Why Treasury Notes Look Short (to me)

Exploring the Factors Behind a Potential Treasury Note Sell-Off

Hey guys,

A week of ultimate flow, like no other I’ve experienced.

It’s for the love of this game that I’m here at 21:09pm on a Friday, about to dive deep into a report for you guys.

The UK budget, U.S. elections on the horizon and “weak” payrolls.

An eventful week.

Macro watch

The Euro area’s manufacturing PMIs have been in contractionary conditions since July 2022, with Germany (the “sick” country) leading the way into negative growth. They need some serious changes if they’re looking to avoid danger for longer, although it won’t be a fast process even if measures are taken now. The one solution is clearly global trade diversification, which Germany has begun, tipping some focus towards India.

The large tail-risk I’m currently overseeing for the Euro area’s manufacturing sector is Trump’s tariffs. The U.S. is the EU’s largest trade partner for exports, a country they heavily rely on for revenue. In a scenario where Trump is elected on Tuesday, the EU will face tariffs of 10-20% for exports to the U.S., meaning U.S. companies will be deterred from using EU suppliers due to higher costs and they will favour domestic trade, something Trump is trying to impose heavily.

The German Economic Institute warned that Trump’s tariffs could lead to c.$162bn in losses for German companies. If Germany thought the damage had peaked in their manufacturing industry, they really have something else coming.

Long-end Bunds have begun pricing in a term-premium, almost in direct correlation with Trump’s winning probabilities, dis-inverting the 2s10s curve further.

Market mover

The UK’s budget on Wednesday announced rises in capital gains tax (CGT), with the power end tax bracket moving up 8% to 18% while the higher end tax bracket moved just 4% to 24%. Other tax portions were increased, CGT being the most noticeable, and these will all contribute to a total of c.£40bn of tax increases per year for the UK.

After the budget, the OBR forecasts were disappointing for the Gilt market. Although GDP will see a small jump next year, to 2%, the OBR expect growth to drag after that: 1.8% (2026) and 1.5% thereafter.

The forecasts hit Gilts initially due to the higher issuance, then rate swaps shortly after. The swap rates for September 2025 are pricing the Bank Rate at c.4.1%, up from c.3.8% prior to the budget release. The uptick in inflation expectations is due to the amount of government spending (c.£70bn) and an extra £12bn of Gilt issuance, taking the total to £300bn of Gilts, both seen as reflationary.

This was truly the last thing the BoE needed, roll on November 7th.

In just 3 days, the sterling (in trade weighted terms) was down by 1.2%. That's the biggest fall in more than 18 months. However, swap differentials may offer the Pound a floor, especially if reflation becomes a larger and more consistent issue.

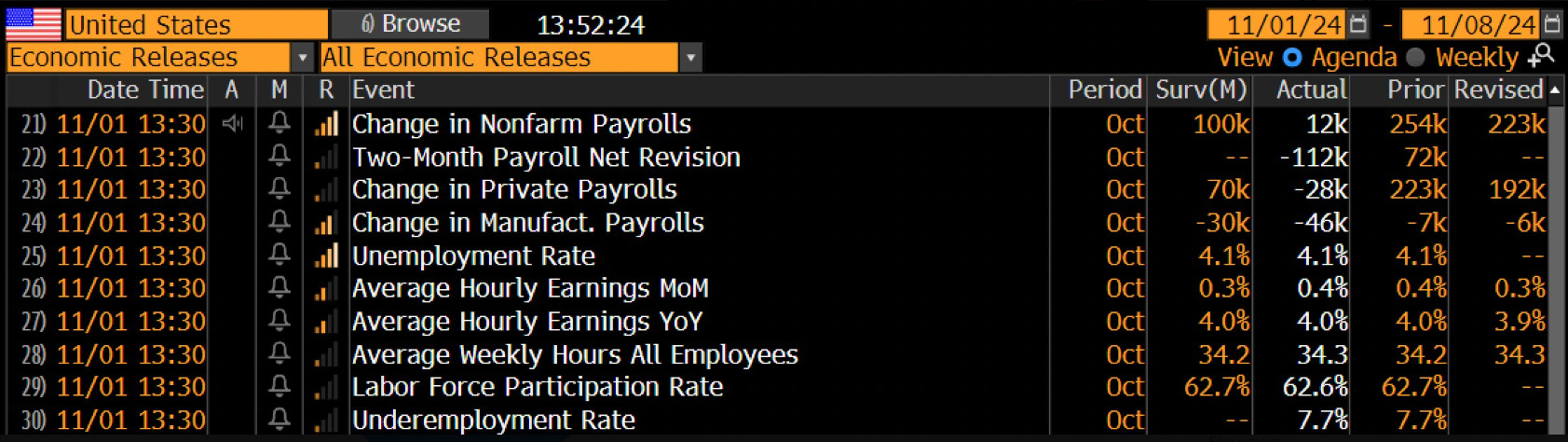

A quick touch on NFP.

Non-farm payrolls were down to extreme numbers in October, just 12k jobs added, however, the unemployment rate remained stable at 4.1% and average hourly earnings showed no cause of concern. The reading has now prompted a pricing of c.42bp of cuts across the November and December meeting from the Fed. Bear in mind that there has been c.100bp of cuts priced out of the U.S. over the last 6 weeks, pretty large turnaround.

Why treasury notes look short (to me)

Let me clear this up, my theory is based simply off of a Trump presidency.

In the below report I discussed a few of Trump’s policies, from tariffs to taxes.

Now, these policies are highly reflationary. Both tax cuts and higher tariffs lead to more money in consumer’s pockets, larger returns for businesses and of course…. increased spending. A reflationary regime will likely be sparked from:

Loose fiscal policy

Pro free economy

Tariffs

Bond yields are currently seeing bearish rates, almost in line with Trump’s probabilities of winning. Of course yields = growth expectations + inflation expectations + term premium, so the move isn’t idiosyncratic, knowing that Trump’s election will lead to tougher policy making from the Fed.

The “Trump effect” on markets in his previous term produced an overload of liquidity, but there were less eyebrows raised back then because inflation was a whole lot lower, averaging c.1.9% across that term. We’re now talking about a large amount liquidity entering an economy which is dealing with sticky core inflation, 3.3% (YoY). Rates will likely be held higher for longer, but I don’t think growth will be damaged because the policies that’ll be introduced will counteract the higher rates (in my opinion).

What my concern is for T-notes, is that the U.S. is seeing sticky inflation in “tight” fiscal and monetary policy conditions now, if Trump wins presidency, the reigns on financial conditions will be let go, creating a surge of loose conditions and further pressure on inflation.

The Federal Reserve will also lose some individuality in Trump’s term, he’s been mocking the decision making of Jay Powell in some recent interviews. He will be overriding their strategy and causing a divergence between monetary and fiscal policy, the loss of power from a central bank causes concerns for investors, a higher risk premium will likely be priced in. He may even go as far as replacing the current board members with ones who align with his economic policies or views on monetary policy, but that’s no guarantee.

There is a profound correlation between his presidency and risk-on assets, as discussed in a report I released a couple of weeks back. The fuel for inflation will be coming from all different angles, one being the increased investment into equities and crypto from the public (I’m focusing predominantly on equities in regards to reflationary potential because company earnings will grow and that’ll push larger investment).

What has the bond market had to say about it so far?

Implied volatility in Treasury yields has already risen to the highest since October 2023, that says it all.

Figure 7 is re-affirming my bias. Volatility = Higher demand for term-premium.

I hope you enjoyed, see you next week!