Unpacking Trump’s Early Strategy and Argentina’s Default Countdown

Breaking Down Trump’s Initial Actions and What They Mean

Hey MMH readers!

Started the year with some serious momentum, the compounding effect will propel this further.

If you haven’t already, set out a game plan out for your 2025 goals, don’t just aimlessly write them down.

The question you need to ask yourself is, “Is the work I’m doing now moving me closer to my goals and can I be more efficient in another area/task to speed the process up?”

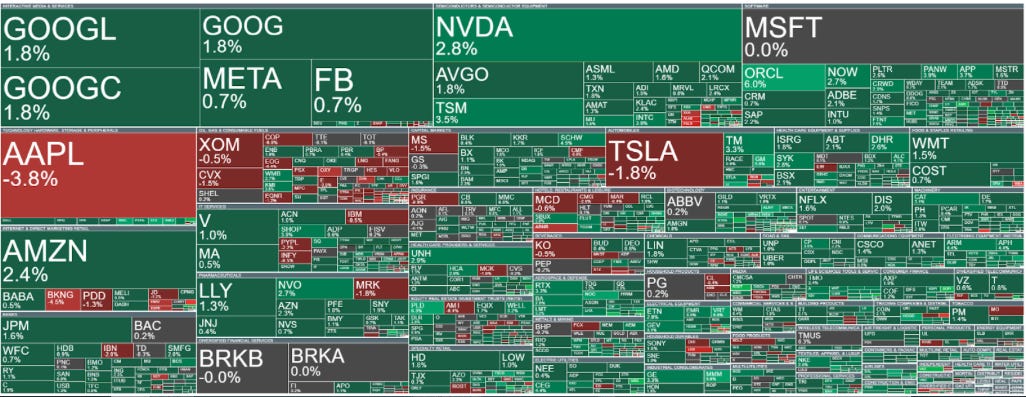

Anyway, back to markets, Trump has finally taken office!

Let’s see what the market will unpack for us.

Macro watch

Look, it’s pretty obvious what every trader is watching closely towards right now, the big T word.

Tariffs.

In Trump’s inauguration speech he didn’t explicitly mention tariffs, his focus was more on immigration (he actually announced the introduction of a state of emergency at the southern border). The 2Y and 10Y both gapped lower at the open on Tuesday, the yields quickly gained back their losses, while stocks were green on the following day.

A 10% tariff on all Chinese goods to the U.S. seemed signed off until his remarks on Thursday where he stated that he doesn’t want to have to impose tariffs on China… Underdelivering tariff promises already?

While the 25% on Canada and Mexico (expected February 1st) seem pretty set in stone. Although the Euro dodged a bullet in his inauguration speech, they will likely be hit hard (in my opinion) because they’re running an enormous deficit with the U.S., which Trump aims to fix.

Market mover

Some focus on EMs, Moody’s has upgraded Argentina’s credit rating, citing the government’s efforts to stabilise its finances, which have reduced the risk of defaulting on debt obligations. The ratings agency raised Argentina’s score from Ca to Caa3 and improved the outlook from stable to positive.

Yes, the risk is reduced but are we going to see a 10th sovereign default? Based on their track record and the challenges they’re currently facing, yes.

The move up in rating is positive, but still very poor. The challenges that Argentina are facing are multi-faced:

Hyperinflation - The country faced a 140% YoY inflation rate for 2024.

Ultra high debt levels - They are carrying a large amount of foreign debt, most is denominated in U.S. dollars so the burdens has deepened at the USD has gained traction and the Peso has fallen off a cliff.

Political uncertainty - A volatile political environment, including frequent shifts in economic policy and contentious elections, has deterred investment and contributed to market instability.

The country has seen so many defaults that the repercussions seem to have lower effect than in the earlier cases. Put it this way, if you have 0 faith in a country, it can’t get any lower so the consequence of another default is bad, but not AS bad as another country may face.

Trump’s Early Strategy

Firstly, freezing the hiring of Federal civilian employees has got me thinking. Depending on the actual contribution that these jobs had previously on NFP, we may see lower figures but most of all (once again depending on the number affected), disinflationary pressure.

In Figure 5 below, you will see that the jobs frozen account for the smallest proportion of Federal employment in the BLS figures. I’m more focused on percentages, even if they account for just 20% of the figures, to put this on freeze will surely cause some decent impact on job hirings and some (not a lot of) disinflationary pressure.

Another case for disinflationary pressures is that Trump has announced the resumption of drilling permits and aims to solidify the U.S.’s dominance as a leading oil and gas producer. Of course, higher supply = lower prices, but how much will this really weigh in on inflation?

For reference, check out Figure 6 below. It shows how much energy is contributing to CPI or should I say…. not contributing.

Once again, it really depends on the amount that the oil prices are affected by, but nonetheless the thesis is the same, disinflationary pressure. Whether it’s disinflation by a small or large margin it doesn't matter, the fact is there is no upside pressure in this policy imposed by Trump. He didn’t stop there with his dovish policies/comments. On Thursday, Trump said “With oil prices going down, I'll demand that interest rates drop immediately”, claiming he knows rates better than the Fed. It does raise some level of concern for the independence of the central bank, although he can’t actually directly cause the Fed to act, but rather force them into a position of acting (which honestly, is not much different).

So we’re painting the picture, once again for a lower USD…

In my report on the 10th January, I discussed shorting USD/JPY, many reasons discussed, have a read below:

Q1 2025: Undervalued Cuts, Ambitious Tariffs, and China's Counterstrike

The only way I was seeing the dollar higher was in the scenario that Trump came out in his inauguration and was even more aggressive on his policies, but he wasn’t. Also, with a little help of the BoJ hiking 25bp to 0.5% the trade is c.2.4% up, see in Figure 7.

Sorry for any USD bulls, it doesn’t get much better. Trump seems to be underdelivering on his tariff plans, let me explain below.

Pre-eelction, Trump was aggressive in his comments about tariffs on china, stating a “minimum of 10% on all Chinese goods” as part of his protectionism act. However, on Thursday in his speech, he said that America “has one very big power over China, and that is tariffs, and they don’t want them, and I’d rather not have to use them, but it’s a huge power over China”.

Key take away from the above - “I’d rather not have to use them”. So, were tariffs on all Chinese goods just a threat to make them behave in a way where Trump has mighty power? Besides the point, even if Trump did impose the tariffs he said he would on China, they were already priced into the dollar so it’d take more extreme tariffs to have moved the dollar higher.

Seems like under deliverance on China’s tariffs, for now, which is dollar negative.

However, he has stuck to tariffs imposed on Canada and Mexico, which are 25% on all goods. This tariff is likely coming into place on February 1st, which is a significant move because these two countries are two of America’s three largest trading partners. Last year, imports to the U.S. from Mexico amounted to over c.$470bn while imports from Canada were close to c.$420bn. Also, Canada sends between 75-80% of its exports to the U.s> and in GDP terms, that contributes for over 20%. While 80% of Mexicos exports head to the U.S. but this accounts for a smaller 7% of their GDP. There may be three losers in this situation, both Canada and Mexico may impose retaliatory tariffs on American goods.

Honestly speaking, I think it’s time to double down on dollar shorts. A real hand has been show for dollar’s weakness with so many macro events helping, just wait until rates are repriced (which is round the corner) and we will see a further unwind of the dollar.

Have a great trading week!

Honestly, looks more like Trump is just using tariffs as negotiation tactic, I wouldn't be surprised if February 1 becomes March 1, then April 1 and so on. At some point maybe some country will step on his toe and he will roll out a quick emergency tariff but to then walk it back as soon as he gets what he wants right away, like what just happened with Colombia.