Against Consensus: Dollar Upside Ahead

Why Lower Rates Won't Weaken the Dollar

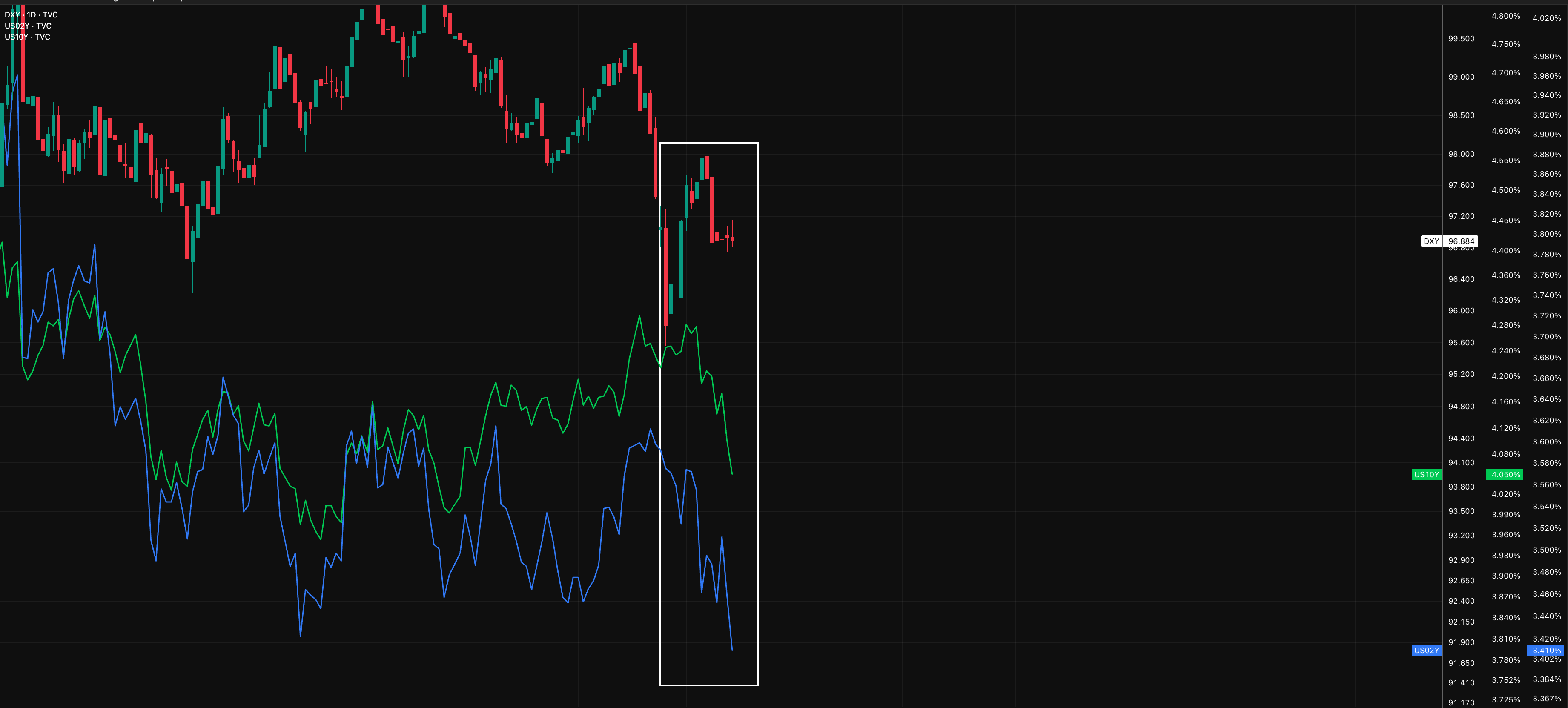

The market traded in dislocation two weeks ago and still has room to catch up, the dollar started trading higher with equities as yields fell. We did see a sharp drop in the dollar on Monday but honestly nothing to reflect the momentum of front-end yields. There were (and still is) two scenarios for the setup: equities start creating lower lows as rotation causes downward pressure, which indirectly causes a negative correlation with he dollar as the dollar trades higher. Or scenario two, the dollar catches up on with falling yields and outperforms on a cross-sectional momentum basis

Even as the short end bids higher and yields roll lower, the dollar is struggling to move with any like-for-like momentum. Yes, there is times that there’s disclocation between the front-end and the dollar. But when it trades with lower corrlation for a prolonged period of time, the move that can bring them back together can be sharp.

Last week convicned me that we could see the dollar trade higher as equities trade lower, but of course the key is the drivers. I wont repeat everything I laid out in the previous report but there’s some key things that are showing how much the dollar is struggling to move lower.

1) The dollars main driver, front-end rate expectations.

The terminal rate has been repriced marginally lower (about an extra 14bps), the rate now sits around 3% which is being solidified in the front-end. The issue is that this is causing NO marginal downward pressure on the dollar.

That’s evidence that markets believe US economic resilience remains superior even with rate cuts. If cuts are seen as extending the expansion while other economies face sharper slowdowns or recession, the dollar strengthens on relative growth optimism. The 2s20s is telling us that. For the last 2 months the curve has continued to be dominated by steepening, driven by higher growth expectations.

The danger here would be to keep being short USD because more cuts are being priced, as equity valuations remain strong and growth is priced in curves. That’s a danger because you’re assuming the path is linear, but rotation is causing upward pressure on the dollar in my view which directly causes LESS sensitiv ity in the dollar when the front-end prices in more cuts or the terminal prices lower.

An example is that in normal conditions, you’d expect movements in the front-end to cause a relatiively similar move in the dollar. But when we start having external pressures provide strength to the dollar, then there is much more movement in the front-end needed to cause any movement in the currency itself.

2) How bonds determine the extent of the move

The extent of the upward pressure in the USD and period of time is going to be driven by how the dollar moves relative to the front-end as bonds make higher highs. If we break this range below in ZT and maintain ABOVE the range as the dollar fails to create a leg lower, I’d expect the dollar to actually make a leg much higher than I anticipate now. But if we begin trading in a range in bonds from here, I’d expect the dollar to still trade towards 99.

I see the relationship as this: any movements in front-end yields LOWER will cause unnoticeable movement in the dollar, but re-pricing of the terminal rate HIGHER or front-end yields moving HIGHER will cause more of an outsized move in the dollar, HIGHER.

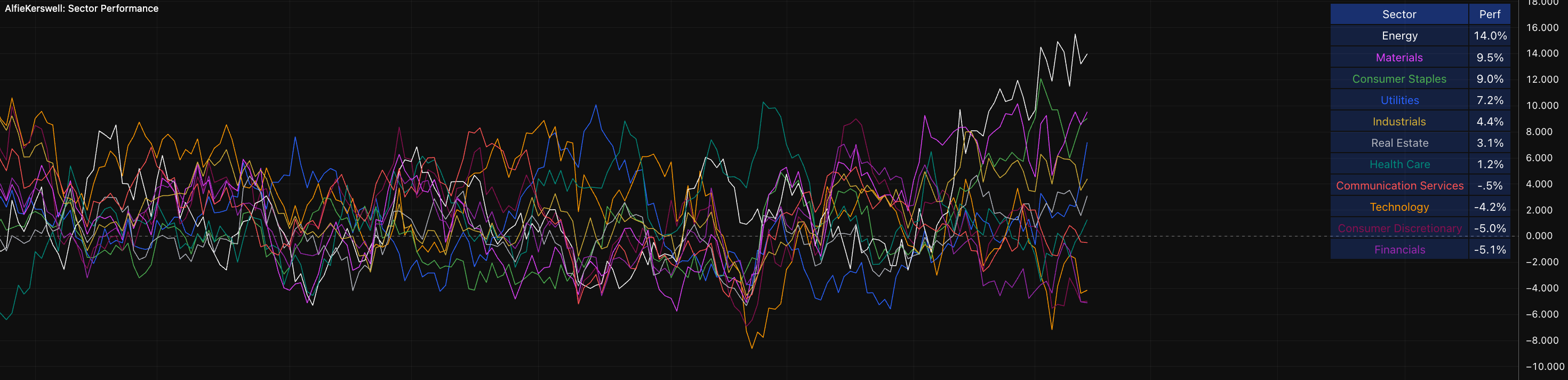

The implications of this doesn’t mean that equities can’t trade higher, in fact they COULD trade higher, but not with any momentum in my view. I laid out why the regime is still faovuring being long equities BUT the timing and price of positioning is important. We could also see a scenario where the dollar trades in negtaive correlation to equites as equities begin getting dragged further by rotation (likely in my view), just look at how defensive positioning has shifted in the sectors:

Equity vol is also causing marginal bidding in the dollar since the beginning of Feb. Equities have barely moved, we’ve been stuck in a range as implied vol rises from a combination of geopolitcal issues, rotation & even a shift in the Fed chair final outcome. Danger zone is here when VIX is trading above 1 on a z score basis, which it is.

Over the last month we’ve even seen bonds rally while causing marginal downward pressure on equities, as even equities are becoming LESS sensitive to changes in the front-end. When bonds rallying, you want to see equities outperform them with momentum as MORE cuts causes outsized upward pressure particularly in tech, but we haven’t seen that.

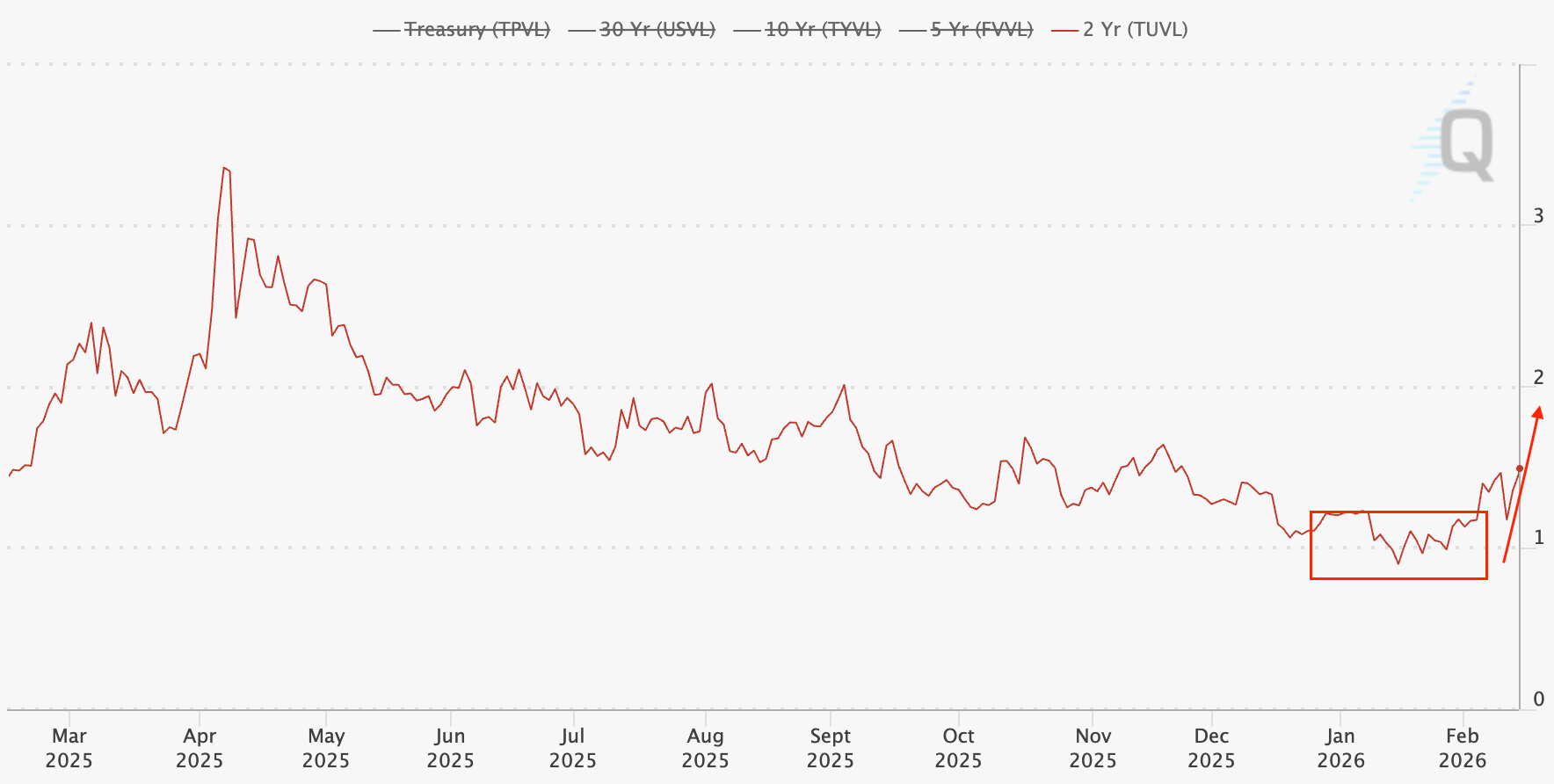

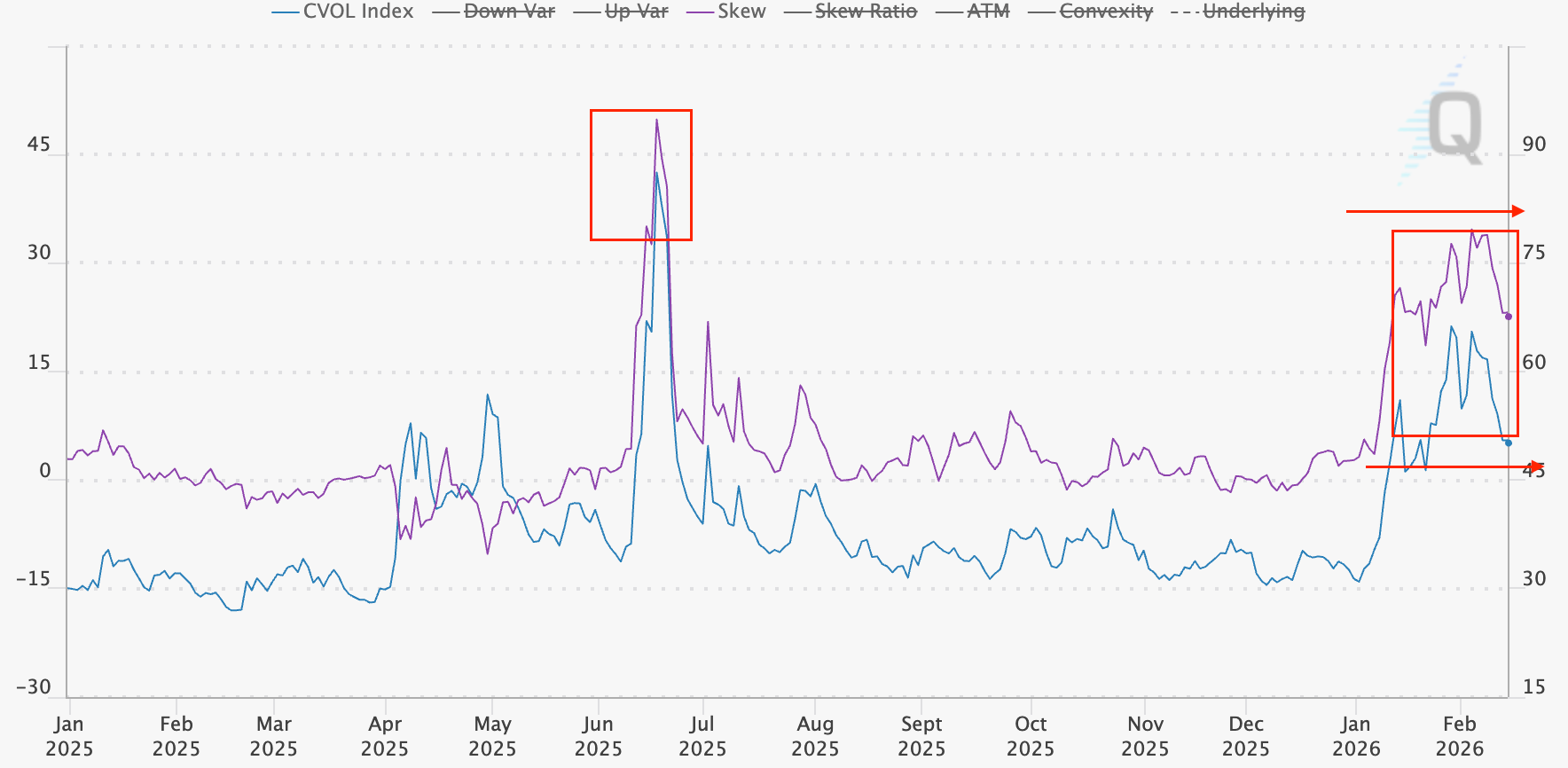

Skew is also posiitoned to see further upside in bonds. If we go off of the relationship we’ve seen as of recent, this means LESS upside in equities and MORE upside in the dollar.

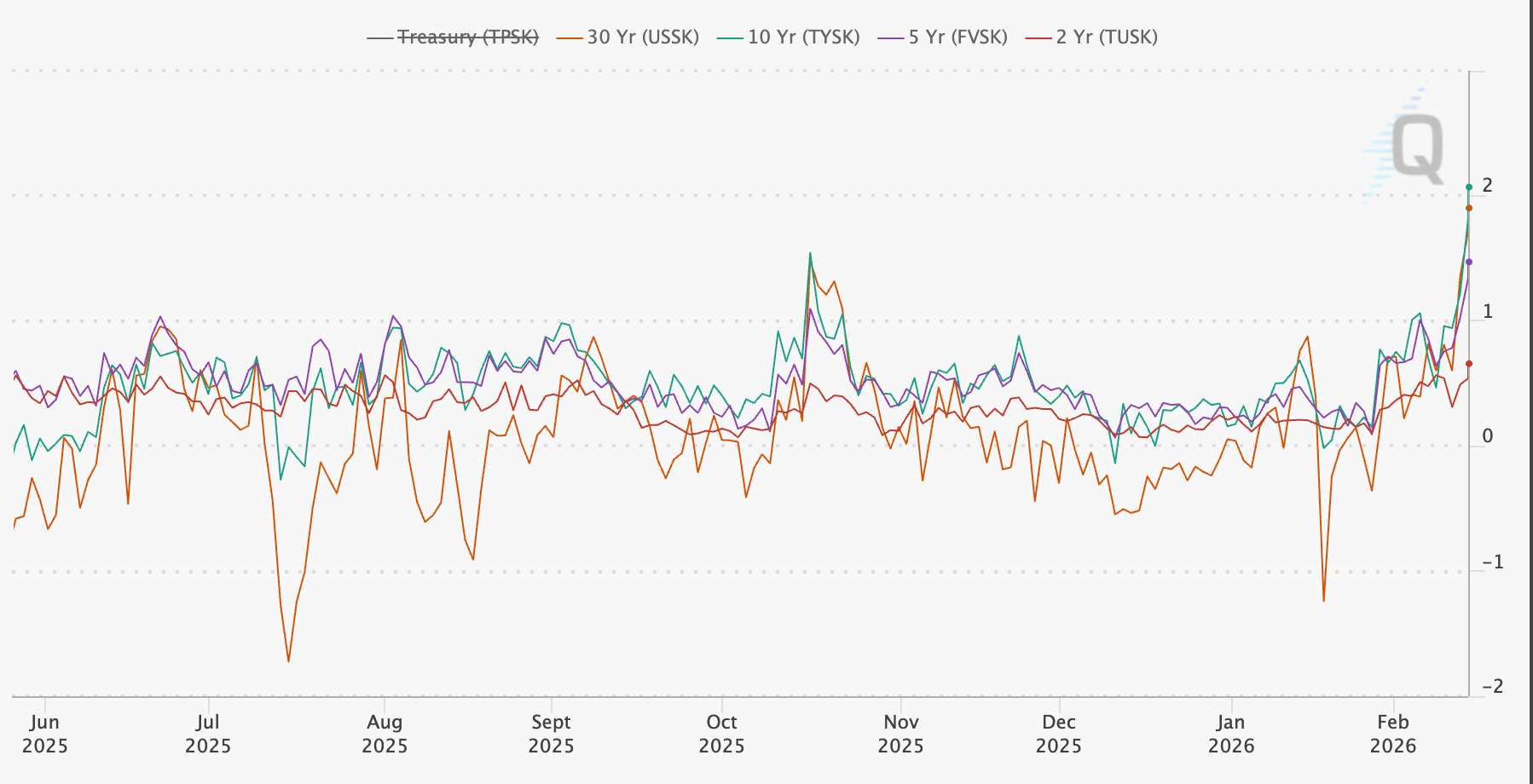

Implied vol on the front end looks to have created a floor and is trading HIGHER

There’s also one key dynamic to point out. Even if tensions DON’T escalate with Iran and the U.S., oil trading at these higher levels price levels, implied vol and skew) causes upwards pressure on the dollar both directly and indirectly. Even if we created a top in skew & implied vol in oil, the levels at which we trade at through the next week matter A LOT. Basically, if we hold these levels and trade in these ranges as oil creates a higher high, then there is upward pressure on the dollar.

My view is that the dollar will begin to trade higher, towards the 99 level as bonds range and equities see marginal downward pressure.