The Equity Playbook

Strategic Positioning Through The Economic Cycle

For the last month, the market has rotated and been driven by a regime dictated by higher inflation and higher growth. Ultimately, there is higher duration risk (inflation) in the system than there is credit risk (growth), which is why equities can still perform like this even as inflation swaps tick up and inflation z-score and speed on a 3m and 6m basis remains positive (across the board - headline CPI has slowed marginally on a 3m basis). There are many different paths we could take from here but I like to think of the path of least resistance.

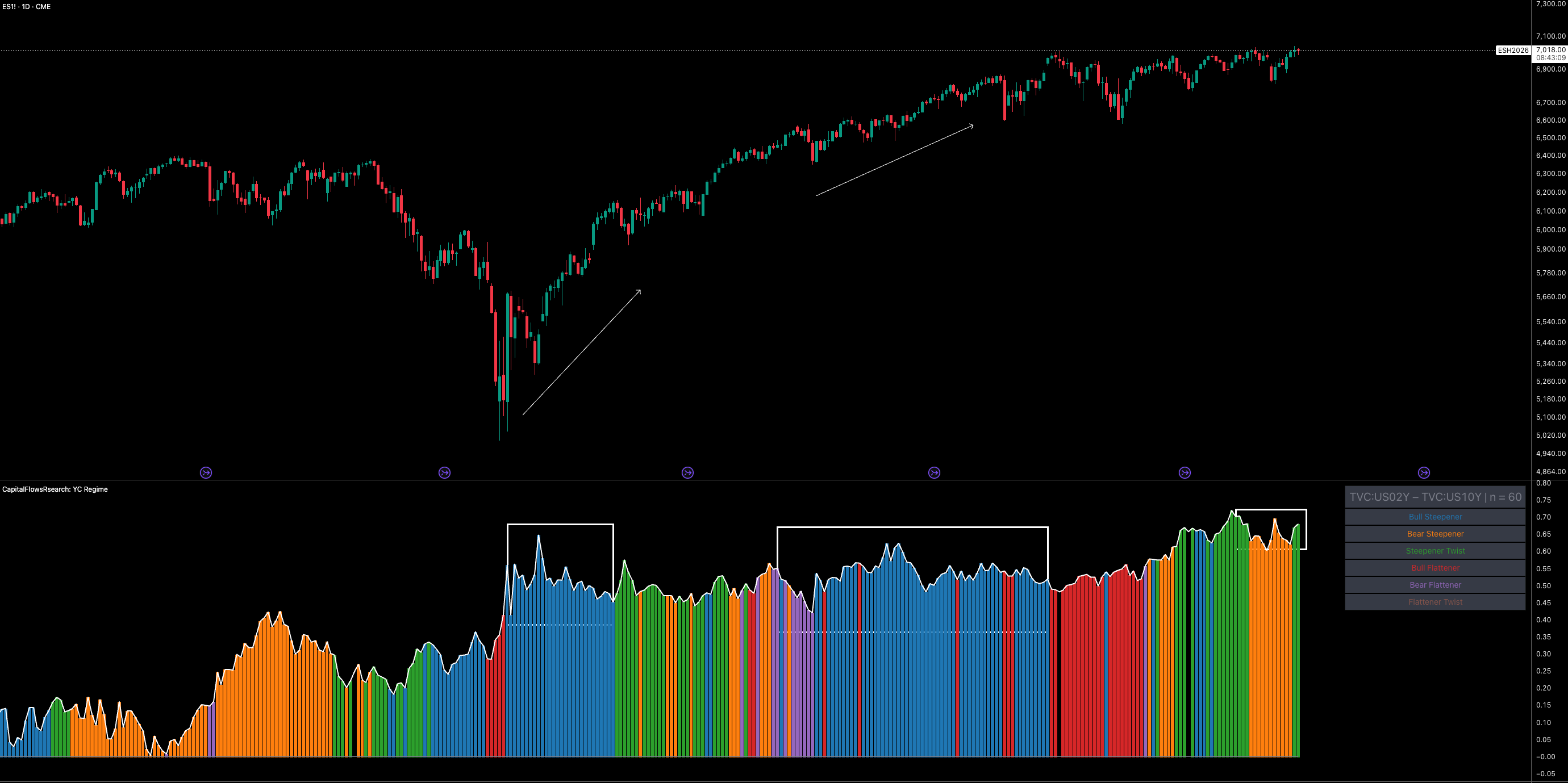

2s10s and 2s30s yield curve is bear steepening on a 60d lookback as we begin to price this reflationary regime. Bear steepenings (bonds selling off and long end rates rising faster than short end rates) had also been driven by the front end, controlled by policy of course. Now growth & inflation aren’t going to be immediate movers (e.g. if we see disinflationary pressures, it’ll show up in inflation swaps before 3m and 6m basis speed & z-score begin to signal we’re hitting a regime), so I like to watch the curve as a leading indicator to how the market is pricing the risks in the system.

You can see as we headed through the tariff saga in April, the curve actually began to bull steepen as the market priced higher growth in the long end, and rate cut expectations hit a peak (around 6 cuts at one point).

The tail-risk I see in mind for equities to continue making legs higher is if the curve flips back to a bear steepening regime because eventually, higher inflation prices will cause a larger drag on equities as growth exceptionalism slows. But we're not there yet, this is simply a tail risk to the idea. As of recent days we're moving into a steepener twist regime which is coherent to a regime where credit risk is low, and outpacing the safety of duration risk. One scenario that is feasible to keep equities pushing higher when we move out of a steepener twist regime is if we have a prolonged period of bull steepening (this is likely based on the front end).

STIRs are at an extreme, and policy pricing is stuck just below 2 cuts. I don’t think we’ll get less than 2 cuts for 2 specific reasons. Headline inflation could lead other inflationary metrics and we could see disinflationary pressure as inflation swaps tick down (less pressure on the Fed). 2) Growth is exceptionally strong but not strong enough to cause MAJOR reflationary pressures. Now that could change but based on what data we have, this is valid. Even if we deliver 50bp (not far off of STIR pricing), there would still be marginal upside pressure in bonds which would cause bull steepening, supportive of upside in equities.

One thing I noted in the substack chat was that we have seen lower reflexivity in equities and the STIR as the forward curve becomes more hawkish. Everyone loves to follow the Fed and say that when the forward curve reprices, it causes marginal downside pressure to equities but on an attribution basis this has not been the case. As rate cuts have been priced out, equities have remained strong, creating new ATHs clearly driven by growth in earnings regardless of a few labor market prints (that do not determine the whole regime itself).

There is also a case for a sharp repricing of STIR (I don’t think is likely), if the labour market has a shock in the coming months. The Fed are becoming more politically involved (especially Powell releasing a video on the topic of Trump) as fiscal policy attempts to pressure lower rates. I’ve said it 100 times, but as Trump builds out his Fed team, this will cause upside pressure in STIR only if disinflationary pressures persist and duration risk declines.

Real rates have ranged and pushed marginally down; I don't think they’re a cause for concern at these levels BUT if that shifts, I'd expect rotation out of the Russell into ES and down the curve. We’d probably begin to see marginal downside in bonds but ultimately not enough for me to get short because I think STIR pricing will drive them higher from these levels.

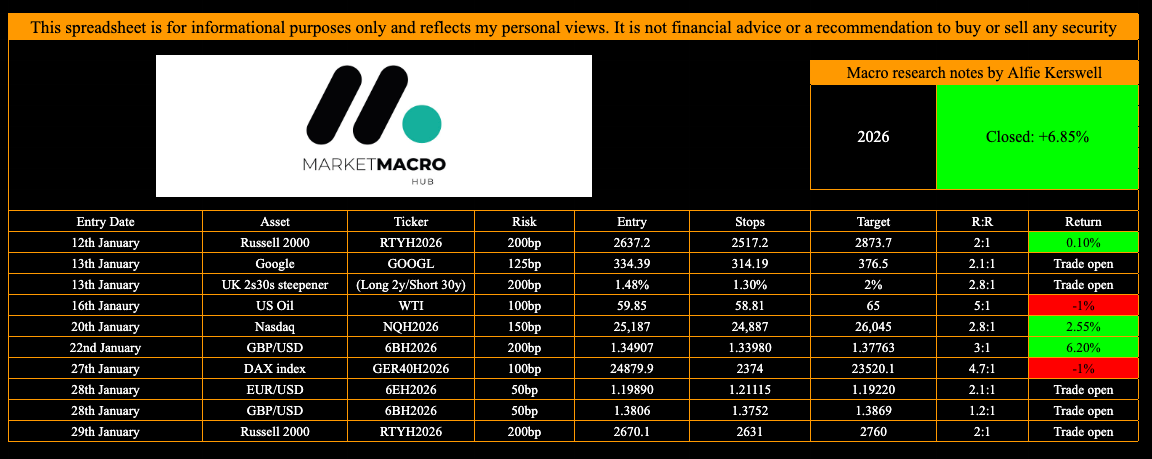

So in the coming weeks, I expect the 2s10s to continue a steepener twist with periods of bull steepening; I don't think we’ll enter back into a period of bear steepening. I think this is going to cause upside in equities. The Russell has outperformed NQ and ES across the last 20 trading days, yet has lagged on a cross-sectional momentum basis as of recent. I'm playing a catch-up in that; I'd rather be long the Russell than ES or NQ right now. I sent all my ideas in the Substack in real time and this is exactly how the trade tracker is looking:

That’s my current thoughts. Simple and to the point.

Have a good one!

good looks - smalls capssssssss.

I don't get how trump IF he successfully builds out his fed team would lead to upside pressure in STIRS