Why Oil Still Looks Short (to me)

A Deep Dive into OPEC Production Cuts, Refinery Activity, and the Looming US Election

Hey crew,

A rather quiet(er) week in markets.

US holiday on Wednesday so volume and liquidity was rather thin across markets.

It’s been a rather strenous period on my side but we push through regardless.

Today’s report is centred on my view for oil, explaining my reasoning, factors aiding my viewpoint and what I expect to see.

Macro Snapshot

No such thing as enough debt. Clearly.

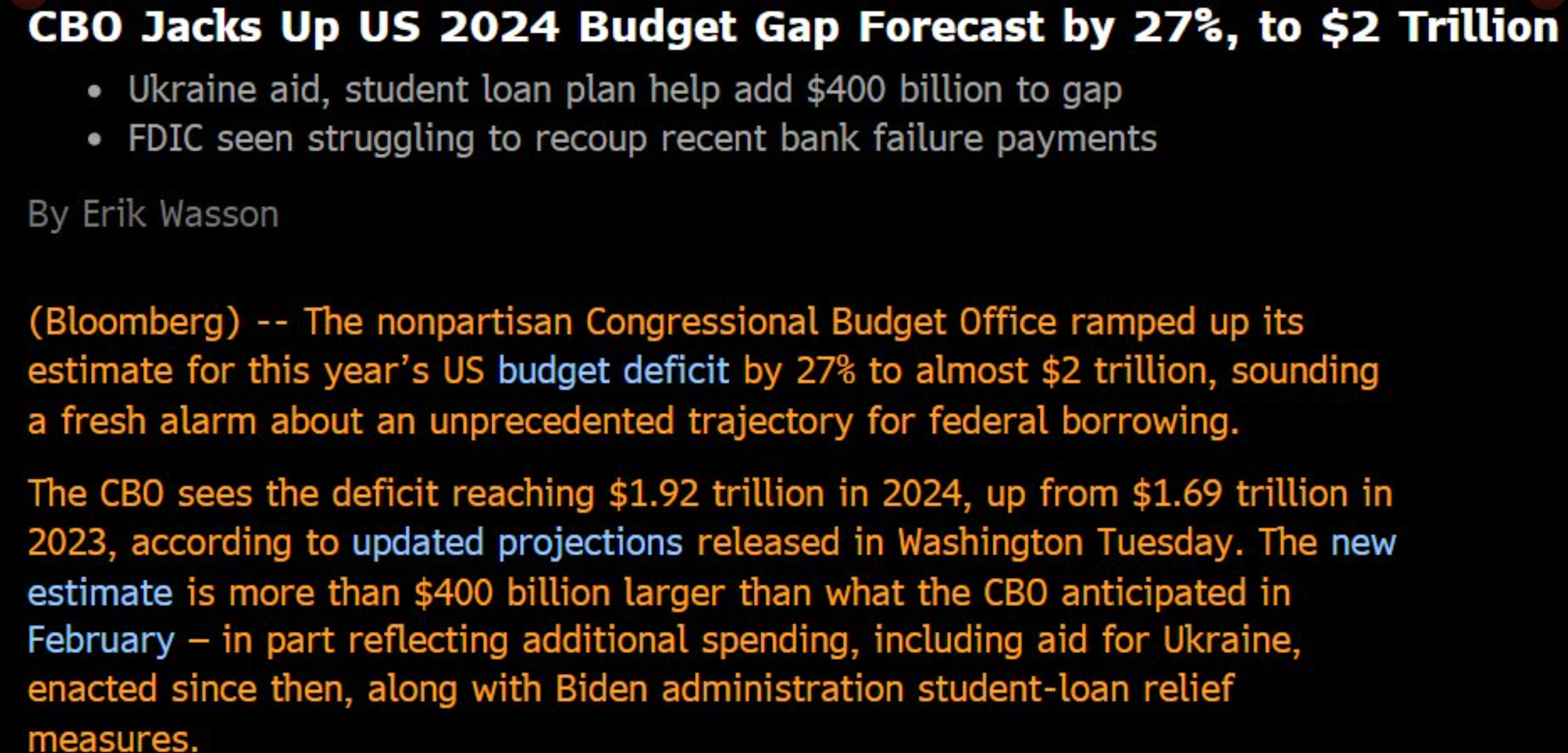

Earlier this week the CBO raised its forecast for the budget deficit to climb to roughly $2trillion.

Every now and then I wonder, is any of this real?

Because the way the US government handles its national debt is likened to that burning house meme. “No issues here, we’ll just our (debt).”

When observing Federal spending the most concerning figures are social security, medicare and net interest. As many have seen, especially leading up to this presidential election campaign, the Social Security fund is expected to run out of money by 2035 which is a real cause of concern for millions of American people.

Thought of the Week

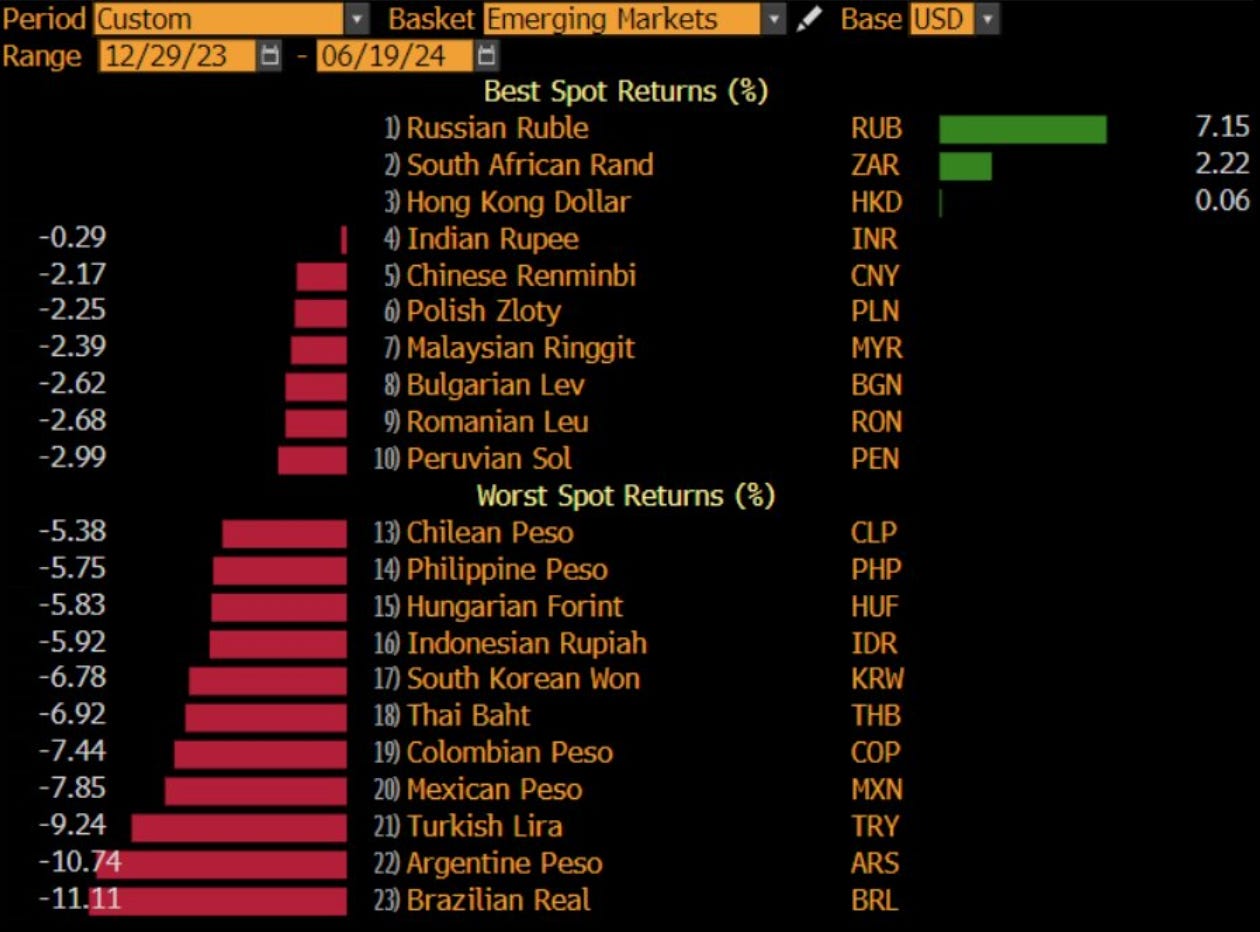

Following on from my currencies primer published this week I received this in my inbox:

Just the continued unwinding of the great carry, since the start of this year till date the best performing EM ccy has been the Russian Ruble, pretty impressive if you ask me.

Rates in Russia currently sit at 16.00%, but don’t get too excited, headline inflation is at 8.3%, meaning real rates sit somewhere around 7.7%, similar to that of Brazil & Mexico’s real rates.

Despite an ongoing war Russia’s currency markets seem to have faired well if you ask me.

Chart of the Week

It would be difficult, and I mean extremely difficult not to give this chart some spotlight this week.

The SNB surprised markets with a second cut for the year, lowering their base rate to 1.25%. The CHF took a 1% dive post SNB’s dovish cuts.

Still Bearish on Oil

For the past month I’ve kept away from commodity markets, mainly because there’s been too much activity here across macro markets notably currencies, bonds & STIRs.

During such moments I tend to cut back on the markets I focus on to get as much clarity as I possibly can on the markets of prime focus. However, last week I caught up with a good friend of mine who trades oil at a major oil house and our conversation, mainly his insights got me thinking, “It’s to take another swing at crude markets”.

Let’s start with the 10,000 ft view of what’s going on in crude markets.

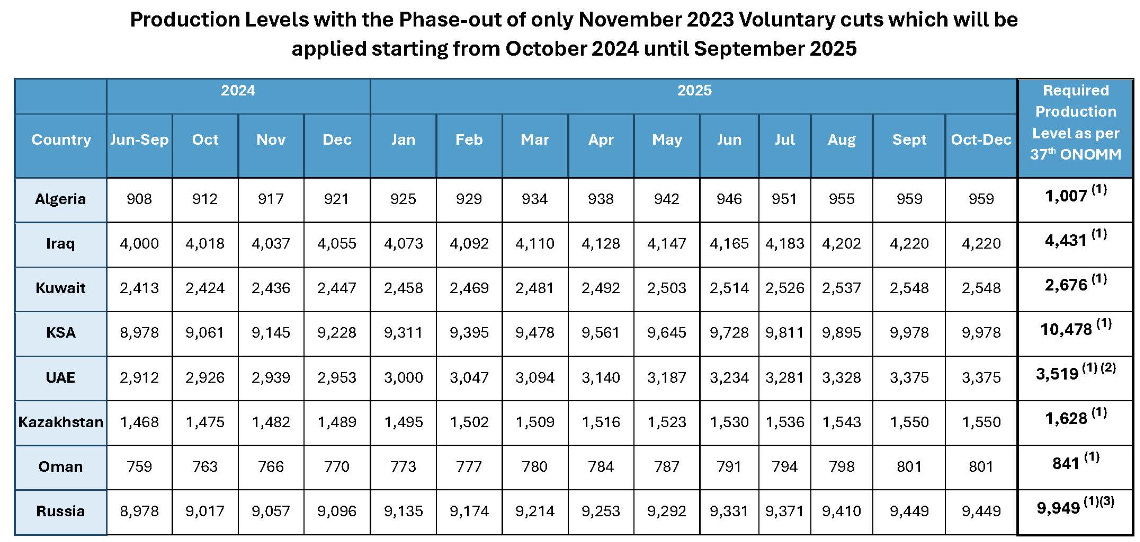

OPEC came out earlier in the month to announce that they would be extending the April ‘23 production cuts of 1.65 million barrels per day until the end of December 2025. The oil group also announced that they would extend the additional voluntary cuts of 2.2 million barrels per day, announced in November ‘23, until the end of September ‘24 and then gradually phase out the production cuts bringing more crude online.

Here’s how crude production levels are looking for the next 18 months.

Naturally, OPEC members weren’t happy with this; when you have capacity for more crude production but have a cap placed on your refineries you find some rebellion from countries who want to produce more crude. Iraq and Russia are perfect examples of this as well as many other Middle Eastern countries.

Here’s my take on crude dynamics.

No.1, I’m still bearish on crude prices, despite the recent rally to $85.00 on Brent and $81 on WTI my view is bearish on the commodity for the following reasons.

Crude oil prices have surged recently due to a confluence of factors. The return of geopolitical risk premiums, coupled with the EIA's report of a larger-than-expected drawdown in crude stockpiles by 2.5 million barrels last week (compared to analyst forecasts of 2 million), has sent a jittery market higher. The approaching hurricane season adds another layer of uncertainty, potentially impacting production and transportation in the Gulf of Mexico.

Now ofcourse, these are all upward price pressures on the commodity, but the underlying trend continues to point to lower prices, here’s why.

Since April 2023 OPEC have taken over 3.85 million barrels per day offline; so now that the demand outlook in Asia appears to be improving all that will take place is OPEC countries releasing all of the crude that was being stockpiled in their spare capacity.

As a reminder, when OPEC announces production cuts, that oil is not being brought to the market, nor used, so that cut in production actually adds and replenishes the spare capacity available. Think of oil production cuts as increasing oil reserves hence adding further stability to oil markets and prices. This is precisely why OPEC cuts are usually bearish or neutral for crude prices, rarely bullish.

So with the onset of improving demand in Asia, the market knows that there’s more than enough spare capacity to meet the market’s demand. Furthermore, we know that market’s usually overshoot the ‘rebound’ of an economy/region, and this case is most likely no different.

The recent spring refinery maintenance season adds another wrinkle to the bearish outlook. We have just coming out of the spring maintenance season, where refineries come offline to do maintenance work on their facilities.

Now what’s pointing me to look bearish is that when a refinery goes offline, (let’s say for 10 weeks) usually they would come back online and resume purchasing crude at the same rate they did prior to going offline. Weaker demand is causing them to be more cautious, and they're currently buying less crude than before the maintenance period. This signals a potential disconnect between supply (increased post-maintenance capacity) and demand, potentially putting downward pressure on oil prices.

Hence why oil markets have fallen into contango.

For my non-oil people, contango is simply a situation where the futures price of a commodity is higher than the spot price. So in oil terms here’s how this is worsening my outlook for crude.

When the market is in contango refineries are incentivised to wait and hold onto crude until future dates where the prices are more favourable, and to do so they put this crude on floating storage (large crude tankers) which act as a warehouse for crude oil. Once again, the issue here is current demand— when speaking with a few people much more knowledgeable on the matter than myself they mentioned that participants are still trying to sell May crude in June simply due to the lack of demand.

The upcoming US election adds another layer to the bearish case for oil. With gasoline prices a major concern for voters, President Biden is likely to face significant pressure to keep them in check. A key tool at his disposal is the Strategic Petroleum Reserve (SPR), a stockpile of emergency crude oil reserves. If WTI prices climb above $80 a barrel – a politically sensitive level – the President could authorise the release of oil from the SPR, increasing supply and potentially driving down prices. This potential government intervention adds to the existing headwinds for oil: weak refinery activity and overall lackluster demand.

Now, in regards to my timing of the short play I will be monitoring the upcoming weeks of EIA data and US crude inventories alongside the price level of brent crude. The $86 per barrel mark is where the risk/reward becomes attractive for shorts given the current price range.

Targets are always a hard one when shorting a commodity void of technical influence, I know I offended a few technicians there, oh well. The point being, with the fundamental drivers of crude being geopolitical risk premium, supply/demand dynamics and OPEC updates, putting a base price target becomes increasingly challenging— in such cases I tend to monitor a position with an open target, if presented with new evidence causing me to shift my perspective I exit the position. Let’s be honest, for the most part, a ‘target price/level’ when trading oil is subjective to the individual behind the screen as in for most markets.

Even with these favorable fundamentals in place, markets have a knack for defying expectations. As we head into the summer travel season, known for its volatility, I remain cautious not to get caught amidst market rips.

A brief yet comprehensive view of why my biases lean towards brent shorts.

I hope you enjoyed this read MMH,

Until next week guys.