The Regime Trade Explained Pt.2

Analysing the cyclicality of financial markets under diverse market conditions.

Hey crew,

Glad to be at it again.

Everyone’s talking and panicking over the debt ceiling; don’t be one of them, rather an observant macro speculator deciphering what effect that’ll have on markets.

Always be neutral headed and in times of extreme sentiment, be that fear or greed, you could be approaching an inflection point in the markets.

We’ll be diving into some more concepts following on from last week’s piece:

Let’s get into it:

Spotting A Market Regime

It’s so easy to hear the term, ‘macro regime’ and automatically start wondering what that term actually means, or how you can build a framework for analysing and spotting different market regimes.

So let me give you a rundown.

There’s key economic metrics I look at to help shape what regime I believe we’re in. Those metrics are:

GDP YoY, QoQ

CPI YoY

Unemployment

Interest rate level

That is the basic rundown of what I would look at to gauge how strong, or relatively week the US economy is. Next I would look at things such as the NFCI (National Financials Conditions Index) to give me an insight into how tight/loose financial conditions are within the economy which would allow me to answer a very important question when trying to depict the regime.

What is the Fed doing? Net easing or net tightening?

That one question clears a lot of confusion, if you can tell what the Fed is doing, whether easing (QE) or tightening (QT) then you’re halfway to figuring out the regime.

E.g, over the past 12 months the Fed has been tightening, so we now know the current policy isn’t accommodative to conditions.

Next, we would want to figure out one thing, is growth accelerating, or is growth decelerating?

That now allows us to group the market into 4 different dynamics:

Growth is accelerating and we have an accommodative central bank (Fed for e.g)

Growth is decelerating and we have an accommodative central bank

Growth is accelerating and we have a restrictive central bank

Growth is decelerating and we have a restrictive central bank.

Voila!

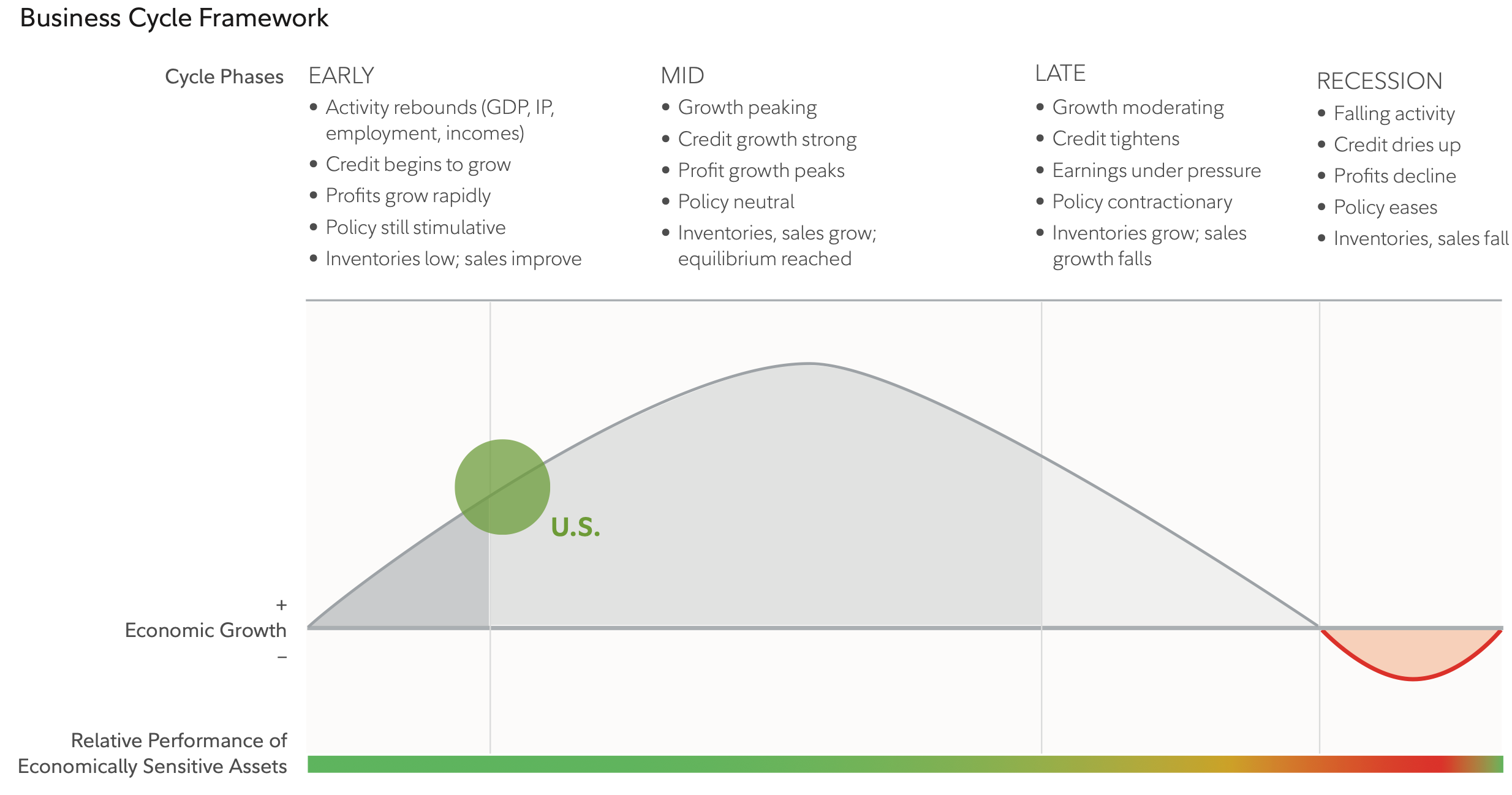

This visual should help you understand the peaks and troughs in market cycles which play along to create different regimes in financial markets. This represents the U.S economy during the early recovery from Covid in 2021.

Great, so now you know that we can only be in 1 of these 4 market regimes or dynamics, the next question you would want to start asking yourself is, what regime are we headed to next? And what asset class has produced outsized returns in such environment?

As we stand I’m confident that most if not all of you can depict which one of the four regimes we’re currently in, and if that’s not you, then I highly recommend going through the private reports that you have access to dating back to April 2023, there’s a lot of key lessons covered.

Regime 4, that’s where we currently sit, now in such an environment the usual go to would be a rush to safety i.e cash, or bonds but we’re not seeing that yet, and the reason for that is simple.Although we may be in a particular market regime, where historically you would take up a defensive portfolio allocation, that does not always mean that’s gospel. Timing. The one component that us macro analysts fail to comprehend and adhere to; in the case of deciphering what asset would present the best case return you would assume that following the ‘trend’ of going long defensives, dollar cash, gov bonds, would be the best decision, right?

Not exactly, you see within a macro regime timing is another factor to consider, just like in FX, if you get the directional move correct but you’re too early or too late to capitalise from the trade, you’re still wrong, no matter how good the analysis is. The same applies to macro.

That’s why it’s important to then go to another level and use theories such as “Dollar smile” or market correlations or study the cyclicality of markets to help guide you to deciding what trade presents the best immediate return.

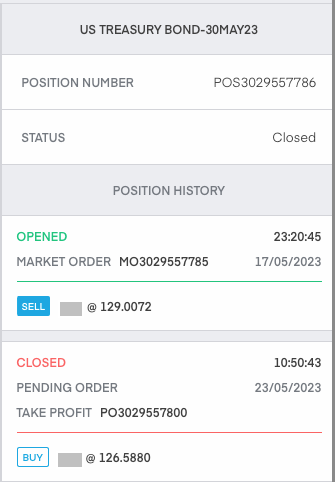

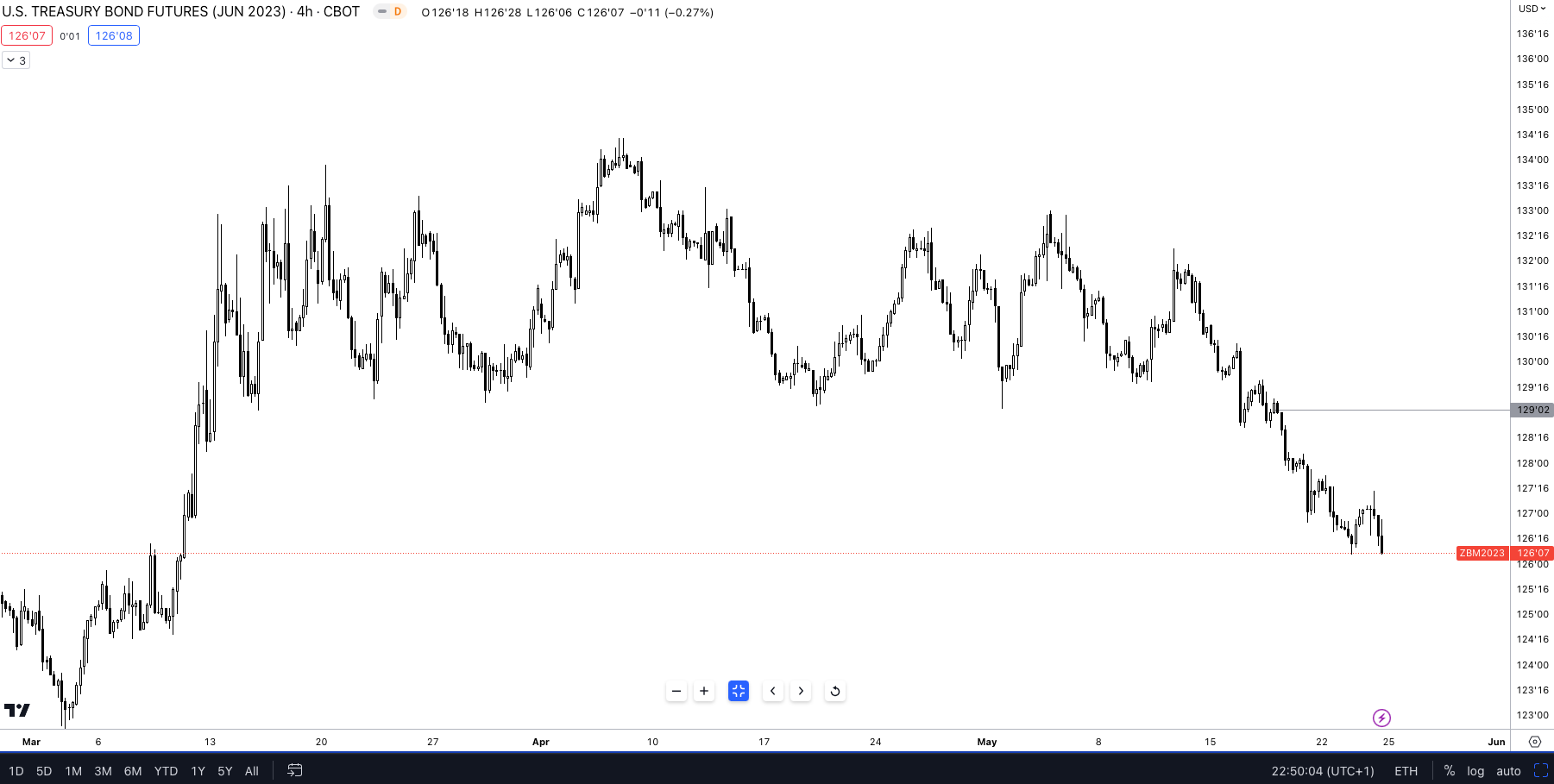

My short position on US Treasury Bond -30May23 (futures contract) achieved its target, a small PnL victory, but a victory nevertheless.

As you can see below, futures price for Treasury’s have been declining ever since reaching highs during the wake of the SVB crisis. However, as the talk around a potential debt ceiling crisis began to gain momentum Treasuries, mainly across the front-end (1M - 6M) maturity, yields significantly rose as investors demanded higher yields for the additional risk being taken in the even of the U.S defaulting and having outstanding bonds to pay creditors.

As this began happening, I saw an opportunity to explore, and test an idea; a short term macro play which went in my favour. That’s what we’re here to do, not just read about things in the news but actually turn them into actionable trade ideas; I’m no pro global macro trader yet, but, I can promise you one thing, this is exactly how they all started.

Reading, researching, executing. Loosing most, winning some but gaining an understanding with each trade, with each position, building their own edge in the market through their macro interpretation.

Oil Short Review

My oil short is still active, currently sitting in drawdown as we speak, this was my high conviction trade but as we know the market’s job isn’t to care how high or low your conviction is, it’s purely to be the judge and exchequer.

On Tuesday the Bloomberg hosted the Qatar Economic Forum, where business and world leaders gathered in Doha to discuss business trends and global growth opportuinities. During the conference Saudi energy minister, Prince Abdulaziz Bin Salman warned that speculators shorting oil should “watch out” and that they would be “ouching” just like they were in April. The comments raised bets that OPEC would cut production, causing a supply squeeze which would translate into higher WTI prices.

In such case I am forced to re-evaluate my thesis and how I have positioned myself in the markets. Like I’ve said in a previous report, as a macro analyst it’s important to have:

OPEC+ members are set to meet June 4th to discuss the next move, by which I may have either doubled down on my bets or liquidated the position.

Additionally, Memorial Day is this coming Monday. If you didn't know, this day is associated with higher oil prices since it marks the peak in U.S summer travel. As is such, there’s more conflicting data with my short view. It’s more important to find reasons against your position than to look for reasons for your position.

From this, I aim to present an example of how you should aim to start testing out your knowledge of the macro world once you form a fundamental understanding of what we discussed in the first half of this report.

For now that’s it but we’ll be going heavy from next week uncovering recent market trends.