My Next Trade: Single Name Equity Analysis

Single Name Equity Analysis

Hey guys, I hope you’re all well.

I want to speak about this single name equity today and the analysis behind it. Before we get into it, I want to start with saying that 1) this is NOT financial advice, I’m simply expressing my analysis on a single name equity and 2) this name was brought about to me by a friend, so no I didnt source this niche idea, I’ve just done research behind it.

Blencowe Just Became a Different Company

Okay so... I need to talk about Blencowe Resources.

It’s becoming interesting because something happened in the last few weeks that I think most people on AIM have completely missed. And by the time they notice, the easy money will already be gone (in my view).

Let’s get into it.

The Resource Story (And Why It’s Bigger Than It Looks)

First, the geology (because it’s the foundation everything else sits on).

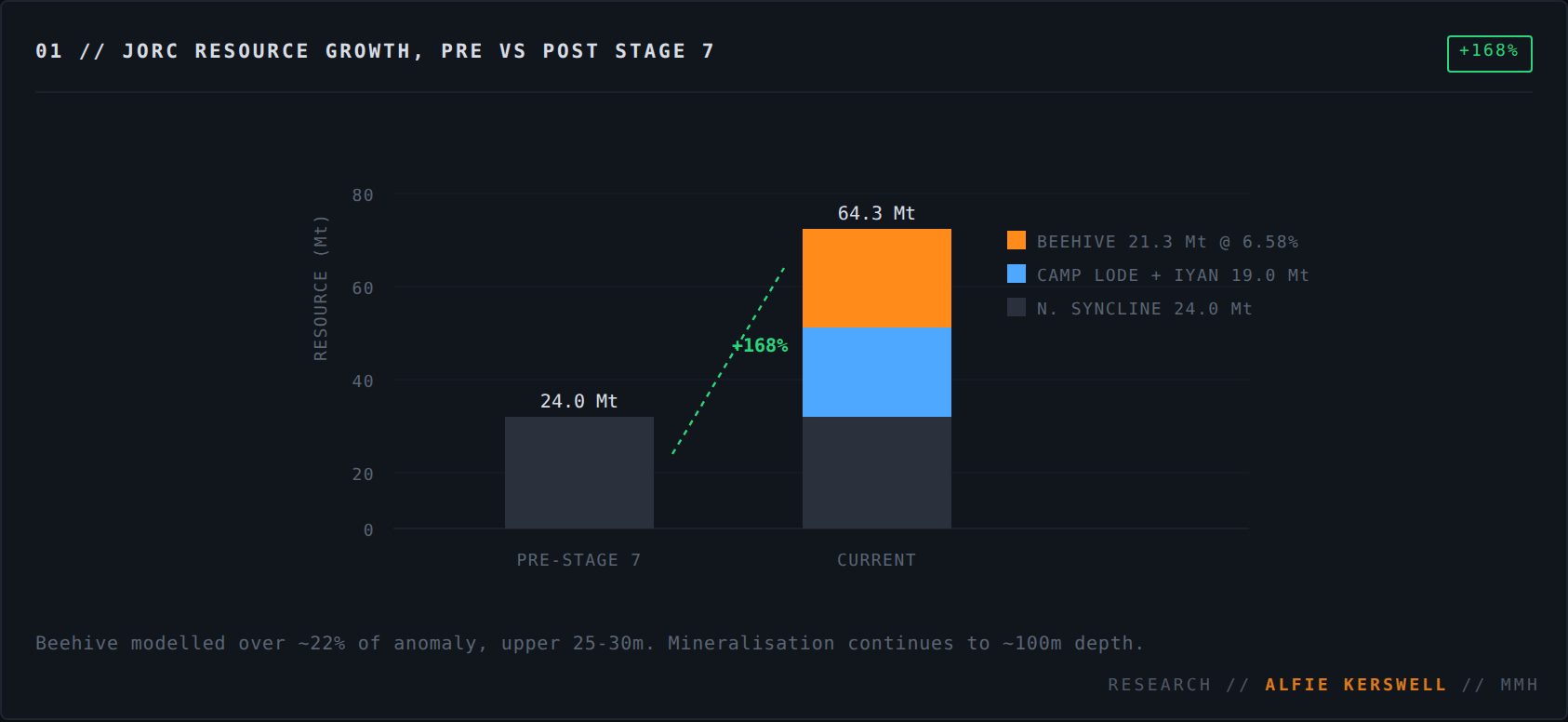

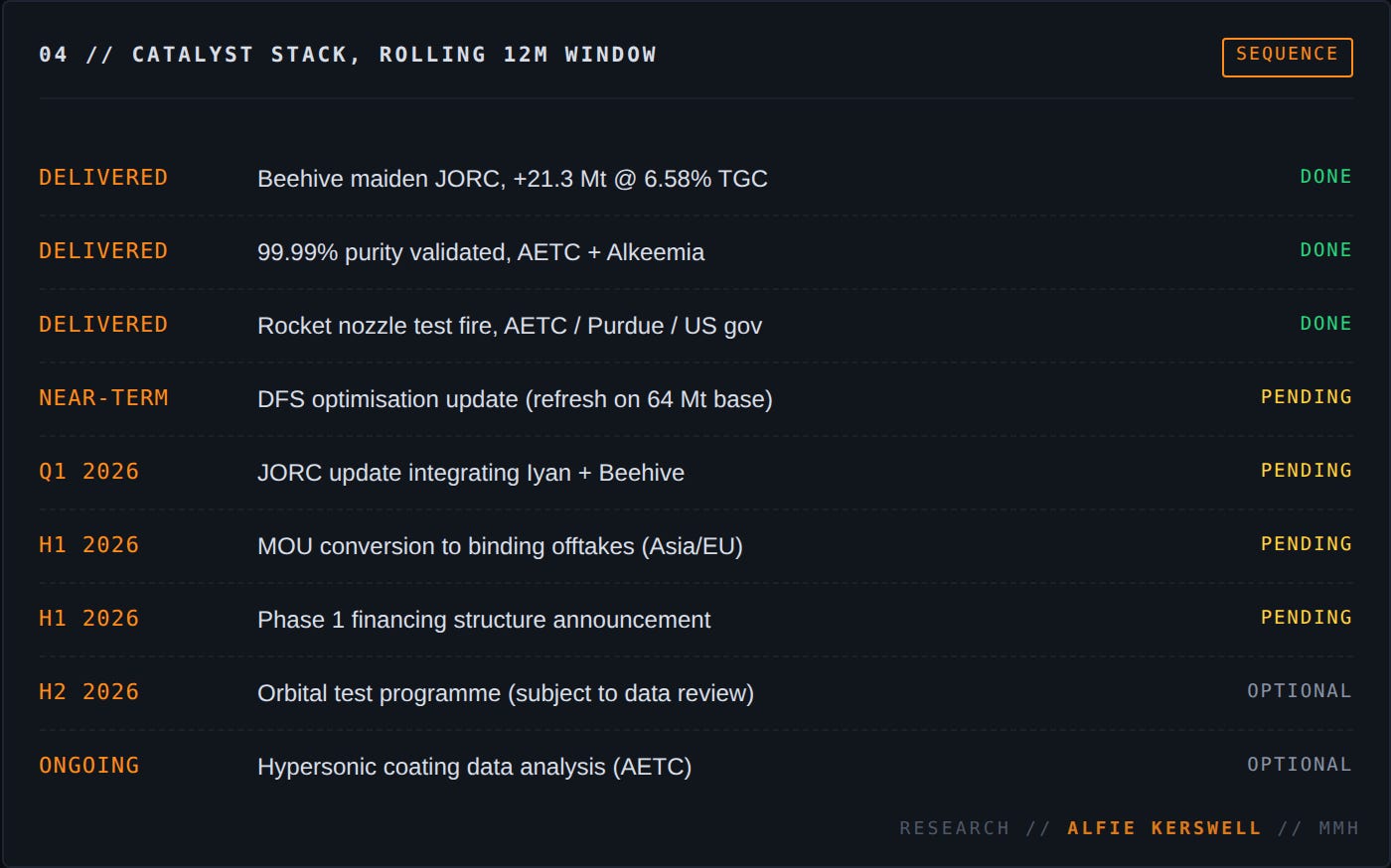

Beehive came in at 21.3 Mt at 6.58% TGC on its maiden JORC. That single deposit takes total Orom-Cross resources to 64.3 Mt at 6.03% TGC across Northern Syncline, Camp Lode, Iyan and Beehive.

Total resources up 168% since the start of Stage 7.

I’ll say that again because people skim past these numbers... 168%.

This changes the weight class of the project entirely. Different funding profile and different counterparties returning your calls. Different conversations.

The bit that should genuinely have people sitting up is that Beehive has only been modelled over about 22% of the anomaly, and largely in the upper 25 to 30 metres. Deeper holes have shown mineralisation continuing down to roughly 100 metres.

Then There’s the Rocket Test

This is the bit I think genuinely re-rates the company, and I don’t see it being priced in anywhere.

Blencowe’s graphite has been used in live rocket propulsion nozzle testing. In California. With representatives from US Government agencies in attendance, alongside Purdue University and Pluto Aerospace.

Let that land for a moment.

This is a ~£20m AIM-listed African graphite junior, and their material has been fired through actual rocket nozzles, in a live test programme, with US Government bodies in the room watching.

The work was done by American Energy Technologies Company (AETC), Blencowe’s Chicago-based partner. The question they were trying to answer was simple... could natural graphite from Uganda replace a portion of the synthetic graphite typically used in propulsion nozzles?

The test programme completed its planned runs successfully. Data is now being analysed, further testing is planned, and subject to outcomes, orbital testing is on the table for the second half of 2026.

In parallel, AETC has been evaluating graphite-based coatings on rocket fin components for hypersonic durability and icephobic properties (surfaces engineered to resist ice formation). Early performance has reportedly been encouraging, with potential applications across both military and civilian aerospace.

Now, I want to be careful here. I see people on Twitter getting wildly carried away with this kind of news, and I don’t want to overpromise.

“Testing” is not the same as “qualification.” And qualification is where the actual money is.

The graphite game works like this... aerospace, defence and battery customers test material for years. Then they potentially sign supply agreements. Then pricing power kicks in, driven by proven performance and supply scarcity. You don’t go from “NASA-adjacent rocket test” to “we’re selling at 5x commodity prices” overnight.

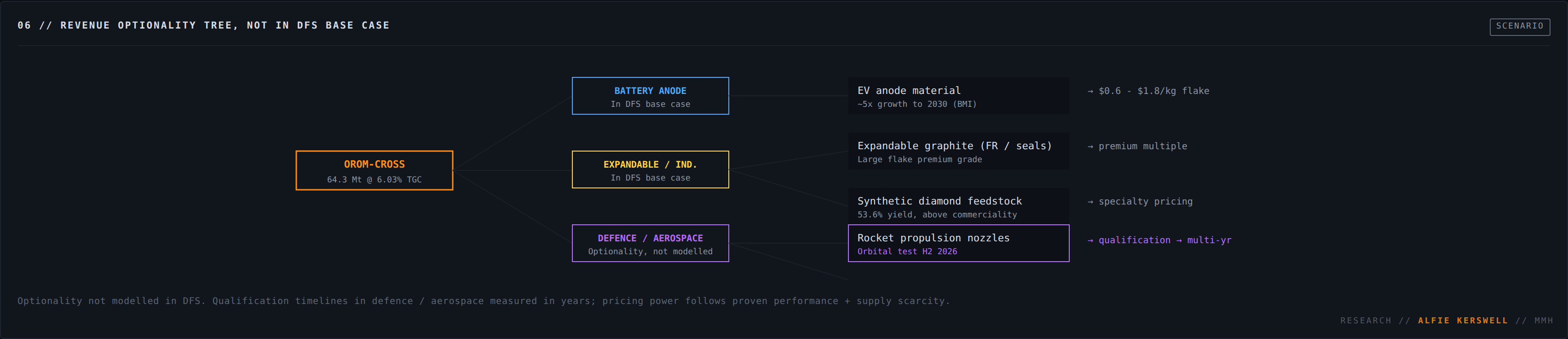

But the optionality being layered on here was not in the DFS. None of it was modelled. And it’s the kind of optionality that, if even a fraction of it converts, fundamentally changes the revenue model.

The Validation Stack Is Stacking Up

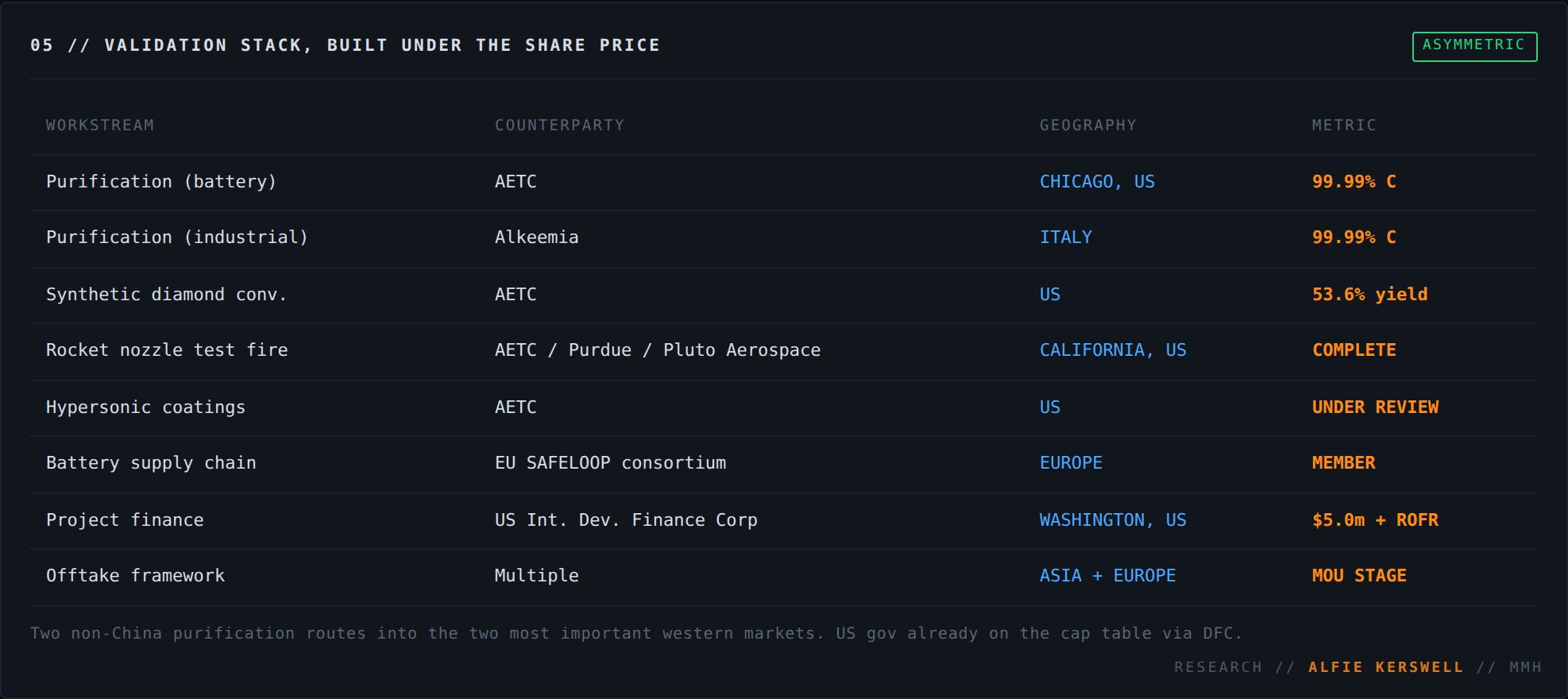

Step back and look at what’s actually been built underneath the share price over the last twelve months, because it’s quite a list:

99.99% graphite purity validated through AETC in the US and Alkeemia in Italy. Two non-Chinese purification routes into the two most important western markets.

53.6% yield on synthetic diamond conversion, which is above the 50% commercial viability threshold.

Live rocket propulsion nozzle test firing, completed successfully, with orbital testing potentially in H2 2026.

Hypersonic coating durability testing under analysis, with both military and civilian application potential.

A $5m grant in the bank from the US International Development Finance Corporation, with first right of refusal on project-level financing.

EU SAFELOOP consortium membership opening a path into European battery supply chains.

Offtake framework that already spans Asia and Europe.

64.3 Mt JORC resource with the next campaign almost certain to push it higher.

Market cap... still floating around £20m.

I genuinely don’t know how you look at that combination and conclude “fairly valued.”

The Cameron Pearce Quote Tells You Everything

Blencowe’s Executive Chairman put it about as plainly as a chairman can:

“The more value-enhancing strategic relationships Blencowe and AETC can build within US Government agencies, and associated technology providers, the more likely offtakes and/or funding from this direction.”

Read that twice.

That is the language of a company that has worked out it’s no longer just selling graphite. It’s positioning itself inside the US defence and aerospace supply chain, the one Washington is actively trying to detach from Chinese critical minerals.

Defence and aerospace validation gets you an entirely different class of strategic partner. Pricing conversations change. Offtake structures change. Strategic interest changes.

And the US Government already voted with its wallet via the DFC commitment. They’re not in this for a press release.

So What Does the Re-Rating Actually Look Like?

The re-rating thesis here isn’t built on any single announcement. That’s what I think people are getting wrong when they wait for “the catalyst.” It’s the stack of them landing in roughly the same window:

DFS optimisation update, where the bigger resource base and refreshed product strategy get re-presented in a sharper form... a JORC update properly incorporating Iyan and Beehive... conversion of existing MOUs into binding offtake agreements... Phase 1 financing structure announcement... further data from the rocket testing programme and the hypersonic coating work... and any movement on orbital testing for H2 2026.

Any one of those would move the share price meaningfully. Stacked together over a 6 month window, you’ve got the makings of a proper, sustained re-rating rather than a one-day pop.

The Honest Risk Section

This is still pre-revenue. It’s still AIM. It’s still African mining. Funding still needs to be properly structured, qualification timelines in aerospace and defence are measured in years not weeks, and graphite pricing has been volatile.

But the asymmetry is what makes it interesting to me. The downside is bounded by asset quality, government backing, and the simple fact that you cannot easily replicate 64 Mt of high-grade graphite with western political cover and a validated US purification route. The upside, if even half the catalysts land in the window I’ve outlined, is materially higher than where we sit today.

Bottom Line

Blencowe stopped being a normal junior miner the moment its graphite went through a live rocket nozzle test with US Government agencies watching. My view is that the market simply hasn’t caught up.

Watch the DFS optimisation. Watch the next JORC update. Watch for further commentary on the AETC programme. Watch for institutional names showing up on the register.

By the time those headlines are landing, the easy part of this trade will already be in the rear-view.

Thanks

Alfie