My H2 Outlook and Predictions

Reviewing the macro themes of H1 and my conviction view for H2

The momentum, the growth phase.

It’s starting.

I met with a young, hungry MMH subscriber earlier this week based in London and it his growth from reading these reports have been insane.

He’ll be joining the team to help with aspects of growth.

He’s one of countless members within MMH who continually keep in contact and share their progress so to you all, I say let’s continue growing together!

I know what you’re thinking.

How can you get involved?

The expansion plan is not yet in full motion, so when it’s fully underway I’ll look within my audience as well as industry pro’s to build the go to platform.

As always lend me your attention as I go through my outlook and review H1:

H1: ‘The resurgence in global liquidity’

If there was any one theme I could give the first half of the year that best describes what we’ve seen in markets.

That would be it.

I’ll explore the slowdown in growth we’re experiencing as that has been a predominant theme across H1’23.

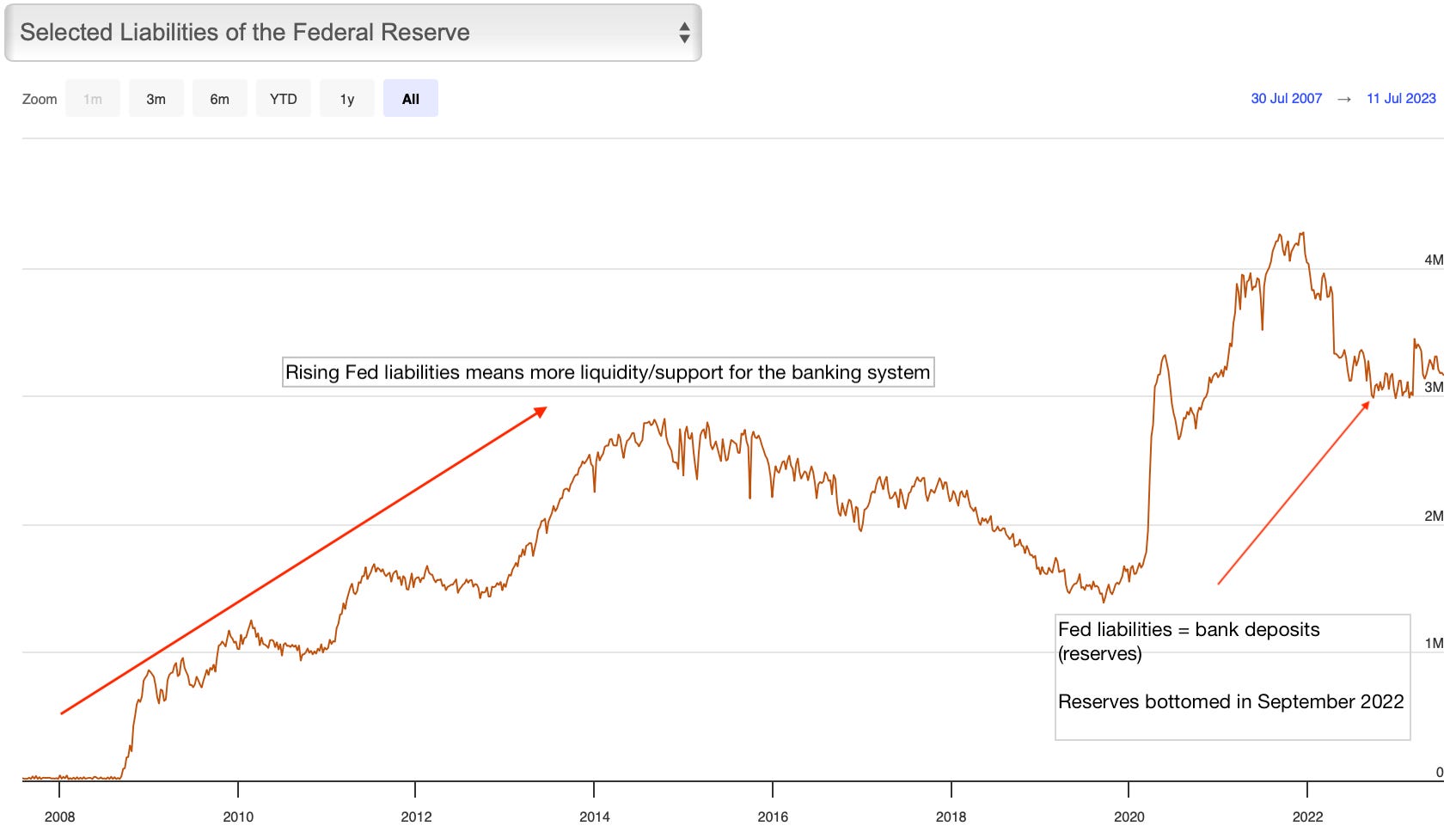

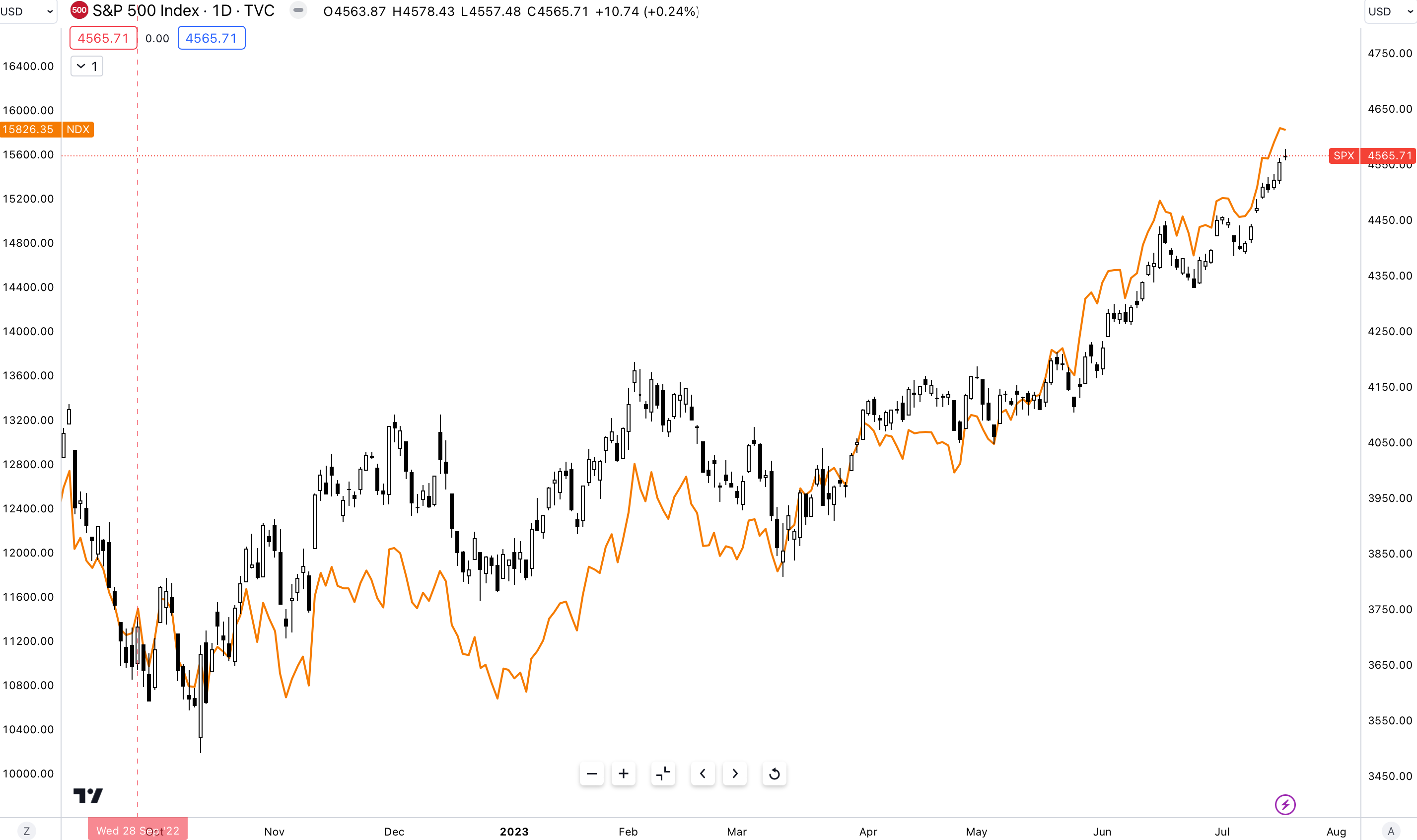

Dating back to September 2022, a date which I would call an inflection point in macro, global liquidity bottomed, markets were in the red and there was minimal prospect for growth. But, it was within the month of September that liquidity begun to re-enter global markets.

Take a look at figure 1.

During the GFC crisis that marked the first ever round of QE for U.S markets, which resulted in Fed liquidity going from just above $10b to over $1tr by 2012.

I’ll simplify what ‘Fed liquidity’ means and why we’re looking at Fed liabilities for that.

The reason we’re looking at Fed liabilities is because central bank liabilities is mostly compromised of bank deposits and reserves which is a form of liquidity to the financial and banking system. As a reminder, the more reserves within the banking system, the greater the money supply within the economy.

The bottom in Fed liquidity came just after the Gilt market and pension fund crisis in the UK, which raised the worries about a contagion risk in other bond markets around the world. Result? The Fed no longer reduced or tightened financial conditions, primarily liquidity like they promised they would during QT. I call that silent easing.

US equities bottomed and have since returned 37% YTD for the Nasdaq & 18.91% for the S&P 500.

It would be ignorant of me not to reference the China re-open and the effect the PBOC have played thus far within global markets.

PBOC stimulus

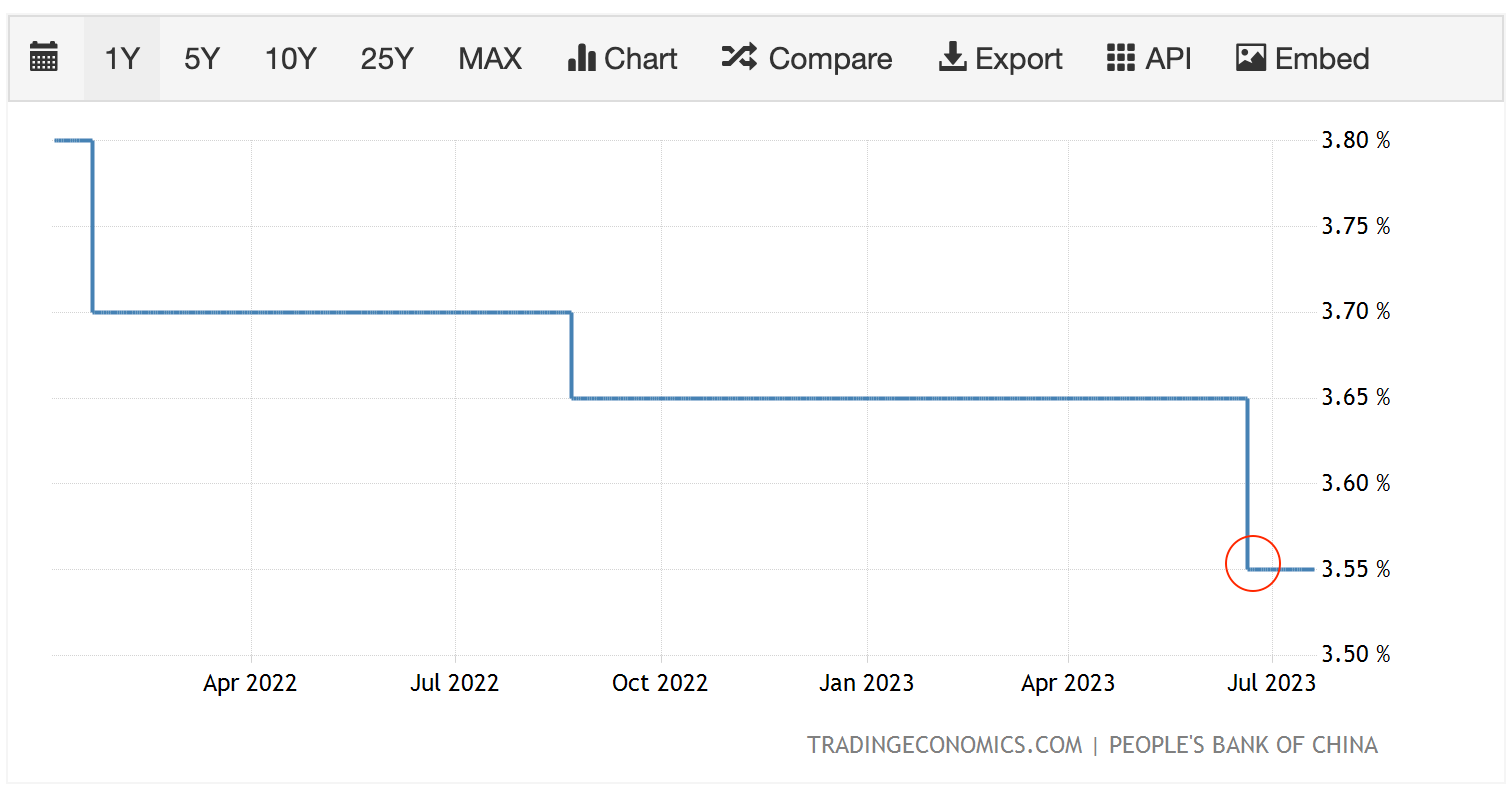

Alongside the PBOC announcing the re-opening, they also announced their aggressive stimulus plan to jolt their economy back into action. Now although that has failed thus far, with Chinese GDP coming in below expected, at 6.4% vs 7.3%, investors still played out the China re-open trade in markets.

Take into consideration the PBOC has cut its loan prime rate to further boost spending and economic activity within the mainland China.

A number of key prime interest rates within China have been slashed as hopes of a strong rebound fade.

PBOC Currency Intervention

As mentioned in my currency intervention report the PBOC sets the daily midpoint for the Yuan every morning, allowing the Yuan to fluctuate +/-2% from the currency band it floats within. Very similar to the YCC Japan implements within its JGB market (Japanese Government Bonds).

The 27th June, the PBOC set in motion the currency intervention operation, followed by state banks who sold Dollars to buy Yuan in the offshore spot market. The intervention reveals a fundamental issue within the Chinese currency and economy; with the Fed expected to continue tightening from next week, the only prop for the Yuan holding it up is the market’s expectation of further support and stimulus from the PBOC which long term isn’t a sustainable or healthy currency strategy.

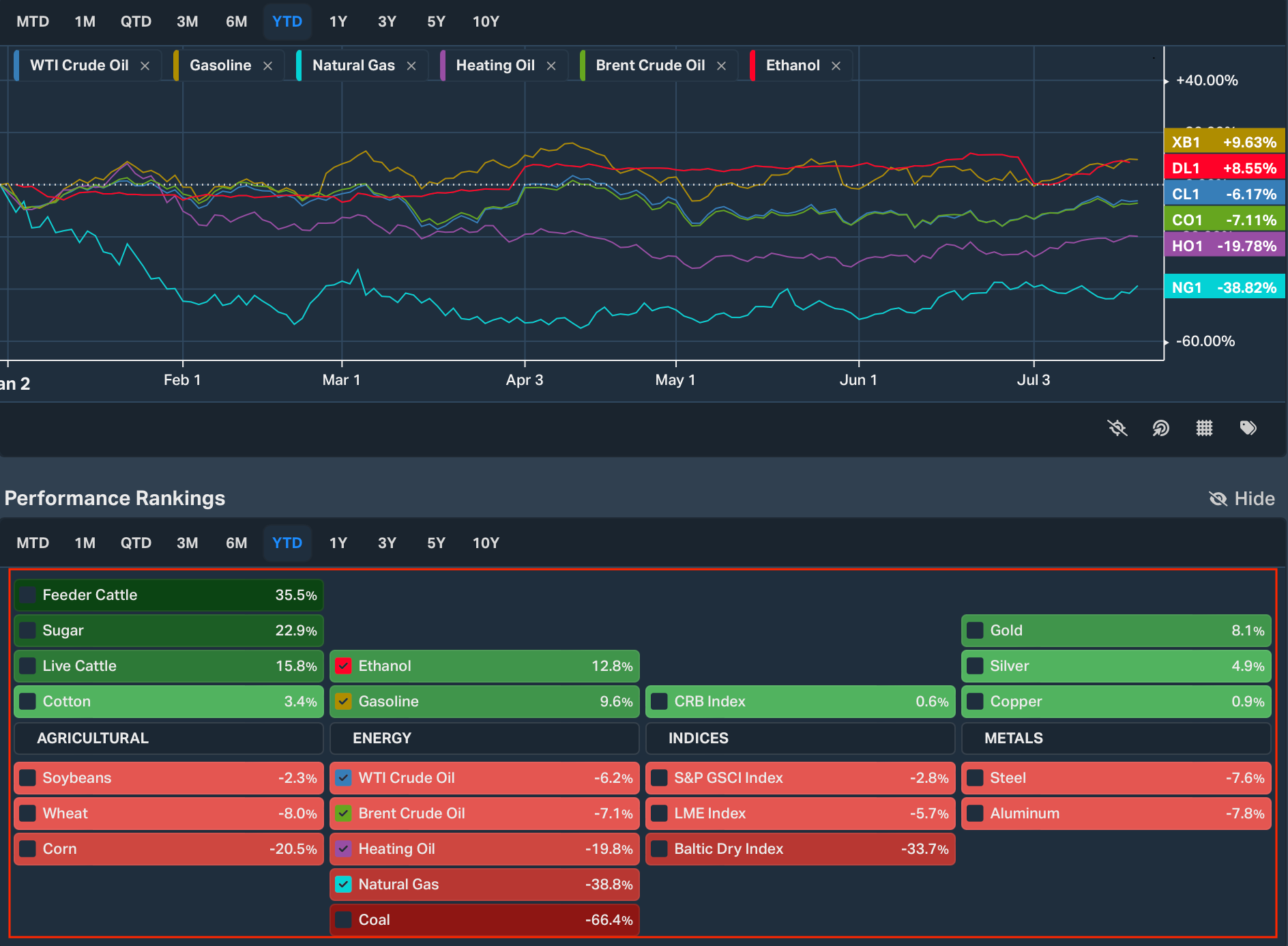

‘Fade Commodities’

If you were looking for the clear short across H1 then commodities, notably energies, would have been the clear trade. YTD you can see the likes of Crude Oil down 6%, Natural gas down -38% and Coal trading at a huge discount. Aside from the fact that commodities were trading at premiums, we’ve entered a deflationary period globally which isn’t an environment commodities tend to perform in.

Within the U.S inflation has come down from the highs of 6.1% to now 3.0%, Euro Area CPI is now just 5.50%. Something that will present some FX opportunity later this year, I’ll explain in the second half of this report.

A deflationary environment is not practical for commodities as we know. Commodities rely on reflationary cycles, strong global growth and increased global consumption/demand for them to perform well. Something which we won’t experience for the rest of this year in my opinion.

So my bias on commodities remains bearish going into 2024, I don’t see any high probability catalysts that can contradict this viewpoint aside from a strong H2 China rebound or global inflation resurgence which is increasingly unlikely.

My Forward Outlook

Let’s start with our favourite currency index. The DXY.

As we discussed below:

The dollar was and still remains my conviction short play throughout 2023, something that has played out very well since mentioning it. We’ve broken below the 100.00 base value mark so let me explain from a macro positioning why this is a clear short for me.

That starts with the US02Y.

Since the ADP figure, and soft inflation data from the U.S, we’ve seen both the dollar and treasuries declining. Not many people know which one is the cause and which is the effect so let me explain what is going on and my viewpoint; as government yield rise, we know that means investors can get more for their money when parking it in U.S debt markets, resulting in the dollar moving higher.

However, we’ve seen the dollar selling off heavily of recent. What this shows is simple, investors are dialling back their interest rate expectations for the U.S economy resulting in a flow away from the dollar into other currencies, like the Euro or Pound.

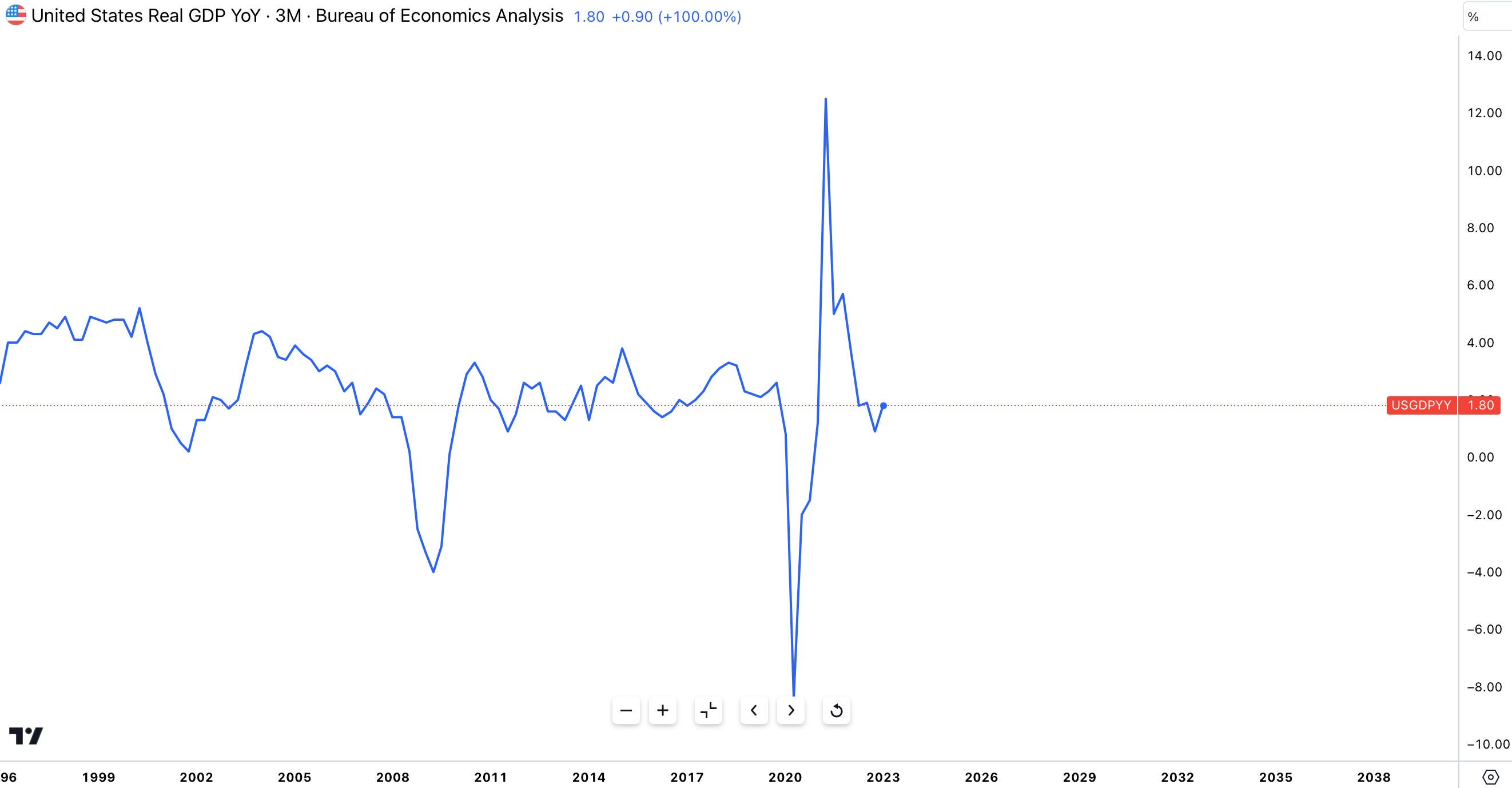

Put simply, this environment is exactly the middle of the dollar smile theory I shared with you all, there is no reason for the dollar to rally past 103.00 unless we have a drastic turnaround in inflation. Real GDP is below trend at 1.8%, the Fed is “close” to the end of their tightening cycle according to Mary Daly, President of the Federal Reserve Bank of San Francisco.

So the dollar is set to take a seat back as investors not only flock to other currencies but explore opportunities within emerging markets equities and FX. EM/FM (Emerging & Frontier markets) tend to perform best in a weak dollar environment, so keep an eye out for EM currencies making a return this half.

My Long Euro Viewpoint

The Euro is another simple yet effect proxy trade of dollar weakness. I expect to see further Euro strength until we see a narrowing in the spread between Euro Area and U.S inflation. Right now the spread is 2.50% (Euro area inflation - U.S inflation), with an interest rate differential of 1.25% soon to been 1.50% after the Fed hike in 7 days. With this understanding, this is a short-term macro play on the Fed coming to an end in their tightening cycle and the ECB closing in, both on the interest rate but also inflation rate, resulting in higher rates for the Euro.

I expect both President Lagarde and other ECB members to continue and hold their hawkish stance on monetary policy as we’re seeing a fight for 2% inflation.

Yen Longs…potentially

You read that right.

I’m evaluating longs for the Japanese Yen.

Reason? During the 2-day central bank summit in Sintra, Portugal, Governor Ueda made a very important statement which went unnoticed. Ueda has commenced a policy review for the Yen. We’ve reviewed how crucial the current level the Yen trades at is, but that’s only from a technical aspect. Ueda emphasised how a hawkish Fed, and neighbouring central banks, puts downward pressure on the Yen making it increasingly difficult for the domestic economy to reach growth and inflation targets. A weaker Yen drags economic activity lower because it makes it increasingly expensive for domestic businesses to export their goods abroad, lowering future growth.

This has already been flagged up by Kuroda and other central bankers.

Courtesy of a weak dollar, the Yen has already begun to gain strength against the dollar. However, I expect this to increase as the BOJ, Ueda, and MOF review their currency and monetary policy stance.

I appreciate you reading until the end.

I know this was a longer one, but it’s always important to review markets after each quarter, half and look forward making clear high level viewpoint.

I will delve into the nuances of each macro view and go into much more detail as they evolve, for now this is a bird’s eye perspective on what I’m watching within FX markets, commodities & rates.

Until next time

A pretty interesting chart is total China retail bank deposits and China saving rates (there are multiple but broadly). They are actually inverse - as rates come down the number of bank deposits increase. That is why China simply can't "stimulate", they have a structural issue of saving due to the bulge in population retiring. Reducing taxes like VAT is their better option.