The Role of Central Banks In Global Macro

A deep dive series on the role of CBs, their functions and implications on markets

Hey guys,

Life’s good.

Living in the moment, zoned in, but ever present of the future and what’s ahead.

Thanks for waiting a little longer for this report.

A focused state of mind worth entering.

In this series of reports, I’ll be delving into a topic many traders, investors and market participants know little about, mostly scratching the surface level with. That is the role of central banks in global macro, their tools, functions and wider affect on markets.

As always lend me your attention:

The Role of a Central Bank

On Wednesday in Sintra, Portugal the ECB concluded a two-day forum discussing all things central banking, from monetary policy, to the ideal balance sheet size, and the current policy trajectory of the major central banks globally.

What a time to dive into the importance of these powerful institutions.

Let’s start big picture.

What is a central bank and what is its mandate?

Put simply, a central bank is a financial authority responsible for the policies that affect a country’s supply of money and credit. It doesn’t get much simpler, we’ll delve into the different tools within a central bank’s arson which assist in controlling money supply and credit, but for now, let’s look at the mandate for the Fed, ECB and BOE.

It’s worth noting that each central bank has its own duty and mandate.

When searching for the simplest explanation for the Fed’s dual mandate this extract from 2013 summed it up better than all other recent statements.

The Federal Reserve Bank

“The Board of Governors of the Federal Reserve System and the Federal Open Market Committee shall maintain long run growth of the monetary and credit aggregates commensurate with the economy’s long run potential to increase production, so as to promote effectively the goals of maximum employment, stable prices, and moderate long-term interest rates.”

European Central Bank

“The primary objective of the ECB’s monetary policy is to maintain price stability. The ECB aims at inflation rates of below, but close to, 2 percent offer the medium term.”

Bank of England

“The Bank of England exists to ensure monetary stability and to contribute to financial stability.”

Short and simple. Now I know this may be very familiar for most of you, but nothing works better than going over the fundamentals. Let’s take a look at a few of the tools used by central banks with the exception of interest rates since this is a topic I have covered extensively.

Central Bank Tools

Reserve ratio:

The reserve ratio requirement is the amount of reserves a central bank makes mandatory for commercial banks to hold in customer deposits. This is usually a percentage of customer deposits.

In the States the reserve ratio requirement is 10%, meaning that 10% of customers’ deposits must be held as reserves in every commercial bank in the U.S. So if JPM Chase bank has $2tr in customer deposits they would be required to hold $200b as reserves with the central bank.

If you haven’t pieced two and two together, let me explain how this tool is used by central banks and how this supports monetary policy. By the central bank setting the reserve ratio requirement, they indirectly affect the money supply within the economy. Raising the reserve ratio forces banks to keep aside cash, and restrict their lending to the public contracting the available money supply. The opposite is also true, when the central bank reduces the reserve ratio banks can now increase the money supply via lending.

Although this tool can be extremely effective a number of central banks steer away from continually adjusting the reserve ratio such as the Fed, BOE and ECB. However, the PBOC is renowned for using this policy tool as a key mechanism within its monetary policy approach. Look at Figure 1.

Over the past 12 months China’s reserve ratio, also called the cash reserve, has dropped 50bps. Prior to this you probably didn’t know why, or what adjustment the PBOC were trying to make, but now with the understanding that a lower cash rate results in increased bank lending we can put together that this was an accommodative monetary policy act to stimulate bank lending by reducing the amount required to be held as reserves. Of recent, we’ve also seen China cut a number of its interest rates to support this accommodative move.

Open Market Operations

Open market operations should be a term familiar to those who bought the Four Foundations of MacroFX, which is scheduled to go under reconstruction, more material, content and value, I’ll keep you updated as and when.

To put it simply, OMO is the process of buying or selling government debt in order to influence the money supply within the economy and effectively steer both short-term and long-term interest rates. Within open market operations, you have two umbrella’s temporary operations and permanent operations.

Here are the key concepts behind both operations according to the Federal Reserve Bank of New York:

Temporary open market conditions involve repurchase agreements that are designed to temporarily add or drain reserves available to the banking system.

Permanent open market operations involve the buying and selling of securities outright to permanently add or drain reserves available to the banking system.

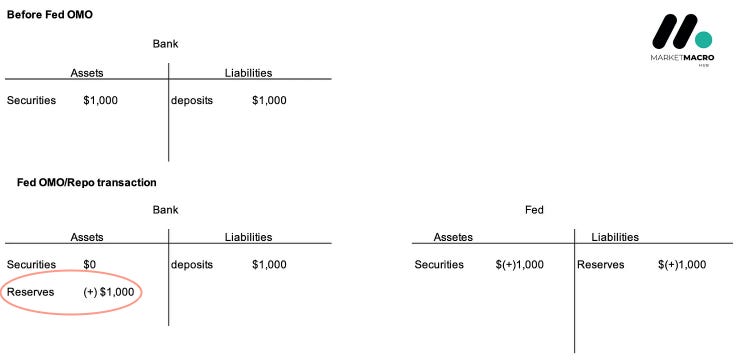

An example of temporary open market conditions would be repurchase agreements, also referred to as “RP’s” and “repos”. Put simply repos is a collateralized form of lending which the Fed utilises to influence the money supply available within the economy.

In a repo transaction, you have two market ‘agents’ or parties, one is the borrower who sells their government debt to another party for a certain amount, with the agreement that the borrower will purchase the securities at a certain date in the future.

The usual tenor of repo transactions is overnight, but they can span all the way out to 65 business days according to the Fed.

In the example, the interest charged for this short-term form of borrowing is the spread between the cost of the German bunds and what the borrower has to pay in order to repurchase the bunds. So the spread between the purchase and repurchase agreement is the interest charged.

So in this scenario, if the Fed were to conduct OMO (open market operations) with the intention of increasing the money supply, they would be the buyer in this example. Purchasing government bonds increases bank reserves’ accounts held at the Fed, so the bank can now lend out excess reserves by creating credit since bank reserves never enter the real economy.

Figure 3 shows a visualisation of what happens to the bank’s balance sheet before and during a repo transaction between the Fed.

As you can see, all that happens is an exchange of reserves from the Fed to the Bank, securities out, reserves in.

Remember, out of all the Federal and central banking tools we’ll uncover together, it all boils down to two things. Increase or reduce the money supply. It may be an oversimplification of these complex mechanisms but it’s true, the goal of each tool is to influence the supply of money and hence control inflation.

We’ve covered temporary OMOs it’s time to dive into permanent (POMOs.)

A good way to start off is to really differentiate POMOs from their opposite. As we’ve broken down, the majority of temporary OMO is done via the repo market, which is a way to influence short-term interest rates and liquidity. POMOs take on a different approach, this tool is USD to steer the longer-term factors (interest rates) in line with the Fed’s mandate; this process is an ongoing market operation.

It’s important to not get OMO mixed up with quantitative easing/tightening as those are completely different operations. The main difference is the size and scale of QE/QT which is a more unconventional tool involving the large-scale asset purchase of securities, OMO is typically a much smaller size compared to QE/QT.

This was the intro to the deep waters of central banking tools and policies. Next, I’ll explore currency intervention, the actions that warrant central bank intervention and examples of successful and unsuccessful interventions.