Why The Dollar Will Soon Be The Greatest Assymetric Position

The Forward Curve Is The Trigger. The Fiscal Backdrop Is What Makes It Structural

Before we get into the report, I want to remind you guys of the FREE console giveaway on July 17th. To access the console, please see the beginning of this report below for steps.

Now I’m not in this position yet, but this is one I am looking to get into in the coming weeks if cross-asset confirmations and data support it.

Being short the dollar, let’s get into that.

Firstly, I want to mark the report from February when I was long the dollar, which was broadly driven by the forward curve, equity rotation and bond vol. The reason I’m marking this report is because these are three signals that could create the top in the dollar, just the opposite way this time.

Cross-asset vol & the forward curve

Firstly, I want to reiterate my point from the previous two reports that the dollar is NOT bidding because of any risk-off fear (neither driven by inflation or growth). Cross-asset vol is contained and if the dollar was driven by the previous months’ spike in implied vol, then the dollar would’ve unwound as these cross-asset vol levels normalised, which it didn’t.

The dollar trading higher is simply a function of the forward curve itself, which I believe has reached an extreme. I laid out in the report below that I see 50bp of hikes as an extreme and struggle to see a scenario where the Fed hikes twice, pauses for a small period of time, then begins cutting, particularly given that growth isn’t strong enough to give any type of massive tail-risk to inflation. The only need for a hike has come since the energy shock, which has now faded, and everyone is focused on how much will feed into core CPI, which I believe will be little.

The Fed control the demand side of the economy, not the supply side. The supply side has done all the work right now, dragged rate expectations higher after oil rose 70%+. Now oil has fallen 42% and rate expectations have repriced to the same degree, which makes sense because oil’s beta to rate expectations will always be higher on the way up than on the way down, simply due to the tail risks after inflation has hit headline, e.g. how much will flow into core.

Like I always say, if you have a thesis on markets, it needs to be expressed in the asset pricing, otherwise you’re either wrong or mistimed, or both.

Cross-asset vol is low. Cross-asset returns and correlations are clearly showing that there is minimal risk in the system, both growth and inflation, and therefore you cannot attribute the stronger dollar to that. The reason this attribution matters so much is because the thing currently driving the dollar needs to be the thing I focus on to unwind it, which is why I’m focused so heavily on the forward curve.

Credit spreads at cycle lows and the Russell outperforming the S&P 500 tells us exactly what is driving the dollar.

I already think that the inflation risk is declining. Long-end inflation swaps reflect that and ultimately the collapse in oil shows it isn't long lasting. But the evidence is that the Fed are already ahead of the curve, which is why we're seeing bear flattening across the board as the short end reprices more aggressively than the long end. It's basically the market saying that its views on growth and inflation haven't changed and the Fed are being too restrictive given that backdrop.

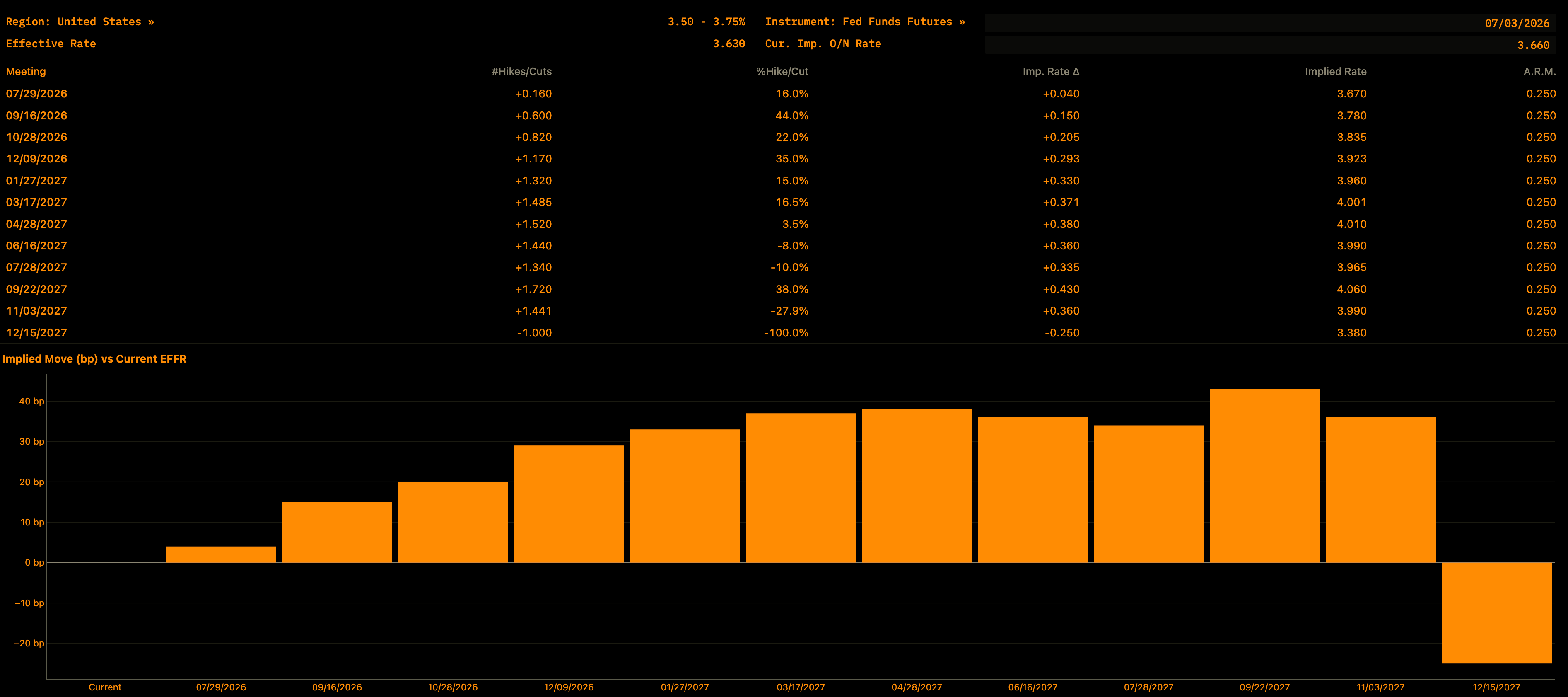

This is the current forward curve for the US.

The terminal rate has floated around the H7 contract for a while and in my recent report I discussed how I believe there is the most asymmetry in that contract if you are trading the SOFR strip directly. If we reprice even marginally, the dollar will have to reprice given that these differentials are the driver of price. In fact I believe the beta to rate expectations will be very high. If we begin to only price in 1 hike (base case), or even 0 hikes, the dollar will sell off meaningfully as differentials need to reprice, especially if the ECB remain hawkish, which is likely given their tailwind and the current level of rates and inflation tail-risk.

Fiscal policy

Now the fiscal side.

And this is the part of the story that I think is being massively underpriced by the market right now.

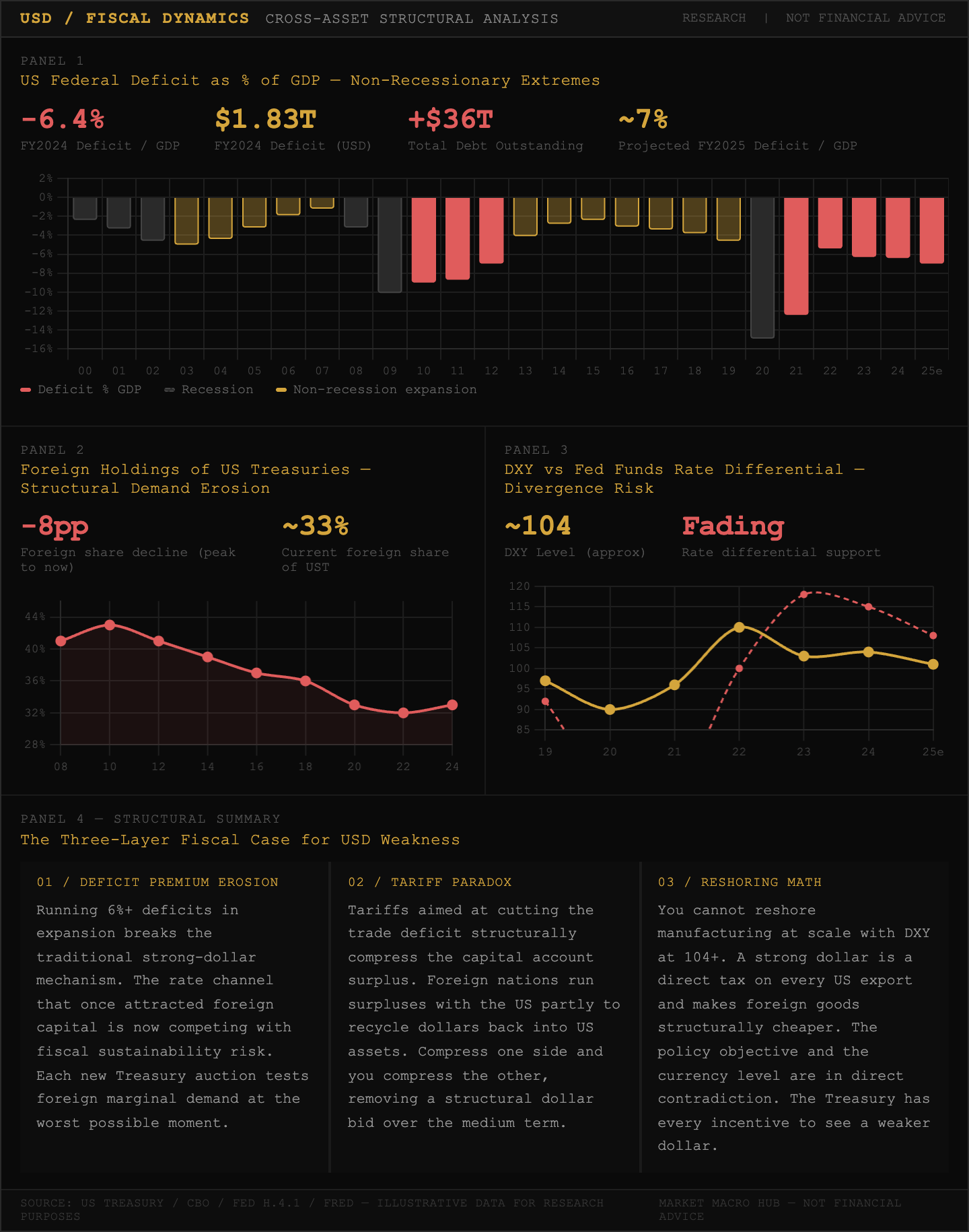

The structural argument for a weaker dollar doesn’t begin and end with rate differentials. If the US wants to compete with China on a global basis for exports, as the administration has made clear, they structurally need a weaker dollar.

You simply cannot reshore manufacturing at scale with DXY at these levels. The math doesn’t work. A strong dollar is a tax on every US export, it makes foreign-produced goods cheaper relative to domestically-produced ones, and it directly undermines the entire policy objective of rebuilding the US industrial base.

This isn’t just a political talking point either, it’s been a bipartisan structural problem for decades. The US has run persistent current account deficits precisely because the dollar’s reserve status creates excess demand for the currency, artificially inflating its value beyond what trade fundamentals would justify.

This is what economists refer to as the “exorbitant burden” of reserve currency status. The SAME privilege that gives the US cheap financing also prices its exporters out of global markets.

Now layer on top of that the current fiscal trajectory. The US is running deficits in excess of 6% of GDP in a non-recessionary environment. That is extraordinary by ANY historical standard. The traditional mechanism by which large fiscal deficits support a currency is through the rate channel, the government borrows heavily, rates rise, and foreign capital flows in to capture the yield differential. But that transmission is breaking down. The market is increasingly pricing the risk that the US is on an unsustainable fiscal path, which means the incremental dollar of Treasury issuance is being met with less and less foreign demand at the margin.

We’re already seeing early signs of this. Foreign central bank accumulation of US Treasuries has structurally slowed. The Fed’s own reverse repo facility saw massive drawdowns as domestic money market funds absorbed the supply that foreign buyers are no longer taking as aggressively. If foreign demand for Treasuries softens further, the dollar loses one of its key structural support mechanisms, not because rates fall, but because the safe-haven premium embedded in the currency begins to erode.

Then there is the tariff dimension. The administration’s tariff policy is explicitly designed to reduce the trade deficit, but here is the tension: a large portion of the trade deficit is a mirror image of the capital account surplus. Foreign nations run trade surpluses with the US partly because they are recycling those dollars back into US assets, Treasuries, equities, real estate. If tariffs succeed in compressing the trade deficit, by definition the capital account surplus compresses too, meaning less foreign demand for dollar-denominated assets. That is structurally bearish for the dollar over the medium term, regardless of the short-term inflationary impulse tariffs create.

And the short-term inflationary impulse is itself a problem for the dollar in a way that isn’t immediately obvious. If tariffs push inflation higher but growth weaker simultaneously, the Fed is boxed in. They CAN’T hike to defend the currency without accelerating a slowdown, and they CAN’T cut to support growth without risking an inflation re-acceleration. That stagflationary trap is the worst possible environment for the dollar because it REMOVES the Fed’s ability to credibly defend it through the rate channel, which as I’ve laid out is the primary driver of dollar strength right now.

So when I put all of this together, the rate differential argument for a strong dollar is fading as the forward curve reprices. The structural fiscal argument points to a dollar that is being propped up by a premium that is slowly being questioned. And the policy mix, tariffs combined with reshoring ambitions combined with a Treasury that has every incentive to see a weaker dollar, all point in the same direction. The forward curve is the trigger, but the fiscal backdrop is what makes this a structural move rather than just a tactical one.

Thanks

Alfie

Fully agree here!

Nice read! Thank you for your view and input as always.

While I align with the forward curve mispricing argument, I fundamentally disagree with the rest of the thesis.

My take on this bullish dollar is that the global economy is structurally short the dollar through trillions in offshore USD debt. When an oil price spike hits without a real wage bounce, consumers get crushed, triggering a severe economic slowdown. This contraction kills the organic dollar revenues of these countries. Because their fixed dollar liabilities remain rigid while their dollar inflows dry up, mechanical demand for dollars rise, forcing a procyclical short squeeze that drives the dollar higher.

However i am on the opposite side, i hope youre thesis plays out, and if you have some counter arguments i can learn from theyre always welcome :)!