Part 1: What If The Fed Look Through Inflation?

The Fed Looking Through Inflation: What It Means Across Every Asset Class

I’m going to make this a two part piece about the implications of the Fed looking through this inflationary tail-risk. This is most important right now as everyone is questioning just how much this will move into core CPI, then the Fed is stuck.

Firstly, when quantifying these changes and trying to find the most likely transmission channel, the part you want to focus on first is rates, then FX, then equities because equities are just a function of what rates and FX are doing:

So I want to begin with a scenario about what could actually happening here. The Fed is sitting with rates at 3.75% with short-term inflation swaps running above target and energy prices being pushed around by the Middle East. There is more risk of persistent above-target inflation throughout 2026 and yet the forward curve is beginning to shift back towards pricing a probability of cuts this year which will likely get more aggressive in repricing as we progress through this cross-asset implied vol/geopolitical premium unwind.

The Fed are going to likely make a conscious decision that the one-off nature of the price-level shock from energy does NOT warrant a policy response because that would likely crush the labour market, and real consumer spending definitely isn’t at levels that would survive hikes in my view.

See my recent video breakdown on this idea below:

The Dec26 contract has a bunch of vol running through it, you can see this in the open interest if you go to the CME website. So if you’re trading the forward curve directly you want to be most exposed to Dec26-Mar27 in my view. It was only last month we had the terminal rate sitting in the Sep27 contract, and in my view I think it probably stays there because even if we get repricing of the curve (likely), I think it’s unlikely that the terminal is brought forward because that’d be a little extreme considering the backdrop (if they’re going to cut into inflation, they’ll do it slowly). So I think we’re likely to see a shift in the terminal rate from Z7 to U7 at best.

You can access ALL tradingview models like these above for FREE here:

What It Does to Rates

Start with the front-end because that is where the Fed actually has control. If the committee is on hold but leaning toward one cut, then 2y rates are basically anchored in a range. It can’t rally dramatically because the Fed is not hiking, and it can’t sell off hard because the repricing of rate expecttaions isn’t front-loaded and hasn’t been that aggressive YET. I think given the setup with real consumer spending and job market growth, it is HIGHLY unlikely that we see 2y rates rally above 4.1%.

The direct implication of inflation being seen as a one-off shock is that the 2y has a ceiling, but this is likely to set us up for a higher normalised range in the 2y when the liqudiity in the system becomes unsustainable and the Fed are FORCED to hike into whatever backdrop they’re dealing with.

Of course the Fed has made it clear that they need meaningful confidence that inflation is moving lower in a lasting way before acting. So what you get in 2y rates is a tight range where it’s pinned by the forces of the forward curve but also higher realised inflation/lliqudiity in the system. Rates in this type of regime would be the most sensitive to data surprises rather than any directional repricing of the policy path vs equities or the dollar.

The long end is a completely different conversation. 10y rates are NOT set by the Fed. They are set by growth expectations, inflation expectations, term premium, and increasingly by the foreign bid for US assets (cross border flows). So when the Fed looks through inflation, what the bond market hears is that real rates are going to be held below where a strict inflation fighting mandate would put them. It’s still a very different picture to 2022, but the risks are that the Fed starts falling behind the curve and pinning real rates WAY lower than they should.

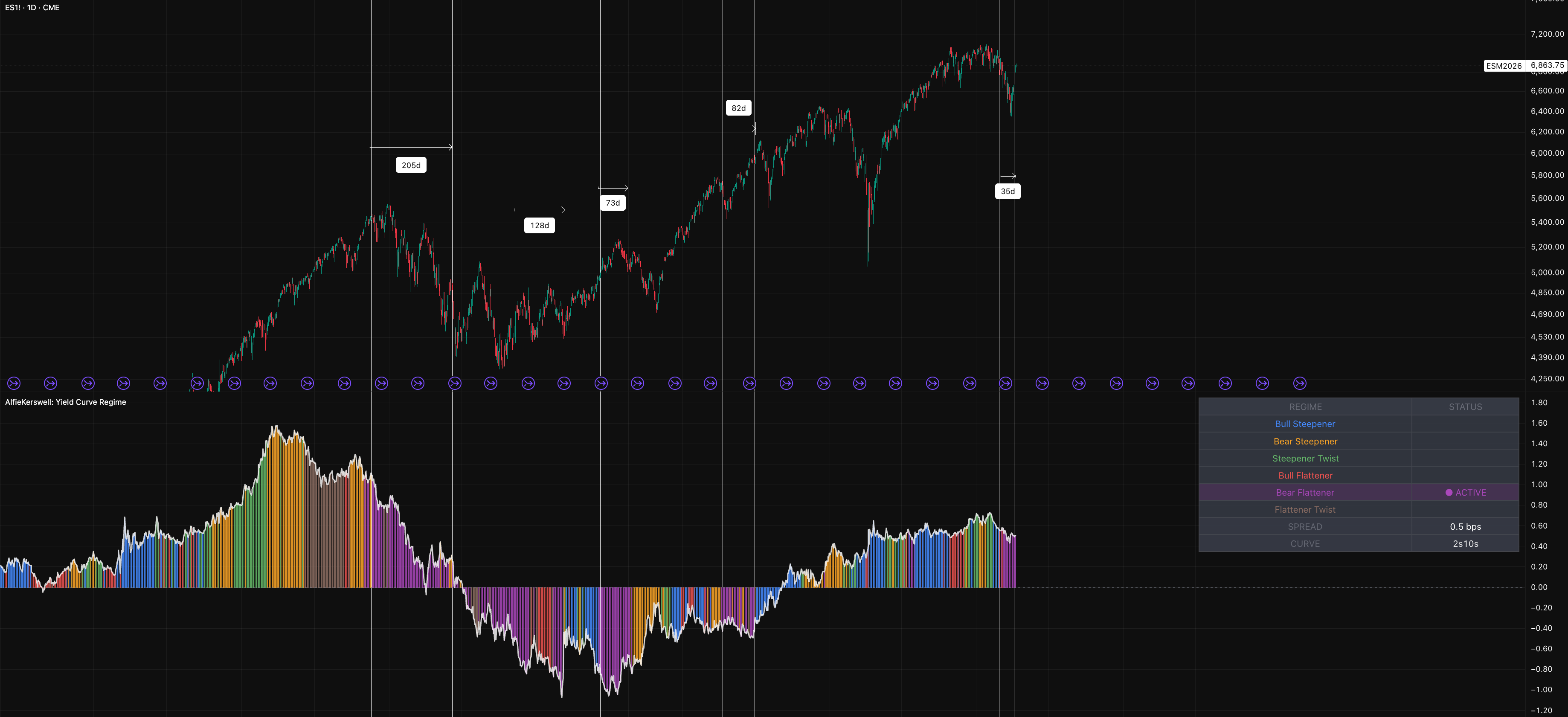

I think the 10y could be structurally pinned higher than the 2y which is why I expect to see a bunch of steepening in the 2s10s.

If the market decides the Fed is making a policy mistake, term premium starts to rise which is why I said that I think the 10y will be structurally pinned higher than the 2y. You can get a situation where the nominal yield is actually going up even as rate expectations drift lower because the inflation compensation demanded by bondholders is expanding, basically more duration risk starts being hedged.

The more interesting 2s10s steepening I’m watching for is the bearish kind, where the front-end is held by policy but 10y rates rally because the market is questioning whether the Fed’s dovish lean is going to structurally undermine the inflation anchor. There’s a strong case that the Fed falls way behind the curve by the time we move into 2027, and I’m spending time thinking about the implications of that but most of all, the direct beneficaries.

Bear steepening is NOT friendly for equities. It’s the rates regime where you get rising long rates that are signaling credibility concerns, which is a COMPLETELY different transmission mechanism than what most equity investors are pricing in. ES struggles in most 2s10s bear flattening regimes:

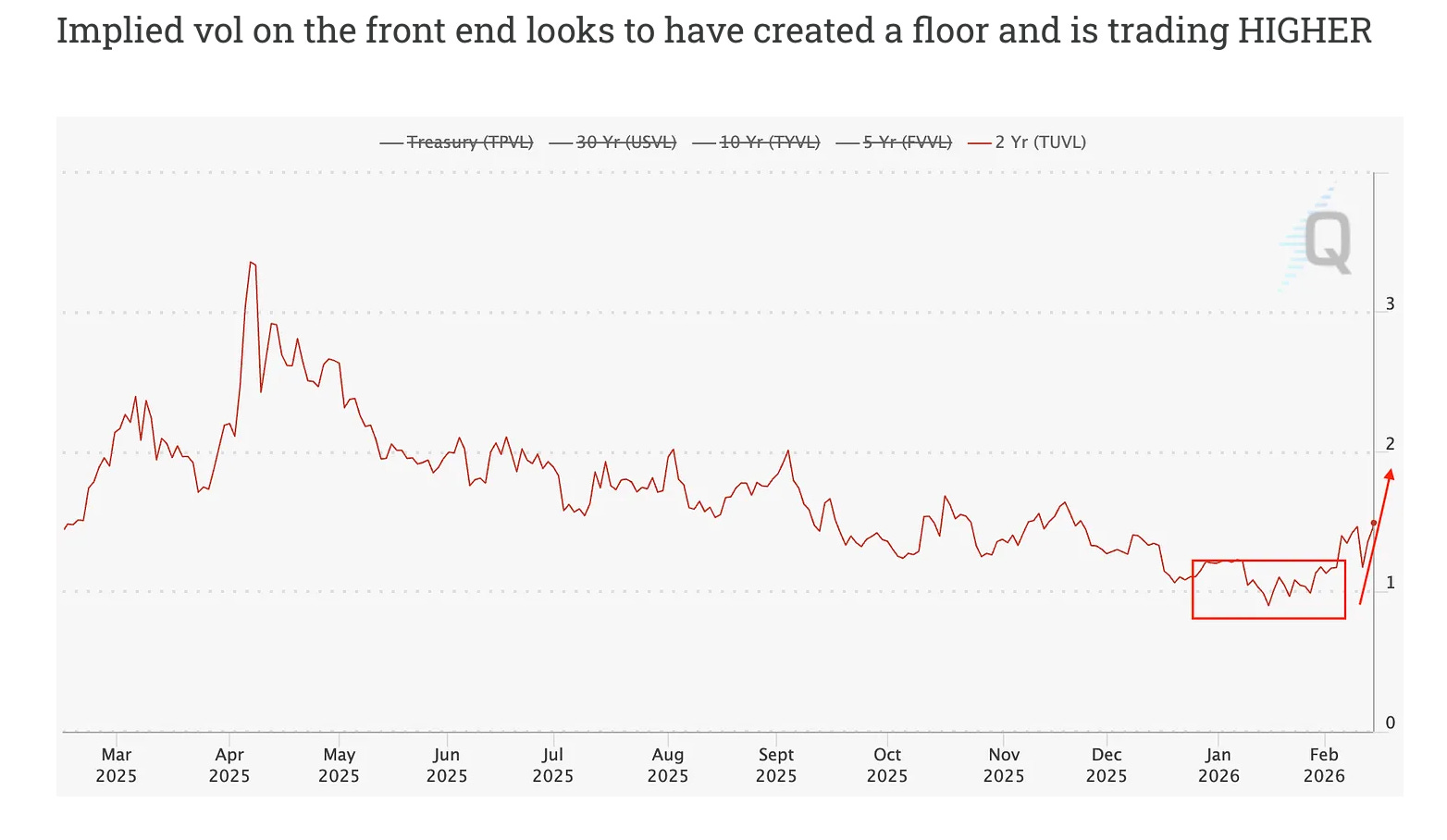

The setup in inflation swaps is interesting because the 5-10y swaps (which is the market’s cleanest read on long-run inflation expectations), have remained broadly consistent with heading towards the 2% target. So the market is not yet calling the Fed’s credibility into question at the long horizon, there is just simply a tail-risk scenario which involves the Fed looking through inflation (if it transmits into core, which could be lagged… and they may have already cut by then).

It is only near-term inflation swaps that have moved, which tells me the market believes the transitory story but is hedging against the risk that it’s not.

There is not as much of a fade trade in SOFR as there was a couple weeks ago, unless you believe the Fed is going to be materially more dovish than advertised (which would require a labour market deterioration that is not in the current data).

Job gains have remained low across the last few months (bar the recent release), and the unemployment rate has been little changed in recent months, which looks more like reduced hiring vs outright widespread layoffs, but we could definitely see that theme a companies cut back on nonsense roles and literally just set up an AI agent to replace them.

The data that begins to matter more as a trader when the Fed is looking through inflation is not what most people think. Of course everyone fixates on CPI and PCE, and yes they matter, but they are lagging indicators in this regime. What you actually need to watch is inflation swaps across the curve to see how the market thinks about longer-term inflation.

Right alongside that, unit labour costs and average hourly earnings becomes MASSIVE because wage growth is the mechanism through which a supply-side price shock becomes embedded in the cost structure of the economy and turns into genuine second-round inflation. If wages become hot, then the transitory idea isn’t valid.

When households start expecting higher prices, they start demanding higher wages and bringing forward purchases, which is self-fulfilling in a way that market breakevens are not.

The Volatility Complex and How It Transmits

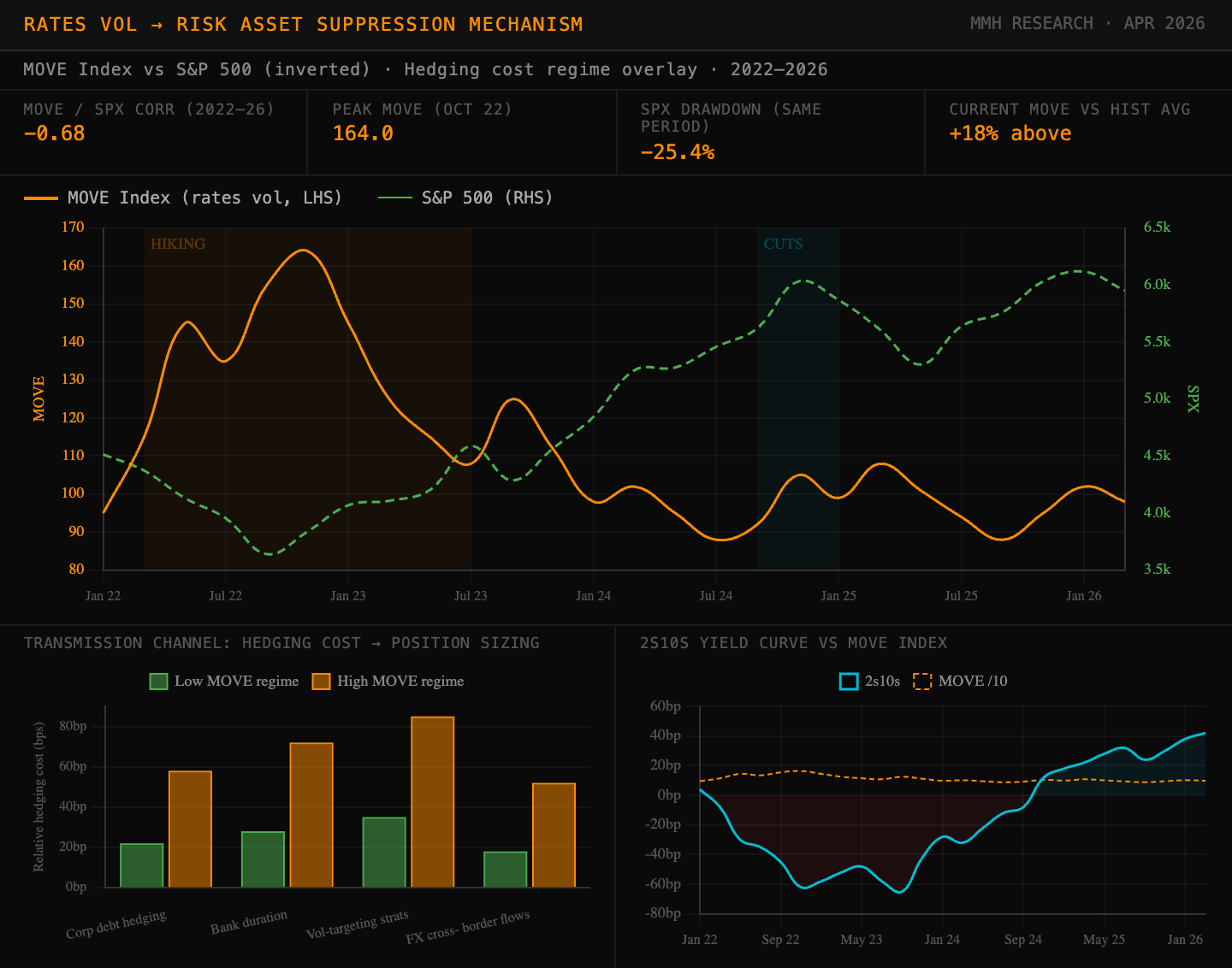

Rates volatility is the parent asset class for everything else. When implied vol in bonds is elevated, it means there is real uncertainty about where short and long rates are going. That uncertainty does NOT stay in the bond market. It bleeds into FX implied vols, which bleed into equity implied vols, which ultimately determine how risk assets are priced across the whole spectrum (look at the visual at the top of the report on this connection: rates > FX > equities). Rates are the heart of ALL markets in my view, equities are just a function of what rates and FX are doing.

I actually made a point in a previous report, before this blow out in cross-asset vol, that there were tensions underneath the surface across the rates curve that gave rates and the dollar massive upside:

See the report here for context:

When rates vol is high, the cost of hedging interest rate exposure goes up (plus the rates market is the largest market for hedging risk). So then that makes it more expensive for corporates to hedge their debt, more expensive for banks to run duration, and more expensive for systematic strategies that use vol as an input to their position sizing to hold risk.

Basically, when the cost of hedging goes up, exposure gets trimmed across the board, and that means lower equilibrium prices for risk assets regardless of the underlying fundamental story (which is why we actually see the S&P hold up well considering the risks, because underlying fundamentals are strong but the macro backdrop was the drag).

Equities don’t like bond vol:

When the hiking cycle was live, every CPI print was a potential catalyst for a repricing of the policy path, and that is what kept bond vol elevated relative to historical norms. So if the Fed stay on hold near-term and begin to cut through the next 6 months, the directional uncertainty in the short end collapses.

On the other hand, if the market starts to question the credibility of looking through inflation, you get long-end vol picking up even as front-end vol stays contained (the idea above), and we’d see MASSIVE steepening in the 2s10s.

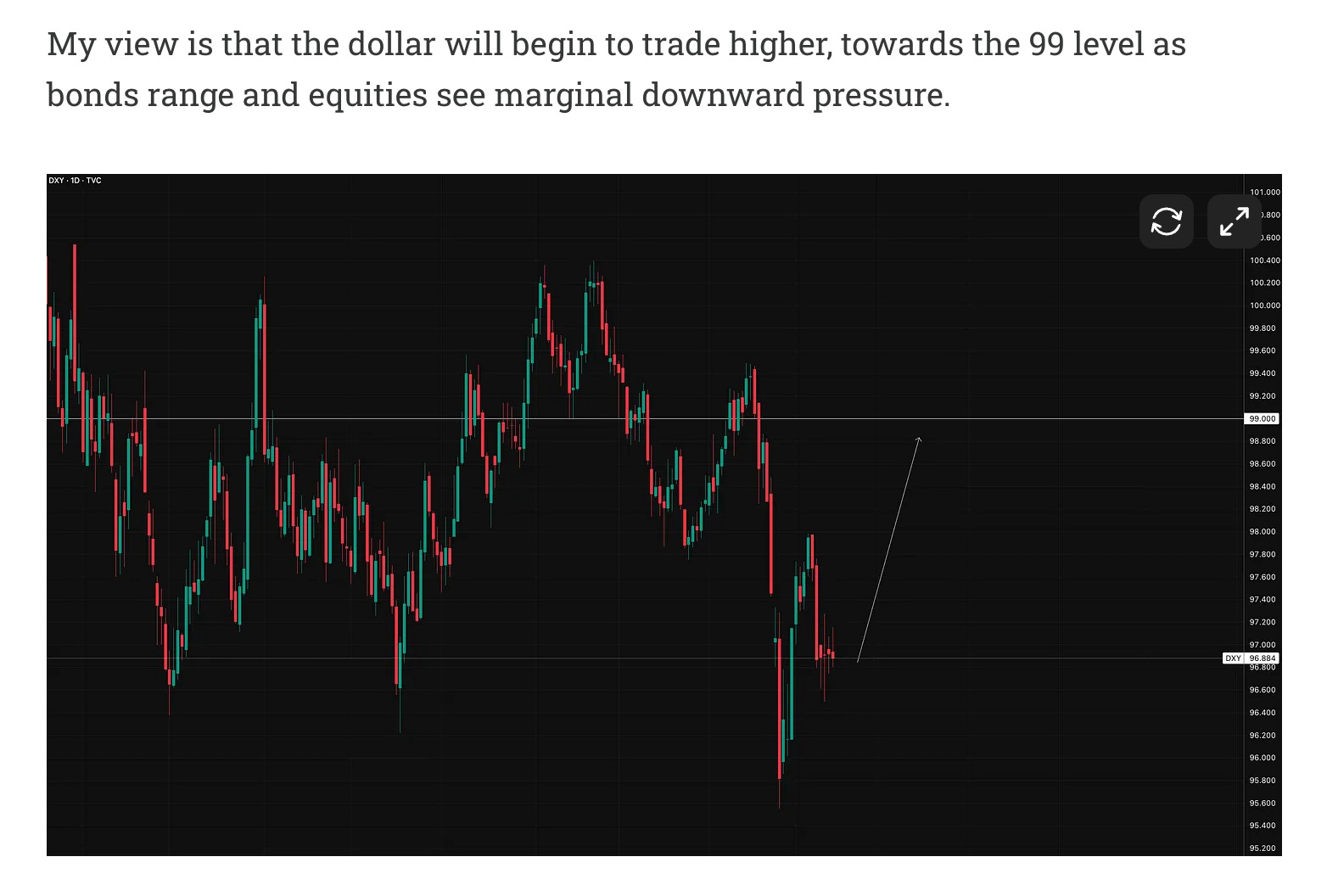

The transmission from rates vol into FX vol is very reflexive. When you don’t know where US rates are going, you don’t know what the carry differential between the dollar and every other currency is going to be. So that uncertainty means FX options are more expensive. More expensive FX options mean it costs more to run open cross-border positions, which deters capital flows at the margin and can create the kind of choppy, two way price action that you have been seeing in majors this year.

The transmission from FX vol into equity vol is slightly less reflexive. When currencies are moving aggressively, the earnings uncertainty for multinationals with significant non-dollar revenues or costs expands MASSIVELY. A big unexpected move in EURUSD or USDJPY in a quarter can swing EPS outcomes by hundreds of basis points for large cap exporters. That earnings uncertainty gets priced into equity implied vol, and elevated equity vol suppresses valuations through the discount rate and risk premium channels simultaneously.

The casual chain is: Rates > FX > Equities. Equities are simply a function of the state of the rates and FX market. There will be a part 2 on this idea where I’ll be covering the implications of this idea on FX and equities, but sectors in particular.

This is a visual on the implications:

Thanks

Alfie

Great article I couldn’t have said it better myself rates vol is the lynchpin for everything in our financial system. i’m looking forward to the video!