The Red Sea Trade: Gold, Crude, TLT

Red Sea on Fire, Oil on Ice: Why Volatility is Ignoring Geopolitical Heat

Hey crew,

This is the first public report of 2024! We’re 12 days into the New Year so it’s never too late to wish you all a happy new year.

Clarity.

A simple word, yet a difficult mental mode to enter for most.

I believe the level of clarity one achieves is dependent on the level of questions you ask yourself. So if you feel you’re lacking that clear-eye view, map out a blueprint of where you’re trying to get to and start asking better questions.

The new year brings with it new narratives, themes and trends which I’ll aim to uncover throughout this year.

As for now, this year is lining up to be another year heavily influenced and directed by both macro and geopolitical headwinds.

Red Sea Conflict Triggers Safe Haven Flow

My previous reports emphasized the paramount influence of geopolitics on asset market performance in 2024. From international conflicts to pivotal elections in key regions, we must now meticulously map potential scenarios and their repercussions for capital markets.

In my report on lessons from hedge funds, I stated this:

In a recent interview, Ken Griffin shared how Citadel approaches the art of risk management and this was what he had to say:

“We look at a variety of historical scenarios and how that impacts our portfolio. When there are events that are being talked about by geopolitical analysts, we will start to run stress tests”

Ken Griffin, Citadel founder

Ken continually asks the question, “How would our portfolio perform if X unfolds?” and I believe there’s a distinct lesson in this mental framework. That lesson, simple yet overlooked, is preparation. Always alert to potential risks and scenarios that would put his portfolio’s return profile at risk. Such scenarios he would test for would be:

Recessionary environment

The second tailwind of inflation

Higher long-run Fed funds rate

Geopolitical escalation between China-US

Middle East involvement in Hamas-Israel

Liquidity risks

Black swan events; e.g Covid-19

This is more relevant than ever given the escalations in the Red Sea.

The Trade Catalyst

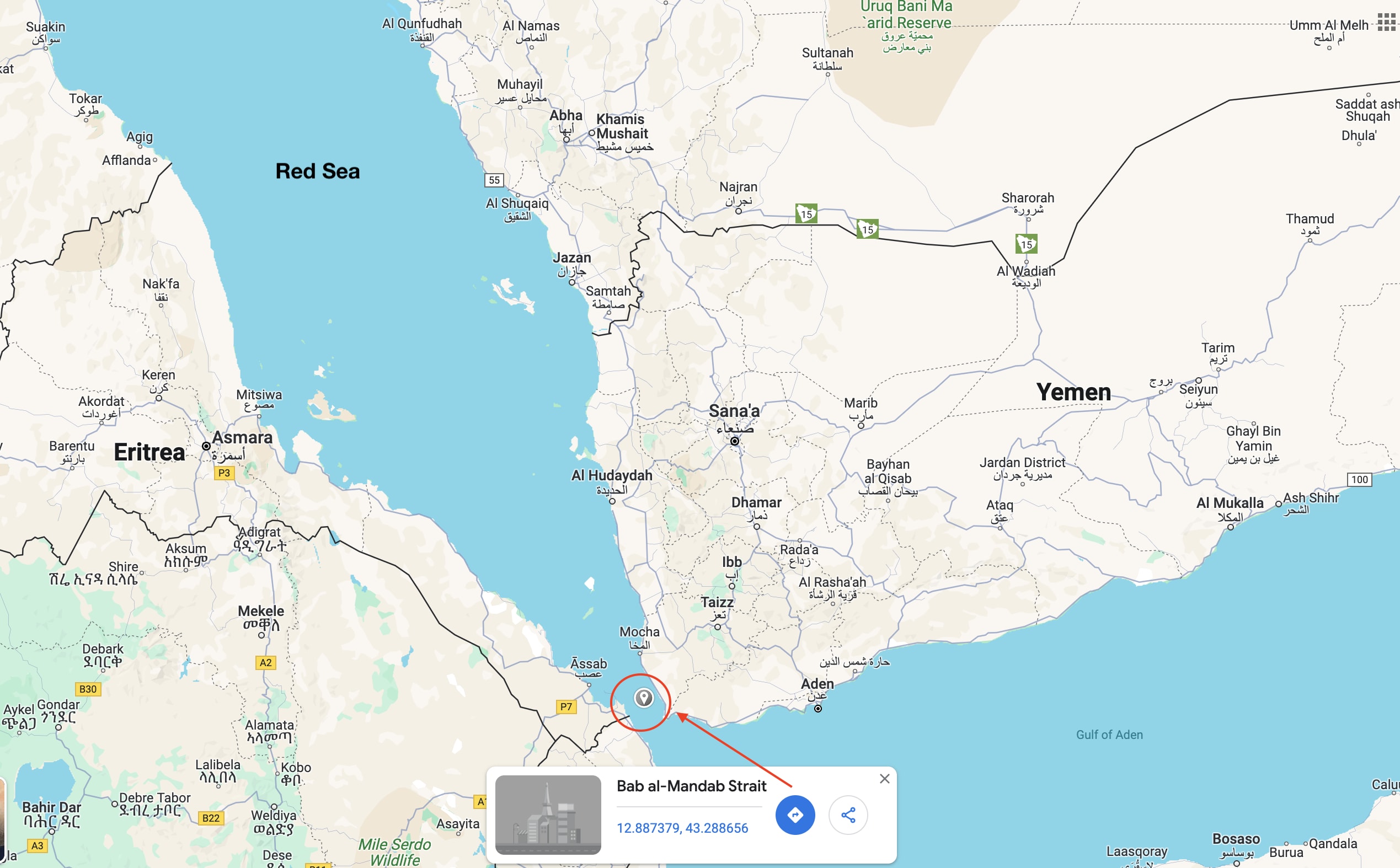

In the early hours of the morning, the US and UK launched airstrikes targeting the Houthi’s in Yemen. The countries launched more than 60 airstrikes on Houthi targets in an attempt to neutralise the threat the Shia Islamist militant group posed to the global shipping industry. In response to the Israel-Hamas conflict, the Houthi rebels began attacking ships in the Red Sea which plays a fundamentally crucial role in global trade due to its strategic location acting as a bridge by connecting Africa and Asia to Europe facilitating trade relations and capital flows.

The crown jewel of the Red Sea is the Suez Canal, this waterway provides a direct shortcut between the Mediterranean and the Red Sea reducing travel distances for ships sailing between Europe and Asia. By shaving travel distances between Europe and Asia, it facilitates 12% of global trade, including 10% of seaborne oil and 8% of LNG, solidifying its position as a cornerstone of the global economy.

The Houthis attack on vessels has imminent effects on global trade, shipping companies have been instructed to avoid the Bab el-Mandeb.

Prior to the airstrikes, Bloomberg reported a 15-20% decline in oil and gas tanker movements. The ensuing conflict forced shipping firms to detour around Africa, disrupting trade flows and triggering cascading effects (first, second, and even third-order) across the market. Investors, seeking refuge from escalating tensions, flocked to gold and the safety of US Treasuries (TLTs).

The consequence of the US-UK attack on the Houthis means prolonged and escalated measures of violence, which for oil tankers, translates to further trade route disruptions, higher transportation fees as they travel around Africa and delayed energy delivery on a mass scale to parties in Europe. Oil rallied 3% in a matter of hours following the attacks before retreating in the middle of the London session.

Contrary to most beliefs, the OVXCLS (Crude Oil Volatility Index), remains fairly subdued, currently below its long-term average of 39.00, not showing a heightened reaction to the risks at hand across.

My thoughts as to why the oil volatility index seems muted point back to the current supply-demand dynamics oil is experiencing. The Middle Eastern oil powerhouse Saudi Arabia cut the price of its crude oil for February delivery for all buyers due to perceived persistent weakness. Lead oil exporter Saudi Aramco, reduced its flagship Arab Light price to Asia by $2 to $1.50 a barrel, that’s a 57% cut in price per barrel. For Saudi Arabia, Asia remains the top destination for crude oil exports, in 2022, Mainland China, accounted for 21.7% of the total Saudi crude exports, followed by Japan with 16.2%, South Korea with 13.1%, ASEAN with 11.8%, India with 11%, and Taiwan with 4%. Price cuts usually incentivise refineries around the world, particularly oil-heavy-consuming refineries in China & Japan to increase their demand, but the price cut has had little success in increasing oil demand.

Mixed data from Mainland China further confirmed the lack of enthusiasm to purchase discounted Saudi crude. China recorded their second consecutive month-over-month of decline in inflation, which although still deflationary beat the consensus of -0.4% recording a -0.3% decline in prices over December. However, all is not negative, China is expected to lead global oil demand growth in 2024 to fuel an economic revival. Forecasts predict China’s oil demand will rise by around 530,000 barrels a day in 2024; much of that demand growth is expected in H2 so oil prices may begin to experience an uplift as the global rate environment cools creating an ideal macro landscape for strong oil demand.

As such the following instruments remain sensitive to any escalations of conflict in the Red Sea and present upside opportunities in continued attacks:

Gold

WTI Crude/ Brent Crude

TLTs are experiencing a wider range of influences on both yields and price which is why I would focus primarily on the two commodities above.

In what has been an intense start to the trading year, I hope this report has been able to provide some clarity to you.