The Oil Shock, Rates, and the Recession Call (Part 2)

The DAX is the cleanest expression of the asymmetry

In Part 1, I made the case that this is not a recession setup. The yield curve is bear steepening, GDPNow is at 3.52%, core inflation is not showing oil pass-through (yet), and the 10y nominal decomposition is being driven by LOWER real rates.

I also made the case that oil is the pivot. The bearish macro narrative is entirely downstream of the oil rally. And oil itself is sitting at an extended z-score, with a price / implied vol divergence that historically does not last, in a complex that has rotated from macro to dispersion. The base rates point toward normalisation.

That sets up the question for Part 2. If the macro setup is bullish and oil is the variable doing all the bearish work, what is the cleanest way to express the asymmetry?

Long DAX in my view.

Let me walk you through WHY.

DAX is in the most negative oil-sensitivity regime in nearly a decade

Roll a sensitivity analysis of DAX returns vs WTI over the last decade. The latest beta is highly NEGATIVE. This is one of the most negative readings in the entire sample.

Plain English: DAX is right now MORE sensitive to oil moves than it has been at almost any point in the last decade. That cuts both ways. It explains why DAX got hit hard on the rally to $100+. It also means that if oil normalises, DAX has the most coiled spring in the cross-section.

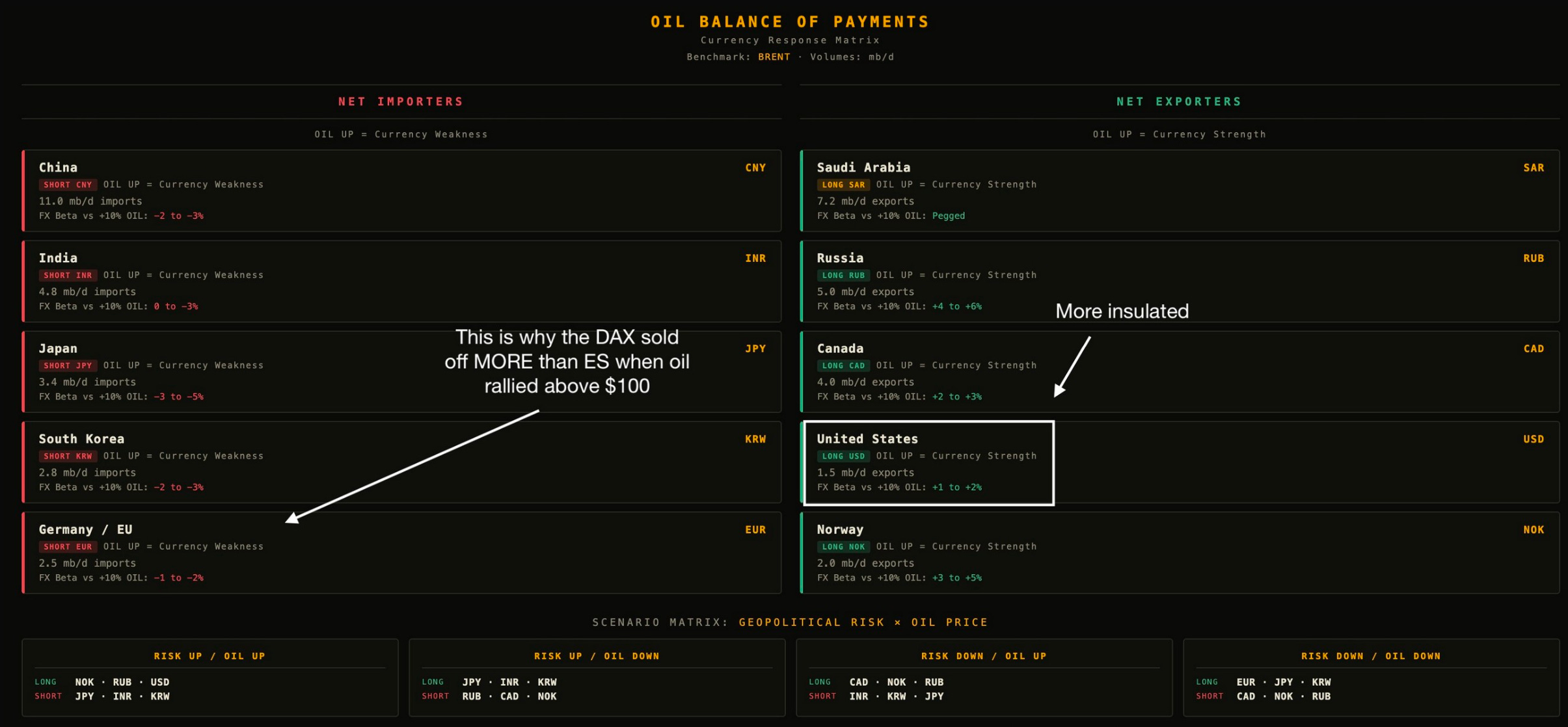

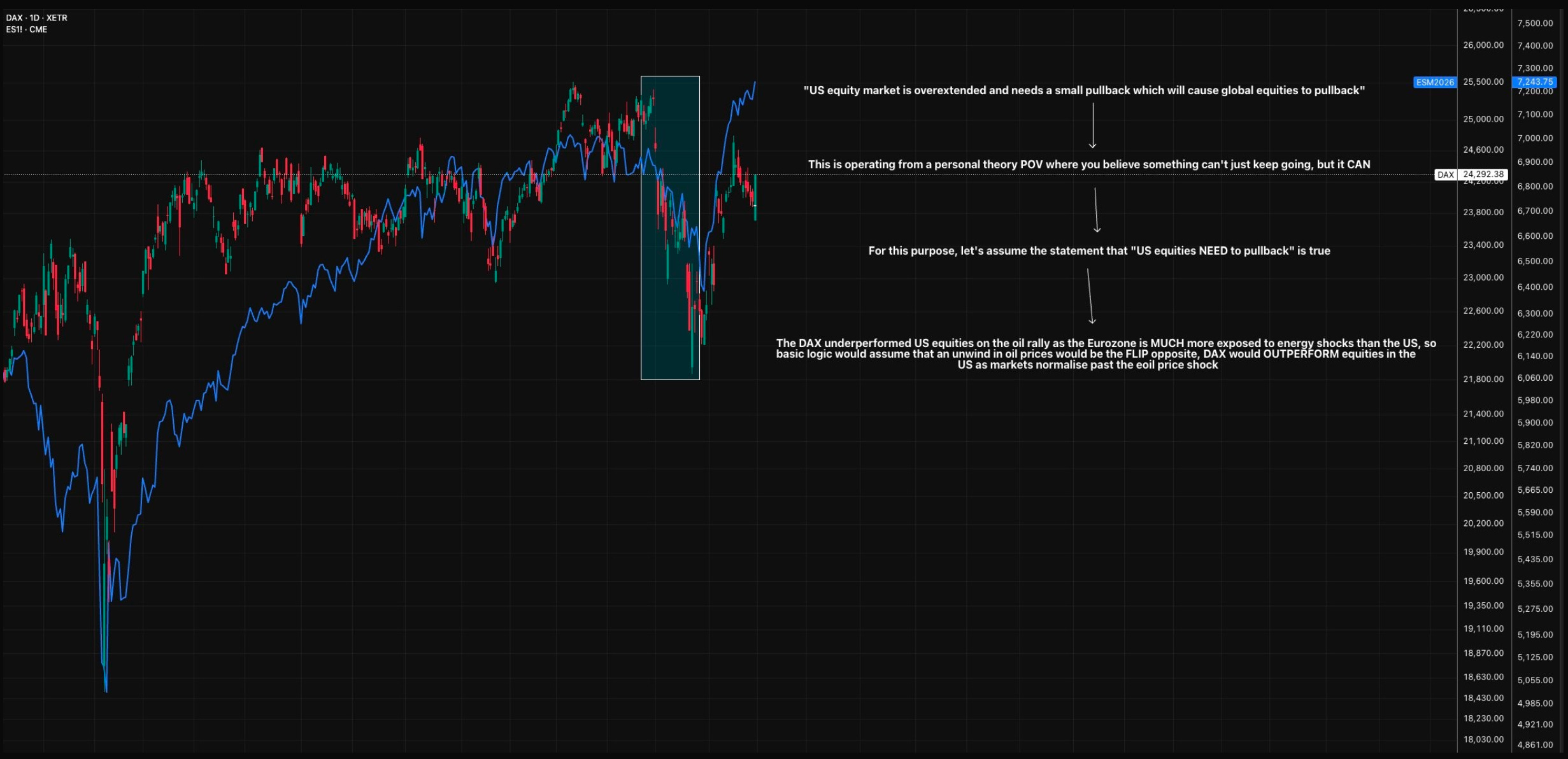

The FX channel: why DAX got hit harder than ES

The DAX underperformance vs ES on the oil rally was because the Eurozone is structurally a bigger net oil importer than the US, and the FX channel makes the impact larger.

Net importers like CNY, INR, JPY, KRW, EUR get hit on oil up. Net exporters like SAR, RUB, CAD, USD, NOK benefit. The US sits on the exporter side now, with 1.5 mb/d of net exports; Germany / EU sits on the importer side with 2.5 mb/d of net imports. That is a structural difference and it shows up in the relative move.

If you accept the view that ‘US equities need a pullback’, the flip side of that view is that DAX outperforms on the unwind. You do NOT need the US to sell off at all, you just need the energy / rates pressure to come out, and the DAX captures MORE of that benefit than ES does.

The asymmetry sits in DAX favour as the market normalises past the oil shock.

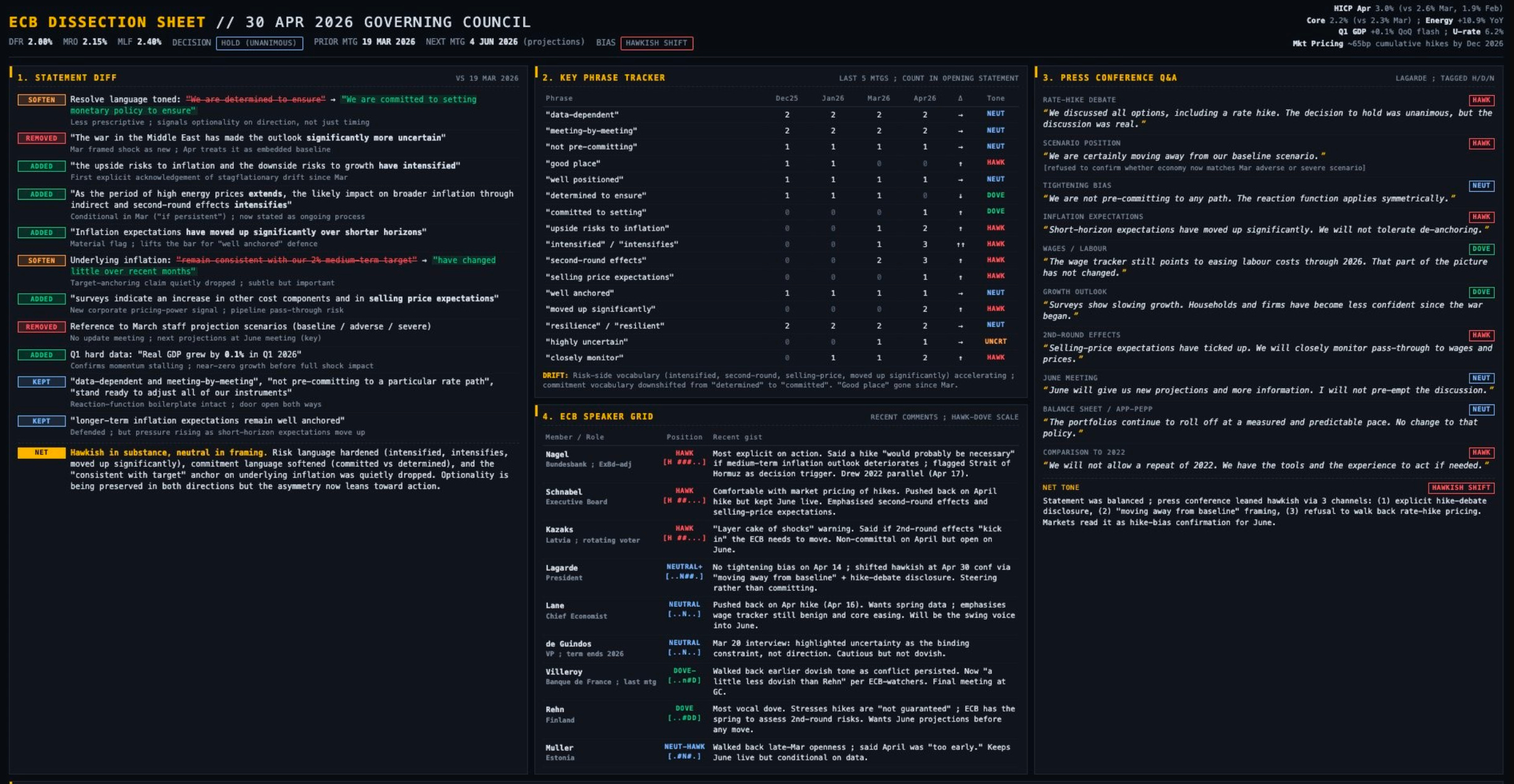

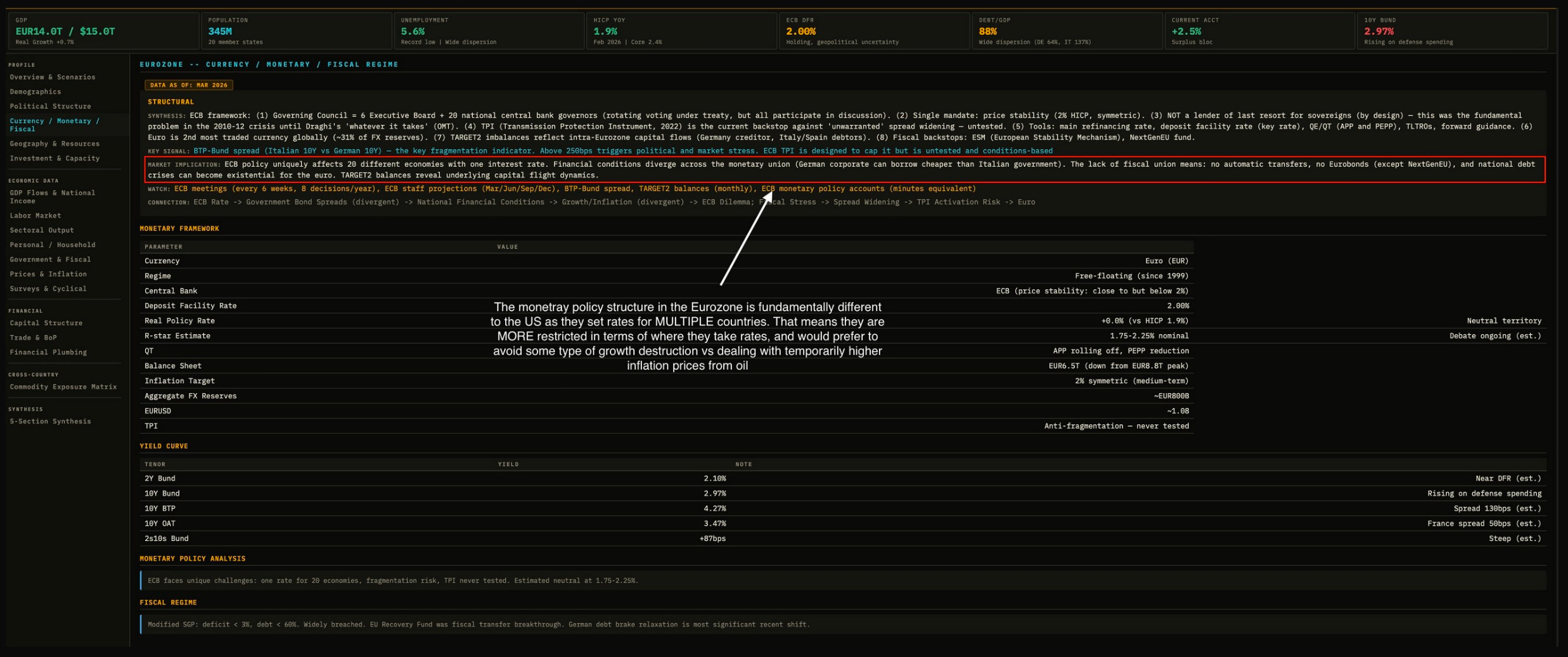

The ECB is the linkage

Last wee’s ECB meeting was a hawkish hold. Lagarde explicitly disclosed that a rate hike was discussed. Statement language got harder: ‘intensified’, ‘second-round effects’, ‘selling price expectations’ all moved up; ‘determined’ got softened to ‘committed’. The market read it as hike bias confirmation for June (once again, meaning it’s PRICED).

But here is the thing. The ECB forward curve is STILL pricing 3 hikes across 2026. That pricing is the artefact of the oil rally and the hawkish framing.

If oil normalises, that pricing HAS to come out (in my view, because nothing actually HAS to happen). The ECB does NOT want to be hiking into a supply-led inflation shock (transitory) with cracks already showing in growth. They are structurally more constrained than the Fed because they set one rate for 20 economies and the asymmetry of policy errors there is not easy: hike too hard and you risk fragmentation, BTP-Bund blowout, the whole 2010-2012 nightmare. They will absorb temporary inflation rather than destroy growth where they can.

The forward curve is the release valve. Lower oil unwinds the priced hikes. Unwinding the priced hikes lifts the DAX. Both legs are market-implied so it makes complete sense. The DAX rally is market-implied, the forward curve is market-implied. There is NO narrative judgement here, no PM saying ‘I think the ECB will not hike that much’. The market is telling you (through the price) that it expects growth to hold even with the current oil and rate prints.

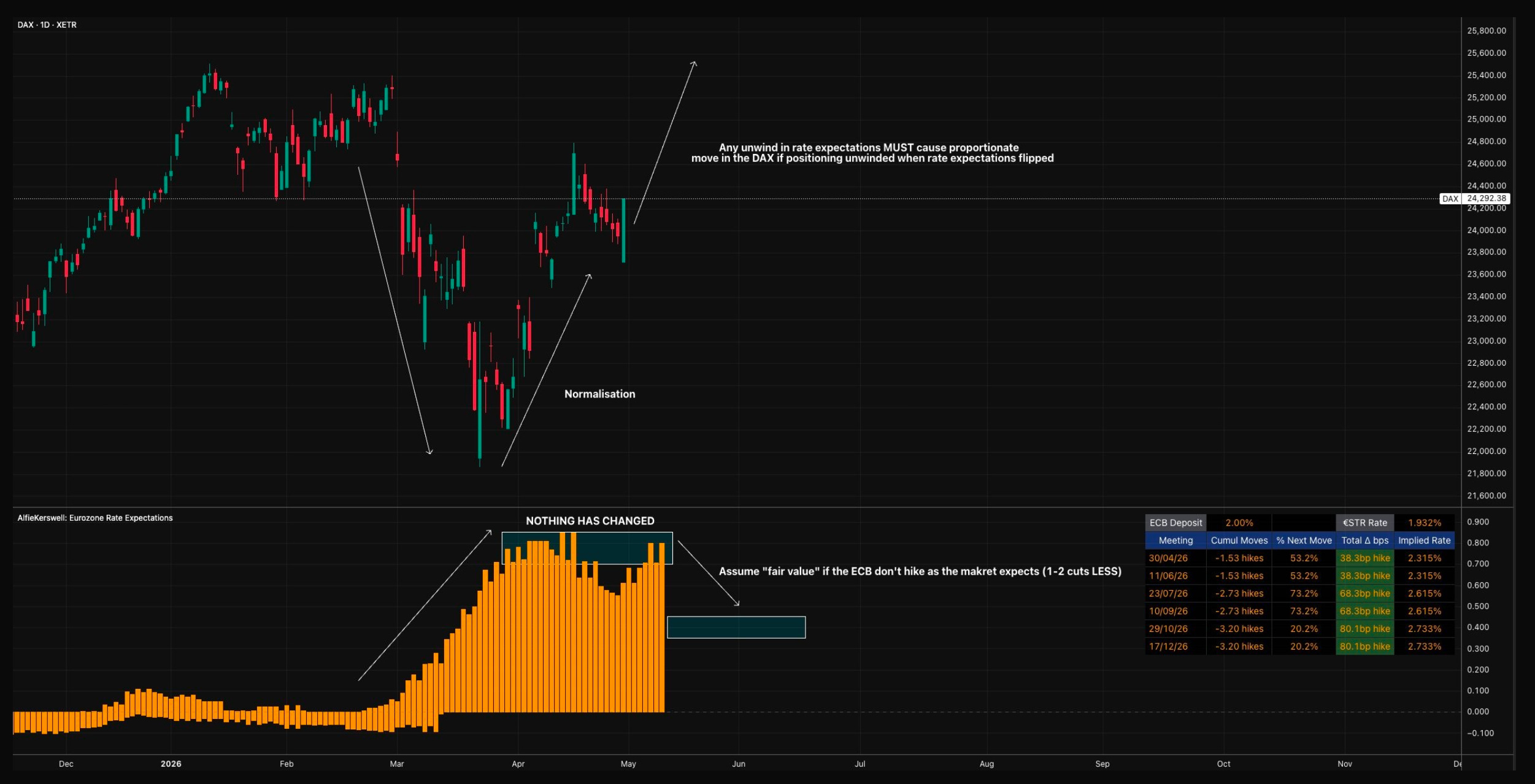

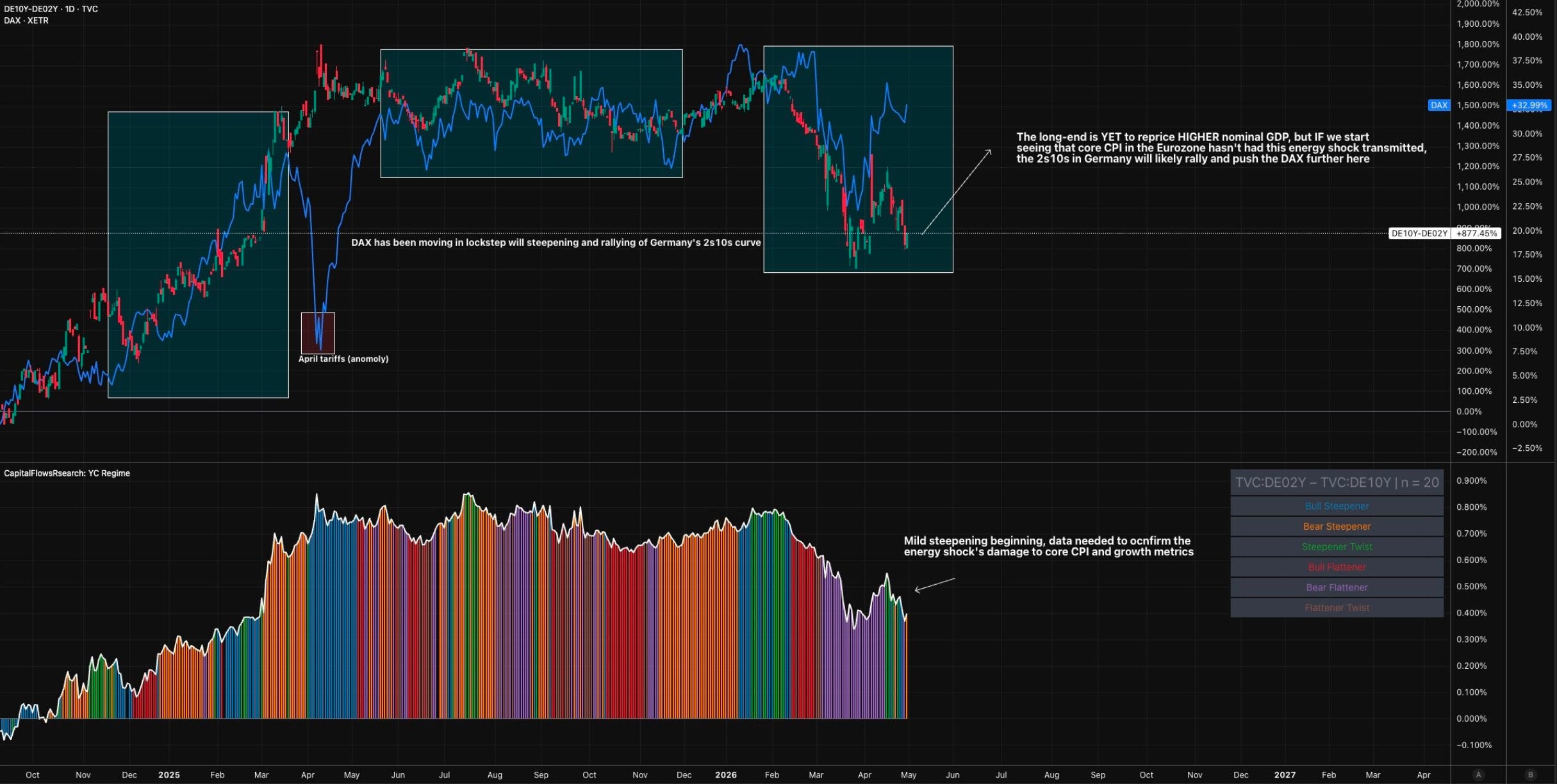

DAX moves in lockstep with the German 2s10s

The DAX vs DE 2s10s relationship is one of the CLEANEST. April tariffs aside as an anomaly, the lockstep is clear. DAX has rallied as the German curve has steepened.

The long end has yet to fully reprice higher nominal GDP. If core CPI prints contained over the next prints, the long end reprices, 2s10s steepens further, and the DAX follows.

The unfinished business in the trade is the long-end repricing. Mild steepening is already underway; data confirmation is what completes it.

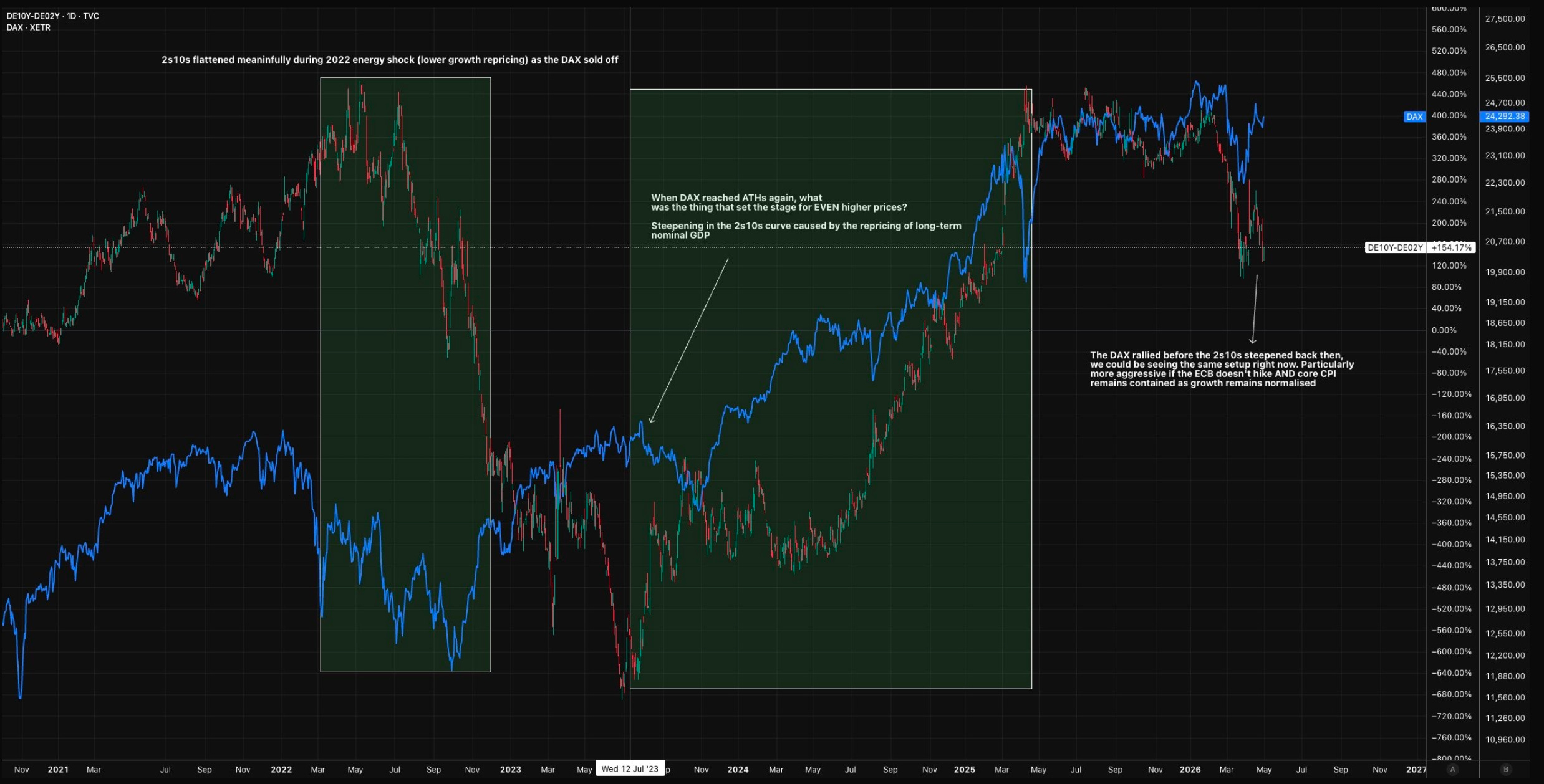

The 2022 analogue

Pull up DAX vs DE 2s10s through 2022 to 2024. Energy shock hits. 2s10s flattens meaningfully, repricing lower growth expectations. DAX sells off. Then the relationship inverts: 2s10s starts steepening on the repricing of long-term nominal GDP, and the DAX rallies all the way back to ATHs.

The current setup mirrors this. We have had the shock, the flatten, and now starting to see the steepening. If the ECB doesn’t deliver the priced hikes and core CPI stays contained, the analogue plays out AGGRESSIVELY. Particularly if both conditions are met.

Energy shock compresses growth expectations, growth expectations stabilise as the shock fades, long-end reprices, the asset class most exposed to the original shock outperforms on the unwind. DAX is the asset class to express that.

What could make me wrong

The honest version of ANY thesis includes the conditions for being wrong. Here are the ones that matter:

Core CPI transmission. If core CPI / Core PCE start showing meaningful pass-through from the oil rally, the inflation resurgence story has legs and the ECB is not bluffing. Watch the next two prints carefully. The whole thesis hinges on the energy shock NOT transmitting to stickier prices.

A genuine supply break. The base-rate argument on oil normalisation assumes the current rally is shock-driven. If we get a structural supply event, OPEC+ break, Strait of Hormuz, hard sanctions enforcement, then oil prices don’t mean-revert in the usual way.

Eurozone fragmentation. BTP-Bund spread is the fragmentation tell. If it widens meaningfully, the ECB hike pricing becomes self-defeating and the DAX does not get the release valve benefit because risk premia rebuild faster than rate expectations come out.

Hard data deterioration. I’m leaning hard on the US growth diffusion and GDPNow read. If the next NFP, claims, and retail sales prints break meaningfully softer in unison, the recession crowd gets a real data point (even though we’d stilll be far from a recession).

The setup right now is high conviction but not unconditional. The conditions are listed, watch them.

Putting it together

The thesis across both pieces is straightforward.

It is not a recession. The curve, the data, and the inflation read all point to expansion repricing higher nominal GDP. Recession views are wrong, mistimed (or both as I said previously).

Oil is the pivot. It is doing all the work on the bearish narrative, and it is sitting at extended levels with a price / implied vol divergence in a complex that has rotated to dispersion. The base rates point toward normalisation.

The DAX is the asymmetry. Beta to oil at the 1st percentile. ECB OIS still pricing 80bps of hikes that have to come out if oil normalises. The DE 2s10s lockstep with DAX is unfinished, with the long-end repricing yet to complete. The 2022 to 2024 analogue ran exactly this script and ended at all-time highs.

The trade is positioned for a release of pressure. If oil normalises and core CPI stays contained, the path of least resistance is rates expectations come out, the long end finishes repricing higher nominal GDP, and the DAX captures the massive follow-through.

Thanks

Alfie

Great stuff! Do you have a view on how eurobonds would perform if oil gets repriced down significantly?

Thank you Alfie