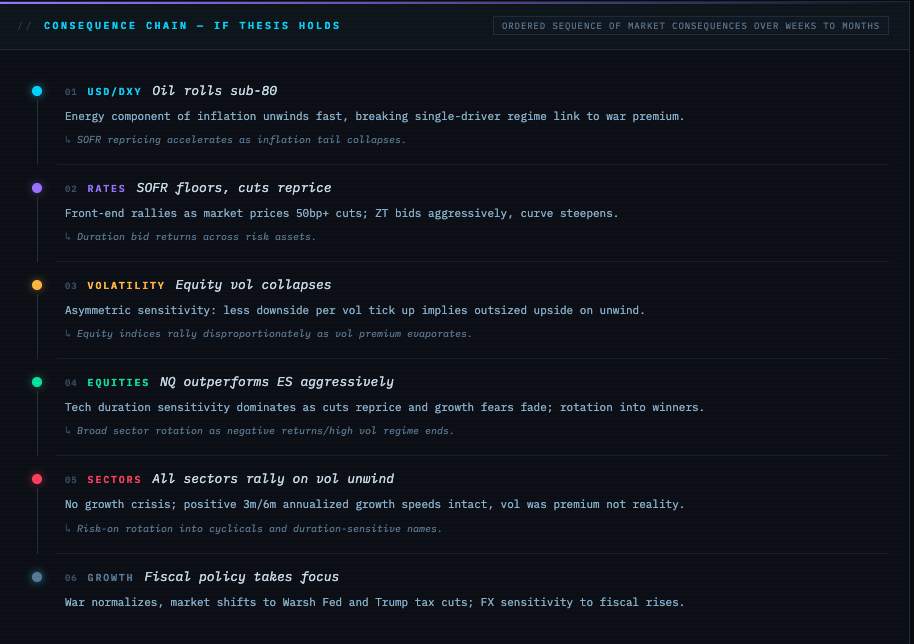

So the sequence I'm watching plays out like this. Oil creates a meaningful top and moves through sub-$80 and the energy-driven inflation component unwinds rapidly. SOFR repricing accelerates, front-end treasuries rally hard, ZT bids aggressively as 50bp+ cuts get priced back in. 2s10s steepening then resumes as the bear flattening exhausts itself, which confirms the regime shift. Real rates decline as cuts reprice faster than inflation unwinds, and that real rate compression is what supports risk assets. 5Y and 10Y breakevens compress as the energy disinflation dominates, though they'll lag spot oil a bit because services stickiness is still there in the background, if services stays sticky above 0.4% MoM then breakevens don’t compress the way the thesis needs.

On equities, if the war was still causing major downside, what we WOULDN’T be seeing is tech up and leading on the day as equity vol unwinds and NQ outperforms ES. This type of rotation is evidence that there is more sensitivity to the upside in equities when equity vol unwinds in comparison to any more premium being added to equity vol causing downside. NQ outperforming ES on vol unwind days, and the fact that the NQ/ES spread correlates directly to VIX collapse, tells you everything (tech duration sensitivity and vol unwind are moving in lockstep).

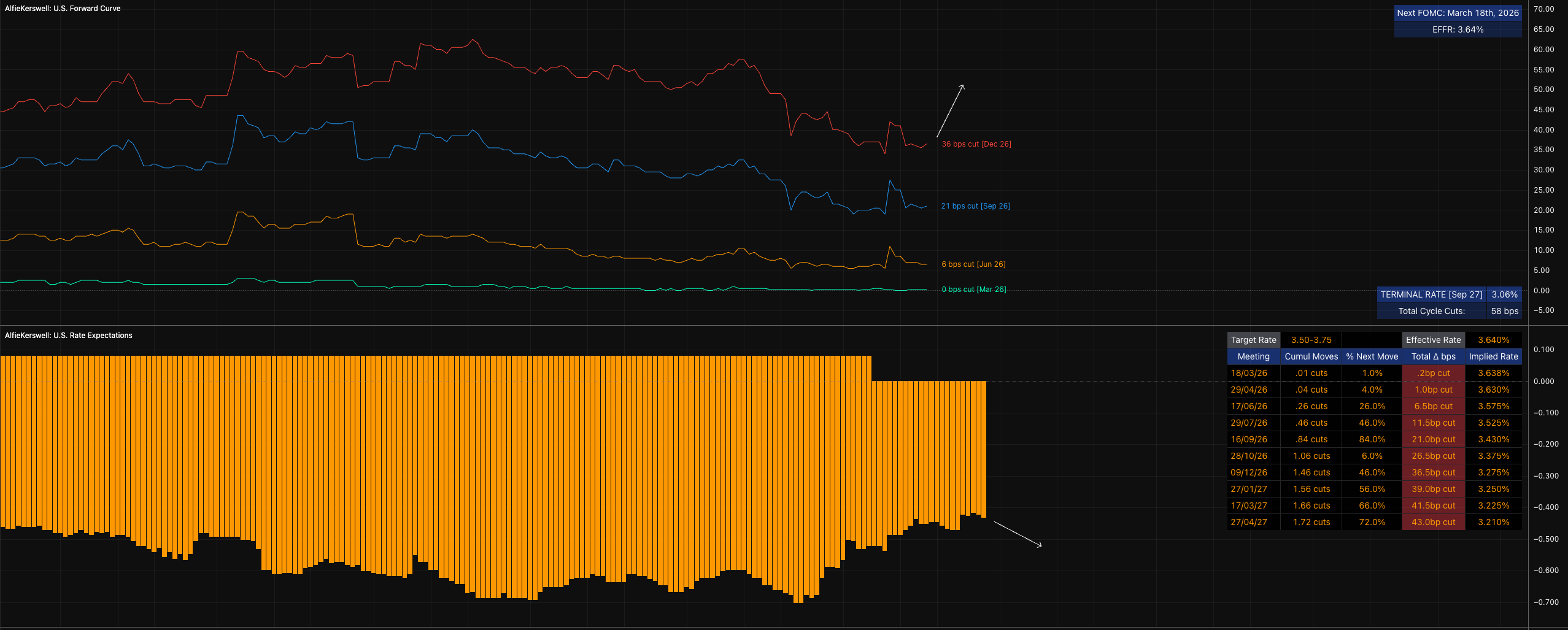

For this exact reason, and with the assumption that oil starts moving below $80 through the next 3-4 weeks with some momentum, I think we’ll see SOFR create a floor here and MORE cuts start being priced for the year. My base case is 50bp, but this is dependent on the energy component and just how fast oil rolls over, could push up to 75bp is NFP continues to print lower as the energy component becomes LESS of a risk.

The KEY RISK to all of this is if oil sustains above $100. If that happens, the energy inflation component persists, SOFR repricing stalls, and were stuck in this single-driver regime tied to the war premium indefinitely. The other invalidation I'd be watching closely is if equity vol starts rising while indices fall IN LINE with it, then that breaks the asymmetric sensitivity relationship and tells you the downside accelerates from here rather than the upside. Same with growth components, if 3m/6m growth speeds turn negative then the no-growth-crisis framework is dead.

Macro sensitivity is rising and the market is being driven by ONE input, war, or even Trump if you want to say that, because he is the ultimate driver of this war. Near term I’m watching CPI on March 11 for the energy component deceleration, FOMC March 19 for any dovish dots shift from the Fed transition, and retail sales March 14 to validate the jobs-to-spending lag thesis. When we begin to see oil roll and rates lead the way as ZT bids higher on repricing cuts BACK in, it’s likely going to be the best time to get long the index, particularly NQ. Monitor skew & implied vol through sessions and run analysis on the sensitivity to each side to build a picture of where the most tension is being held in markets and where the largest unwind is likely to happen, which, in my view, is to the UPSIDE in equities.

The thing about these market drivers (the war right now for example) is that when they blow over, everyone forgets. Literally just last year when it came to June everyone wanted to be heavily long equities but they wouldn’t even say that sentence 2 months prior. When the market normalises, it then starts to focus on real developments either through fiscal or monetary policy. Both are having MASSIVE shifts and will be the drivers through to the end of the year if/when this blows over.

We have Warsh taking charge of the Fed and Trump still yet to fully roll out things like tax cuts, and when the fiscal policy and plans really roll and transmit through the economy, I think FX is where the LEAST eyes are right now and where there will be the MOST sensitivity. That's where my concentration is shifting, building models to map out the implications of a change in both, but more so fiscal, because thats the underpriced driver in my view.

Here’s my visual view on how this plays out (1-2 months):

One of your best ,top read

Oil back at 80 ,Indexes flush out and bounce ,Dollar short ,like nothing ever happened

everything looking risk on again 🫡

very good, Thanks Alfie