Why the Macro Still Works for Equities

Growth is holding up, policy is anchored, and rates are no longer doing the damage

Hey guys, after weeks of tariff headlines and geopolitical noise, equities are still sitting near all-time highs. Funny how all the big risks rarely end up mattering in real time.

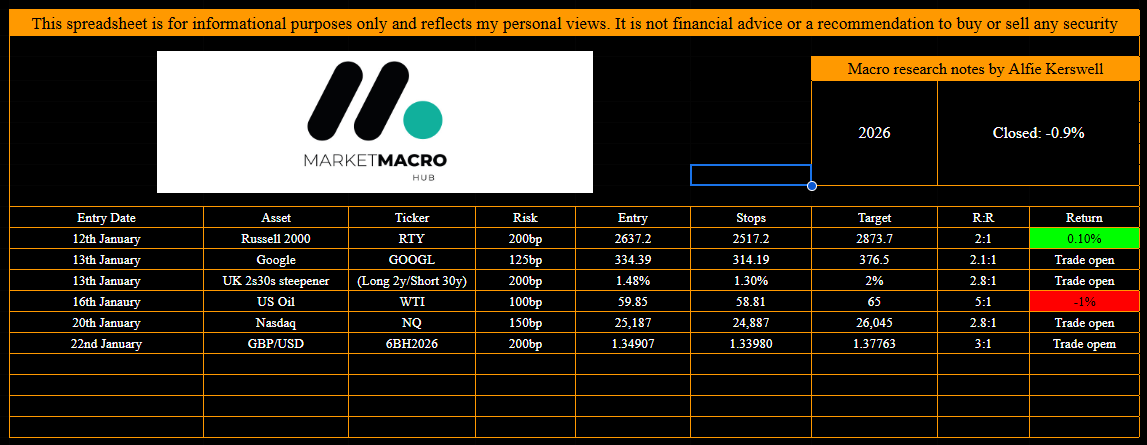

Trade updates below. Open positions are now floating well over +2.5%. I was a bit early on the RTY breakeven, tagged it almost to the tick, and then it went on to rally more than 3%.

This is how the trade sheet is shaping up:

Macro setup

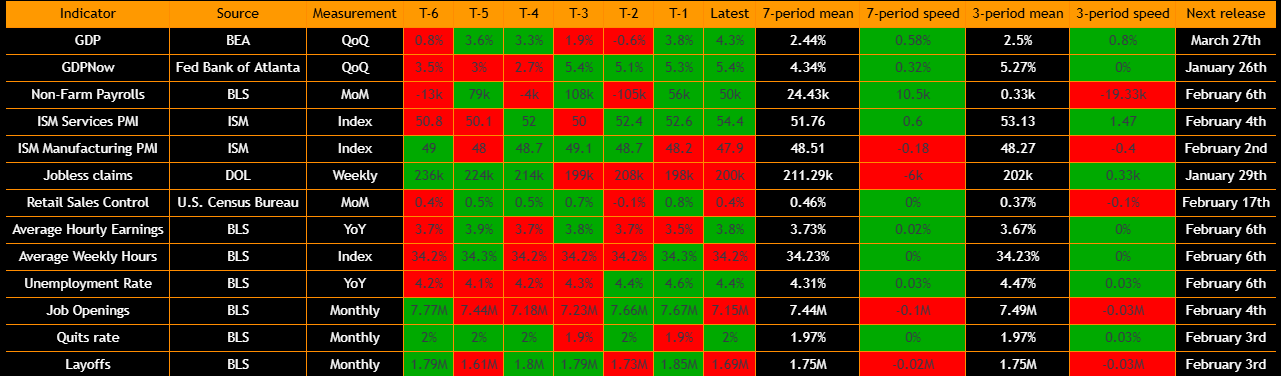

Stepping back, the current regime still makes sense for equities to grind higher, even if the pace is no longer explosive. Growth is holding up on a 3 and 6 month basis even with some softening in the very short-term labour data. Inflation pressures are present, policy expectations are fairly well anchored, and risk conditions are not flashing stress. The result is a market that can still move higher without needing a big repricing lower in rates or a weaker dollar to do the work. But ultimately, tail-risks here are building and have any marginal movements in them will cause outsized reactions in markets.

Yield curves are steepening through bear steepening, with both the 2s10s and 10s30s pushing higher. The combination of those two curves steepening usually reflects an economy that is still expanding. Real rates have been moving higher too (causing marginal pressure to equities), but not enough to say that we’re heading into a drawdown driven by restrictive rates.

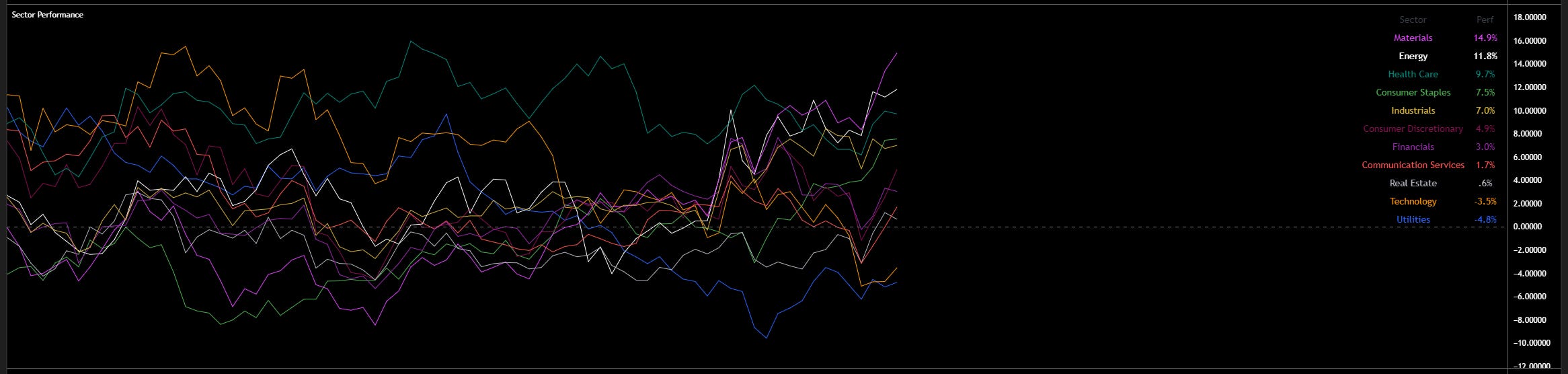

Equity leadership reinforces that positioning is shifting. Energy, materials, staples, and industrials are leading, and factor performance is tilted toward size and value. That kind of rotation tends to show a market that is pricing ongoing nominal activity. Labour market tail risks also look contained. While hiring momentum has slowed a bit, there is no clear signal of a sharp deterioration that would force a sudden repricing of growth expectations. If we start to see industrials and tech move up this ladder on a 3 month lookback, with the curves still steepening then there is less pressure on equities from rotation.

Inflation is the more complicated part of the picture and is pushing us into a reflationary regime (for now). Inflation swaps have been rallying since early January, and most inflation metrics are positive on 3 and 6 month bases. Breakevens and nominal rates have both been moving higher on a Z score basis, which tells you inflation expectations are being repriced up and adding pressure to nominals. At the same time, core and headline CPI are slowing on a 3 month basis but I’m yet to call take this as disinflaitonary pressures. I’m watching the 6m speeds closely as we move into February. If we see 6m metrics shift, I think we could be heading into a goldilocksregime will will create at least another leg higher for equities.

This inflation picture matters for equities because the pressure channel right now is valuations. As long as growth keeps pace with inflation on a medium-term basis, higher inflation expectations do not automatically translate into downside for stocks. The real risk would be inflation accelerating faster than growth, which would compress multiples. That is not what the data is showing yet. Growth has outperformed inflation for over a year and for as long as this setup persists then equities likely wont be dragged by higher inflation. But like anything, things can shift fast.

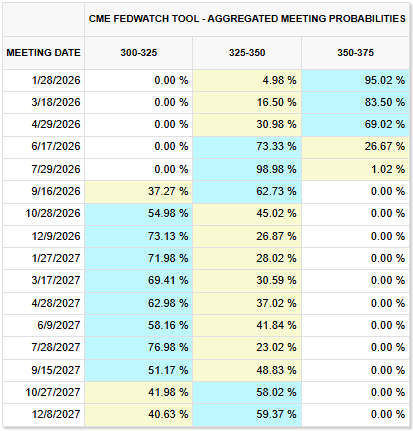

Policy expectations help anchor this regime. The market is pricing just under 50bp of cuts by year-end, split between mid-year and later in the year (June & Oct). The terminal rate is sitting around 3.25%. Importantly, cuts have actually been priced out over the past month rather than aggressively added back in which is why the USD had marginal upside pressure as STIR repriced.

This also tells you markets are not leaning on policy easing to justify equity upside. The thing you want to do most often is run attribution analysis because at different times, different things drive the market. For example, you want to know how reactive equities are to STIR, growth, inflation etc at any given time.

This is also why downside in STIR looks limited coming into the next couple of months. If growth and inflation both continue on their current path, the front end may start leaning toward a 35bp outcome rather than 50. At that point, most of the downside in STIR is already behind us and the path of least resistance becomes delivering at least what is already priced. A scenario where disinflation resumes while growth holds would be outright supportive for both bonds and equities but would still likely only see 50bp priced. A scenario where the terminal rate is repriced much lower would likely only happen if growth weakens meaningfully, which would be a different regime altogether. There is a scenario where we could reach 75bp, but ultimately that’d be growth driven rather than any disinflatuion pressures in my view.

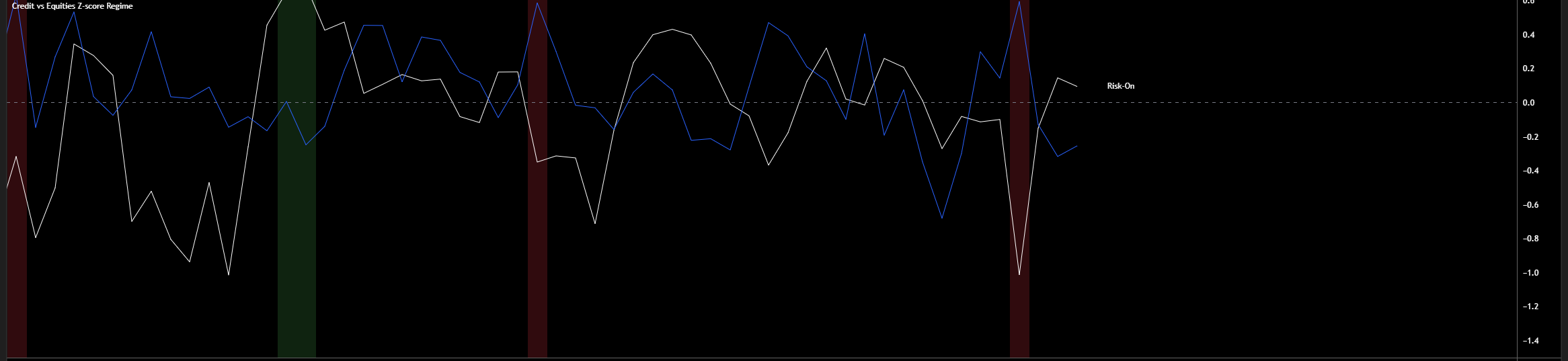

Positioning confirm the relatively easy backdrop. Put skew is moving lower (although we did see it blow out temporarily on Tuesday), implied vol is falling, credit spreads remain tight, and VIX is sitting near neutral levels. Equities are also outperforming credit on a Z score basis (I gave this indicator in the Substack chat), which tells you stress is not building beneath the surface... yet.

Breadth is another key support. Roughly 70% of S&P 500 stocks are above their 50d MAs, and equal weight continues to outperform. Momentum is rotating away from narrow growth leadership and toward the broader market. That is typically associated with slower but more durable equity upside (which is why I flagged that tail-risks hold more weight to equity downside than positioning). Small caps are lagging on a momentum basis and decoupling on correlation, which fits with a market that is cautious rather than euphoric.

For bonds, this setup argues for limited downside as I broke down above. With STIR expectations close to an inflection point and growth not collapsing, the asymmetry improves. You do not need a big rally in the front end for bonds to perform reasonably well, especially if inflation continues to slow on a medium-term basis.

FX ties the whole picture together. Despite tighter STIR pricing and higher real rates, the dollar has not responded meaningfully. Cross-sectional momentum in USD is negative versus equities, while correlation has risen. That tells you rates and fiscal dynamics are pressuring currencies without creating upside for the dollar. In other words, tighter policy expectations are not translating into a stronger USD, which removes a major headwind for global risk assets.

Putting it all together, this is a regime that still supports equity upside BUT at a slower pace. Growth is positive, inflation is firm, policy is tilting more restrictive than recent months, risk conditions are calm, and the dollar is not tightening financial conditions further. This is a setup to cap downside in rates, collapse the dollar, limit downside in equities, and keep the path of least resistance modestly higher rather.

Have a good one!

Why did you close the RTY trade? My RUT betas are ripping, up massively YTD and I don’t see any reversals yet