The Stagflation Label Is Wrong

Why The 2022 Comparison Doesn't Hold

So much talk on the reflexive comparisons to 2022 are everywhere right now. Stagflation is the consensus fear trade (and I get why to a degree). You have inflation above target, a Fed that can’t cut with ease, and a growth picture muddled enough to make people nervous. On the surface the it look similar but we are in a VERY different starting place, I will go more into this later in the report.

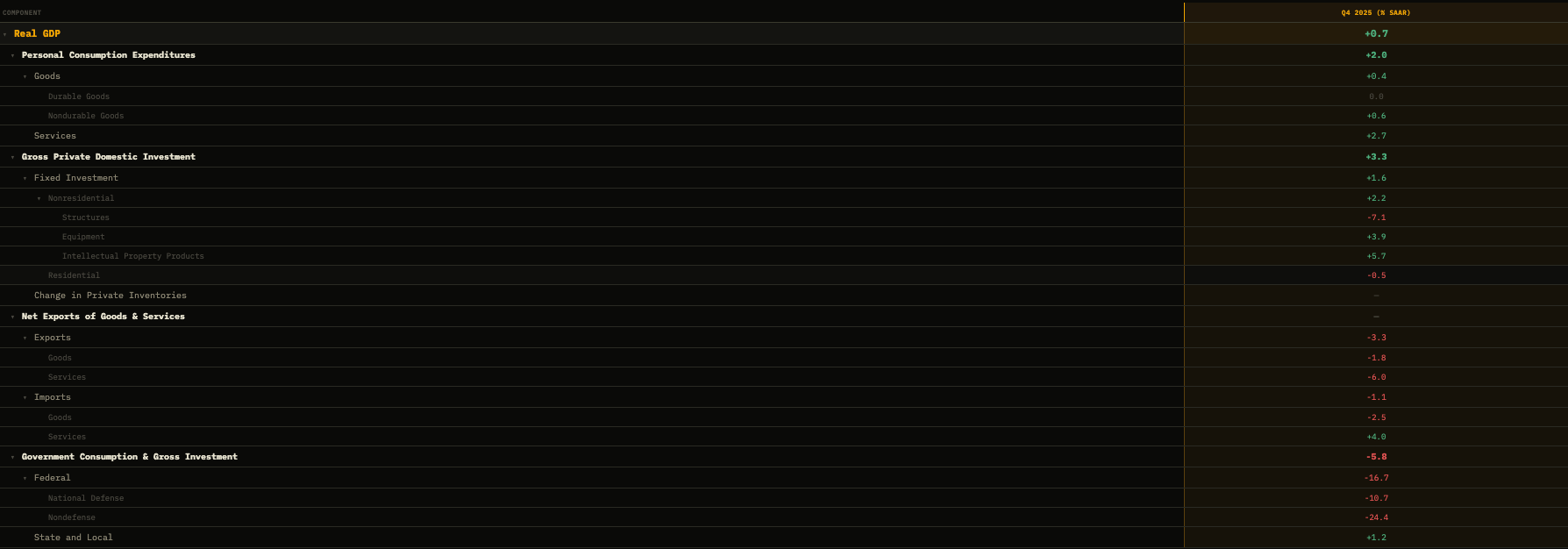

The recent real GDP print sparked growth fears/recession talk, but the headline figure is distorted by transitory composition effects. Strip out the government and trade distortions and the private sector is in reasonable shape. Consumers are STILL spending, business investment in tech and equipment is holding up, and forward-looking demand indicators across both services and manufacturing are pointing higher (you’d be seeing these roll over with momentum if there was some sort of growth shock was on the way). The economy is not running hot by any means, but it is also NOT breaking into stagflation.

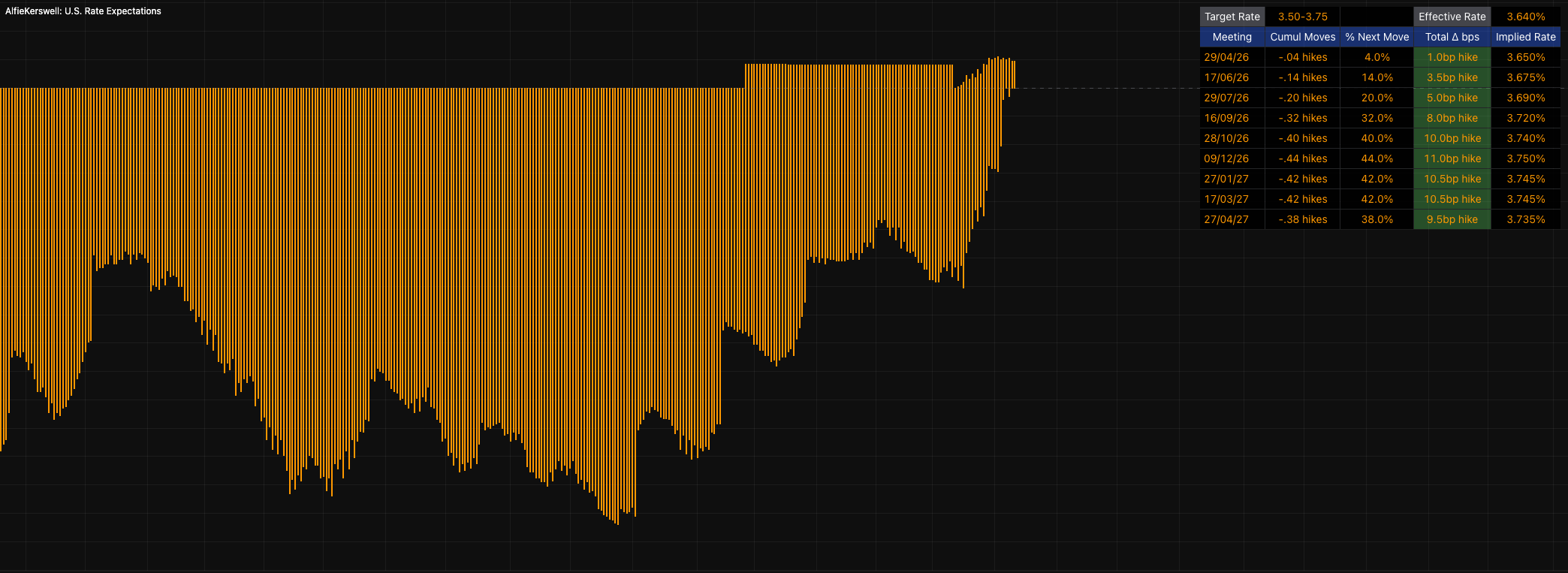

The Fed is effectively stuck at the minute but this could quickly change before their April meeting. They’re unable to cut because of this inflationary tail-risk from oil, and unwilling to hike (in my view anyway) because the labor market and growth inputs are sufficiently not powerful enough to survive hikes. The markets are pricing hikes but this is still blown out of proportion in my view. As QUICK as markets can price hikes is just as QUICK as they can price them out.

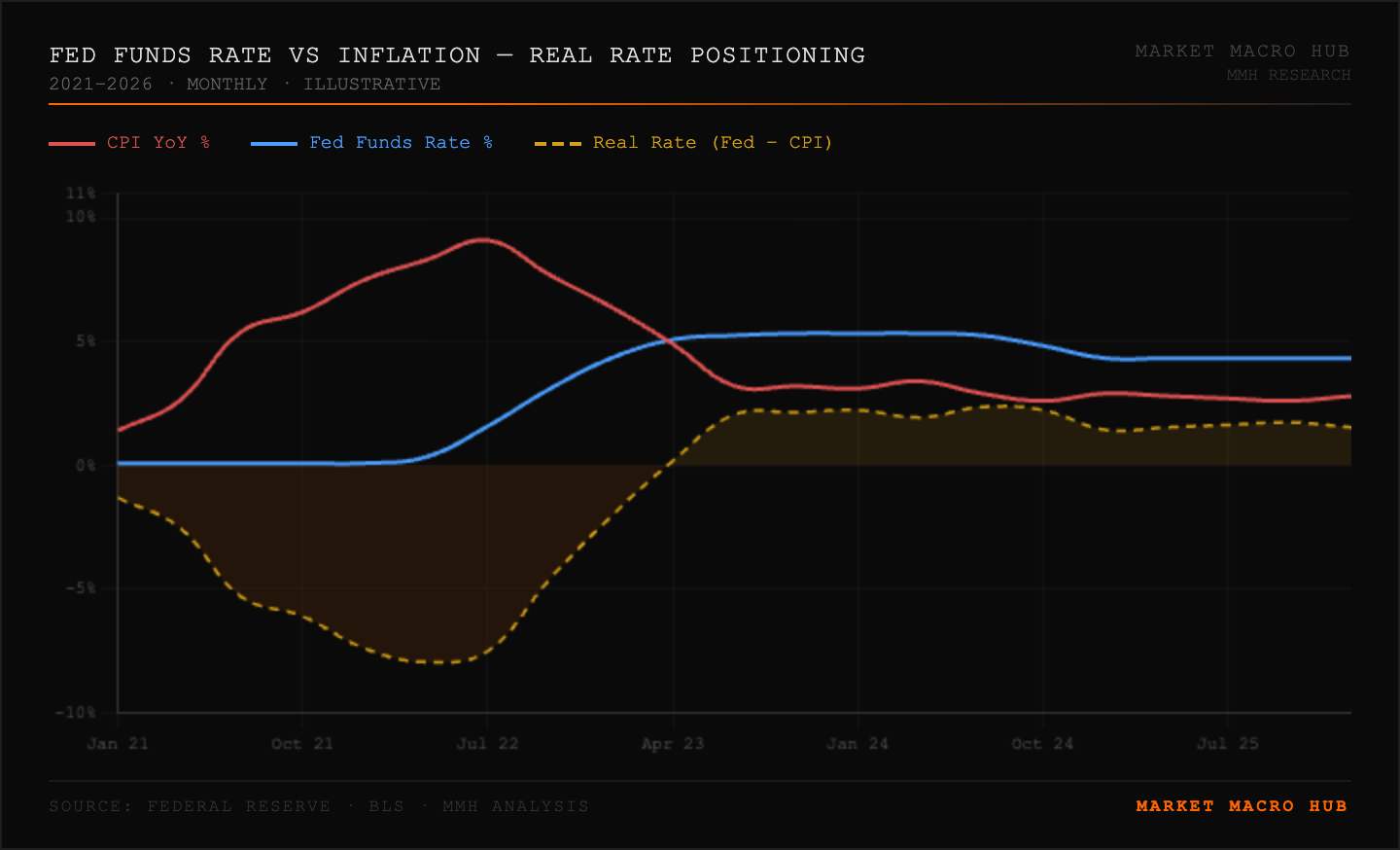

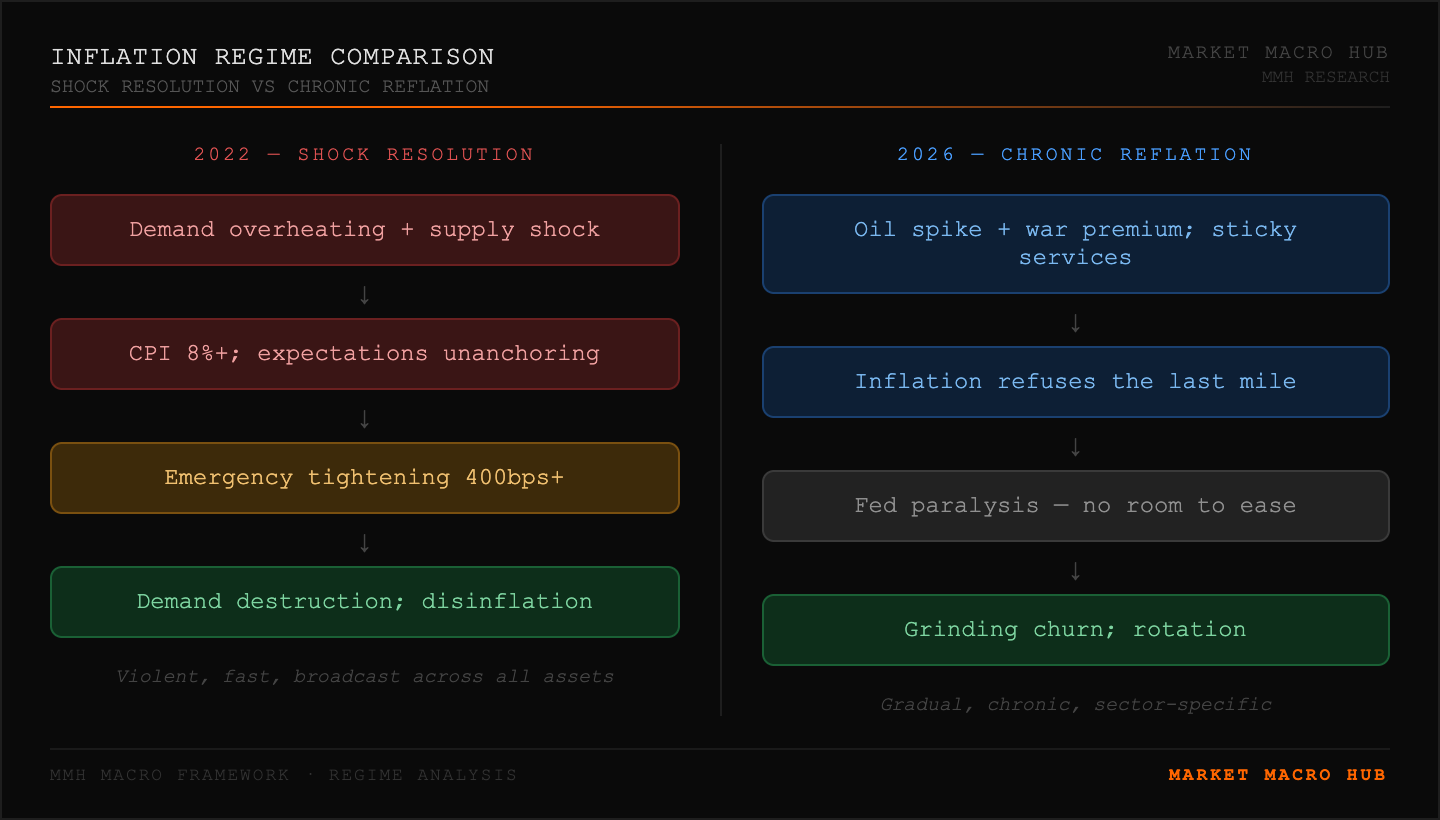

This is where the 2022 comparison completely breaks down. In 2022 the Fed was MASSIVELY behind the curve. Real rates were deeply negative, financial conditions were extraordinarily loose, and the Fed was STILL buying assets while inflation was running at 8%. The tightening cycle started from a position of maximum stimulus into maximum overheating. We have NOT got this starting point.

Today rates are ALREADY meaningfully restrictive. The Fed is NOT behind the curve on inflation in any comparable sense (you could say they’re behind, but relative comparison it’s nothing like it was). They are sitting with rates above neutral with inflation above target. The question is whether they can ease at all, and the answer is probably not YET, which has been reflected in the forward curve.

The Fed being forced to hold rates is NOT the same as emergency tightening, and conflating the two leads to the wrong conclusions about asset pricing.

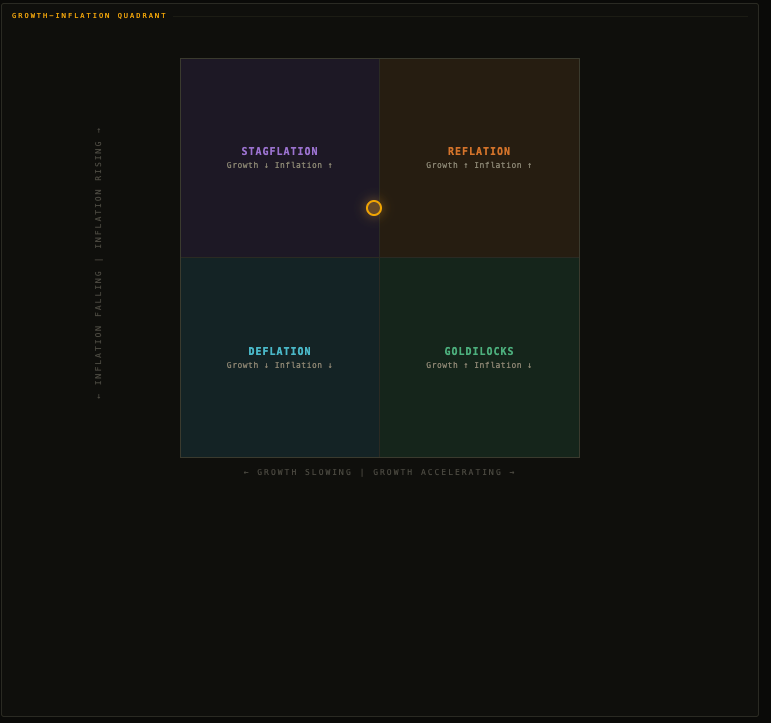

I’m running some models on a terminal, iterating them as fast as I can to push out as much value to you guys as possible. My regime quadrant falls into this stagflaiton box but VERY close to reflation, it was tilted by the oil shock and the lack on confirmation of from both sides about a de-escalation, meaning oil stays in this higher range for longer, but this is just a regime model and NOT something I’d set a thesis on, but it’s definitely accurate in the fact that it’s still on the edge of reflation.

Considering that the US are in a full battle with Iran AND the market is pricing stagflation, ES is only 7% off ATHs. Now, given regime-expected returns for stagflation, repricing of the forward curve AND a war with Iran, I think the index is holding up fairly well and reflects supportive growth in the underlying economy, which once again supports us moving into a reflationary regime.

Regime expected returns:

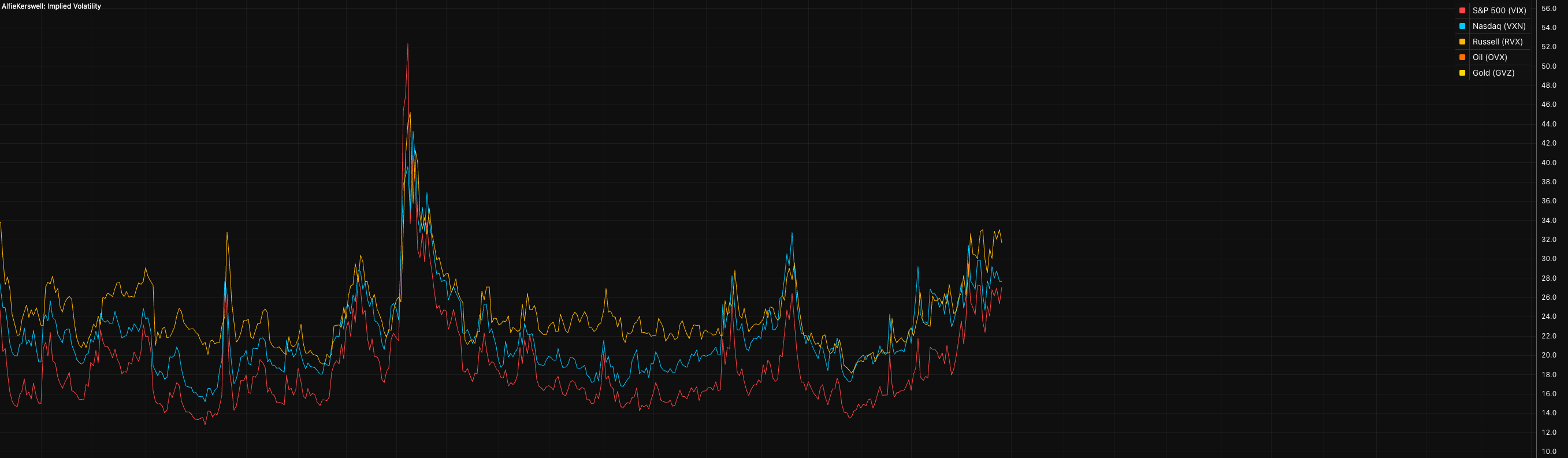

There’s still a LOT of tension underneath the surface in equities (I laid this out in the previous report, check it out). Implied vol is still at an extreme and it only takes ONE confirmation to unwind this all, we’ve seen how reactive equities are on these types of headlines, we had ES move well over 3% wihtin 5 mins on a headline about Trump saying there was an agreement being spoken about/talks were happening (whether true or not).

The moves have mean reverted but when there is somehting official from both sides, you’d expect to see the same outsized moves as hedges unwind and this implied vol moves lower meaningfully, it’d be a cross-asset compression of vol in my view.

Another input that makes the current setup push toward reflationary rather than continued stagflationary is the demand component. Stagflation requires growth to be actively deteriorating while inflation rises. The leading demand indicators, forward orders in both manufacturing and services, are NOT suggesting deterioration.

If that resilience is confirmed over the next couple of months, you have an economy running at trend with inflation ticking higher on the energy transmission. Nominal growth reaccelerates modestly even as real growth stays moderate.

The current read across stocks, bonds, and the dollar shares surface similarities with 2022, with equities down, bonds down, and the dollar up. But the regime underneath is ENTIRELY different. The most common regime following stocks down, bonds down and dollar up is actually reflation, which would be much more aggressive vs 2022 as the underlying growth and liquidity in the system is NOT supportive of prolonged stagflation in my view.

A lot of the tension underneath the surface in the current equities setup is also pinned by the forward curve, which looks very unreasonable to me. It is beginning to price about a 50% chance of a hike this year. But this is all on the assumption that the current state of the market remains throughout the next 2 months at least, and we have seen the opposite of that with less attacks and more signs of wanting talks and de-escalation. It’s also common knowledge for central banks to look through energy shocks while monitoring tail-risks.

The instinct to reach for 2022 as the reference frame is understandable because you have inflation above target, a Fed that CANNOT cut with ease, and a growth picture that is muddled enough to make people nervous (particularly through the labor component). BUT, the inflation that persists is not the violent broad-based surge of 2022.

If the war prmeium gets unwound across all assets, which has evident signs of being a potential (as I mentioned above, negotiations are being mentioned), then we go back to focusing on the transmission of thse oil prices into the economy, which is still a very different story to 2022…

What that means for risk assets is also different from 2022. In that year the valuation reset was brutal because assets had been priced for near zero rates, and the duration hit to equities, bonds, and growth assets was violent because the starting multiple was so stretched.

Today valuations are not cheap by any means, but they are also NOT priced for a zero rate world either. The market has already adjusted to a higher for longer framework in its baseline. Rotation still matters A LOT here.

In 2022, there were also MANY more shocks to posotioning. The shocks we’ve seen through the last 12 months have all been geopolticial shocks (particularly through Trump), which is a complete different tail-risk to a direct inflationary shock.

Today the market is ALREADY sensitised to inflation risk. The narrative of sticky inflation, higher-for-longer rates, and Fed paralysis is consensus and definitely NOT a contrarian call. That changes the dynamics of how the regime unfolds. In 2022 every inflation print was a fresh shock forcing incremental repricing. In 2026 a reflationary regime would be a confirmation of something already partially priced, which means the moves are likely to be more gradual and more sector specific than the brutal across the board de-rating of four years ago.

I still remain with the view that I want to get short USD and long equities.

This is NOT 2022 repeat. This is a different animal entirely, and trading it like the last cycle will leave you positioned for the wrong risks at the wrong time.

Thanks

Alfie