The Jobs Keep Coming

Snapshot review of the US jobs report

Hey crew,

I’ll say it again, glad to be back.

There’s 3 weeks until 2024.

A year in which I experienced a lot, learned so much outside of markets.

A year in which I made the most out of every high, and picked myself up out of every low.

Patience, resilience & discipline. These principles that have become personal auditors of all my actions, ever-growing, ever-learning and forever welcoming of the new chapter.

No resolutions, just sharpening of the tools, anyways, here’s a snapshot review of the US labor market.

Strength Persists in the Labour Market

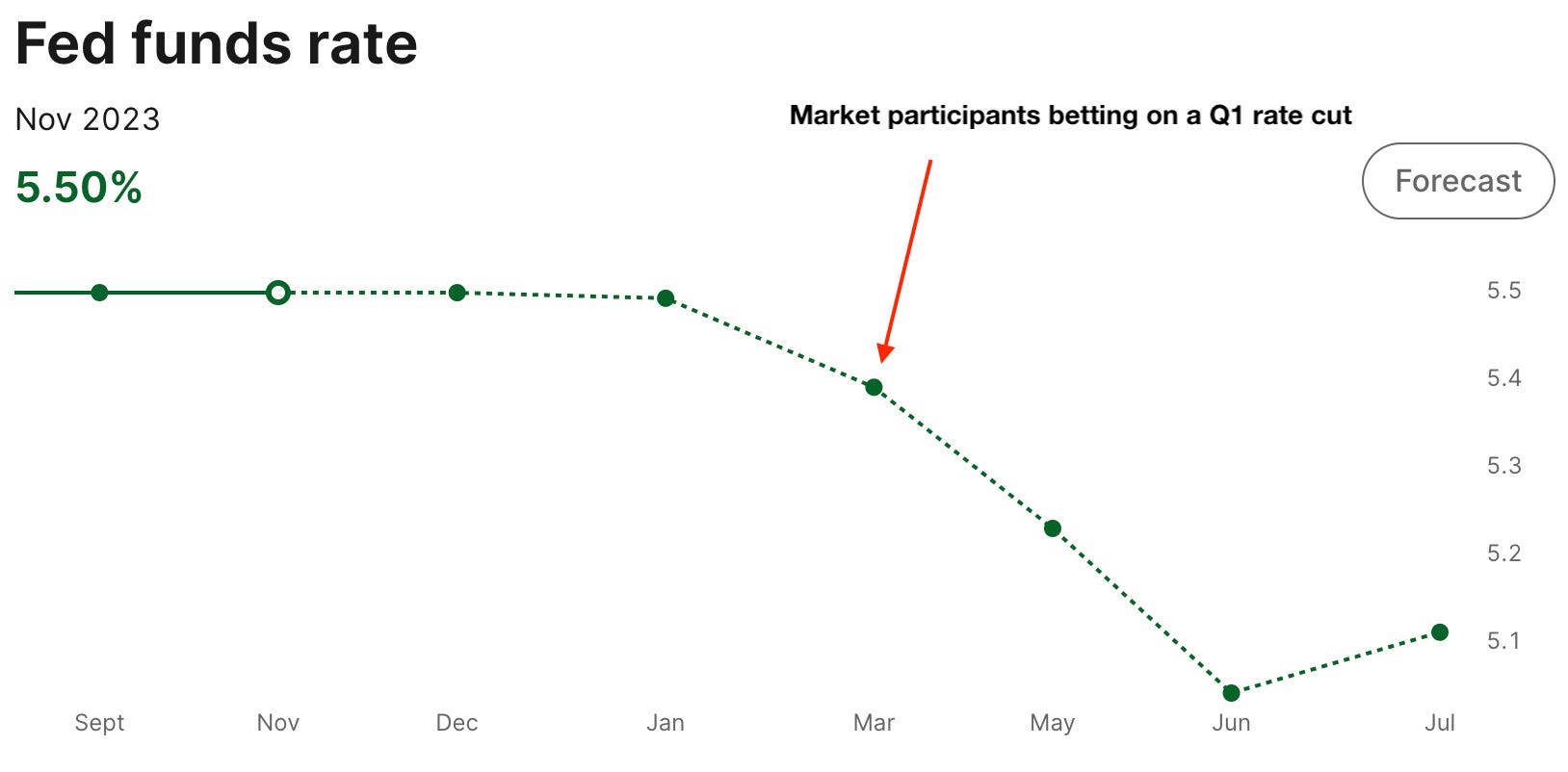

As the Fed transitions from tightening monetary policy to softening policy projected in H2 of 2024 markets are left in a very peculiar position with both investors and policymakers tentative of all data releases coming out regarding inflation, growth and unemployment. For investors allocating into PE, VC, or any capital-intensive investments with high sensitivity to policy rates, any confirmation that the Fed is releasing its foot from the gas for certain will result in a huge amount of capital flowing to these investment vehicles.

Bill Ackman, hedge fund manager of Pershing Square Capital, believes rate cuts will commence in Q1 of 2024, a standout viewpoint compared to the broad consensus that we will see a Fed cut in either Q3/Q4. If we were to see early rate cuts from the Fed, the Biden administration would benefit hugely during the Presidential election near year. Now that inflation in the US is largely in the rearview mirror, cutting interest rates not only helps the return profile of financial markets but also businesses with financing demand and the average US citizen looking to become a homeowner. Reasons that would fuel sentiment to back the current Biden administration.

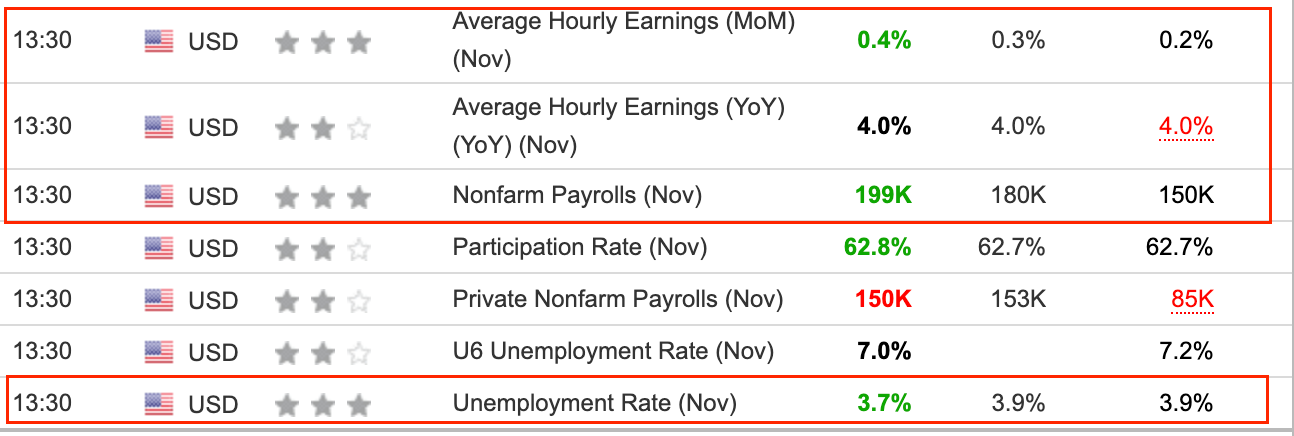

Non-farm data was released today and this print may force traders betting on a Q1 pivot to re-evaluate their views. Expectations were that the US added 184k jobs over November and average hourly earnings grew 4.0% YoY. The US labor market exceeded forecasts adding 199k jobs in November whilst the average overly earnings stagnated at 4.0%.

The labor market continued to power forward regardless of the Fed’s hawkish rhetoric on keeping policy unchanged. I believe this was a strong, but relatively tame job print.On Tuesday, the Bureau of Labor Statistics released the JOLTS job openings data, which fell short of expectations. Job openings were anticipated to reach 9.31 million but settled at 8.73 million in October, missing the mark by nearly 600,000.

The downside to this data point is its time delay, JOLTS are released with a two-month lag, which limits its impact on financial markets. However, this hard-lagging data point carries with it an element of confirmation regarding the health of the US labour market. Adding to woes, Wednesday’s ADP employment change (private sector jobs) also disappointed to the downside adding 103k vs 131k expectations.

The market's response to the NFP print appears to have been more of a knee-jerk reaction, as the underlying trend in the labor market remains robust. While the pace of job growth may have moderated, there is no immediate sign of weakness that would jeopardize the prospects for economic growth in the US.

In the immediate aftermath, yields on the 2Y spiked 10bps to 4.740% whilst the 10Y’s reaction was slightly muted in comparison to the 2y, seeing a moderate 10bps rally. The question we need to be asking is what condition the US consumer is in? Throughout 2023, the US consumer rallied through the consequent effects of inflation continuing to spend both in store and online, but that still doesn’t tell us the underlying health of the US consumer. Wage

Headlne inflation has slowed to 3.2% YoY, but that’s still an increase in prices. The cost of goods are still rising in price, now its just at a reduced pace. This drag on financial household spending is what I believe will mount into a looming problem for US consumption as consumer credit card debt defaults begin to rise. I’ve got a report dedicated to the credit crisis.

In conclusion, the US labor market remains resilient despite the Fed's efforts to tighten monetary policy. The November NFP print exceeded expectations, adding 199k jobs, while average hourly earnings stagnated at 4.0%. However, the JOLTS job openings data fell short of expectations, indicating some moderation in the pace of job growth. Additionally, Wednesday's ADP employment change disappointed, adding only 103,000 jobs compared to the 131,000 expected. The US consumer remains strong, but the lingering effects of inflation and rising consumer credit card debt defaults could pose a looming problem for US consumption in the near future.

As always thanks for your readership MMH