Low Growth Risk, Weakening Inflation Risk

The war premium is leaving energy, and it's taking inflation with it

Credit Markets Confirm Low Growth Risk

I have laid out for a while how I believe growth risk is EXTREMELY low and the credit market is confirming it (and has been for a while). HY and IG spreads are at cycle lows, which tells you credit isn’t sniffing any growth deterioration. Breakevens have started drifting lower too, with the 10Y BE down 11bps and the 5Y down 30bps over the trailing period (even after the oil shock). That combination of compressed spreads and falling inflation compensation is EXACTLY what you want to see in a Goldilocks read… the bond market is agreeing that the growth/inflation mix is improving.

Inflation risk remains larger than growth risk, but neither are a concern and inflation risk IS declining in my view.

Labour Market: The Bear Case That Never Arrived

The labour market has been the consensus bear case for two years and it hasn’t delivered. Payrolls have normalised well off the post-covid surge but the underlying pace has been remarkably stable. The 5-year picture shows a jobs market that decelerated in an orderly way rather than rolling over, and the 2-year detail shows that even through the tariff shock of early 2026, the dip was sharp but brief. Claims are still historically low, openings remain above 7.5 million, and layoffs are actually trending DOWN. Wages are firm but not accelerating. This is a mid-cycle labour market, not one that’s cracking.

This all reinforces my view on growth.

Growth risk is low precisely because the labour channel is holding. Consumer spending runs through employment and wage income, and both remain intact. I’d need to see claims pushing well above 250k and sustained negative payrolls prints before the growth picture genuinely deteriorates in my view.

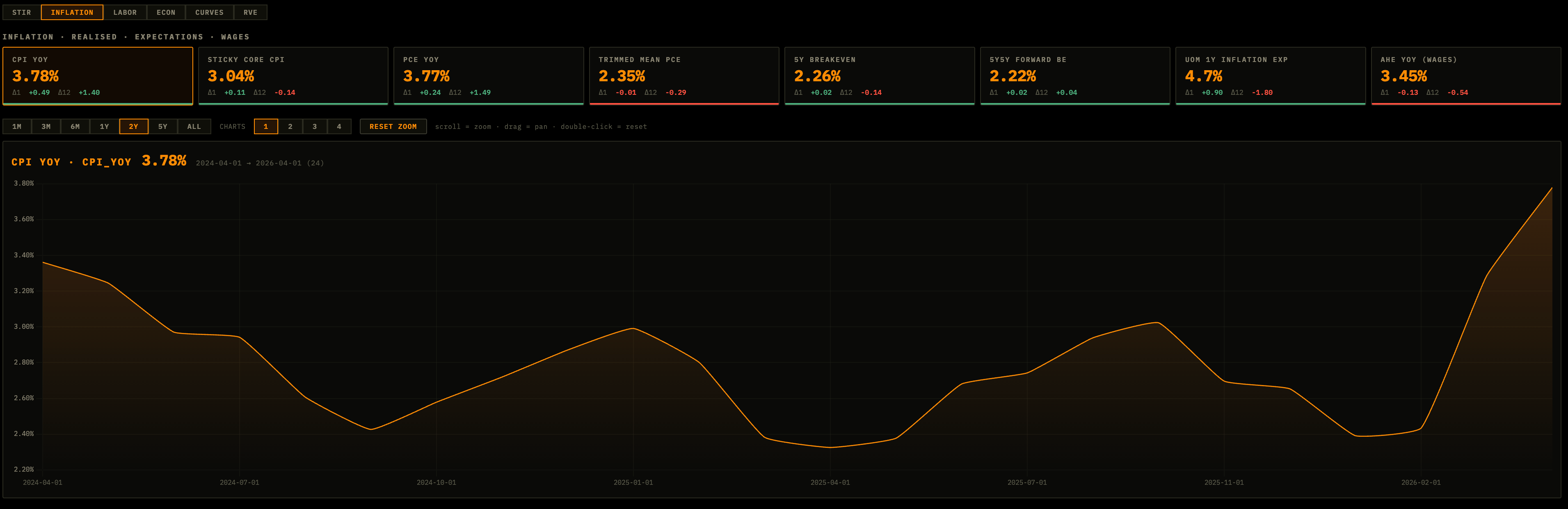

Inflation: Where the Real Asymmetry Lives

The inflation picture is where the asymmetry lives (and I’ve laid this out in the Substack chat). After a clean disinflation window through 2024, price pressures have re-accelerated across every major measure. CPI, core PCE, trimmed mean PCE are all running well above the Fed’s target and the 2-year trend is moving in the wrong direction. The tariff impulse (old news…) has fed through into goods prices, services have stayed sticky throughout, and the re-acceleration has happened even WITHOUT a demand boom driving it. That’s the uncomfortable part because this is a cost-push dynamic that’s harder for the Fed to address without breaking something.

The long-run chart gives you the historical context. Every sustained inflation episode above 3% has needed either a policy response serious enough to cause demand destruction, or an exogenous price shock to reverse it. We came off the sharpest tightening cycle since Volcker, got a disinflation window, and are now re-accelerating. The Fed is stuck: growth is fine enough that cuts aren’t justified, but inflation is high enough that further hikes would be a political and economic problem. Rates stay higher for longer (and that’s the dominant macro constraint on the cycle right now).

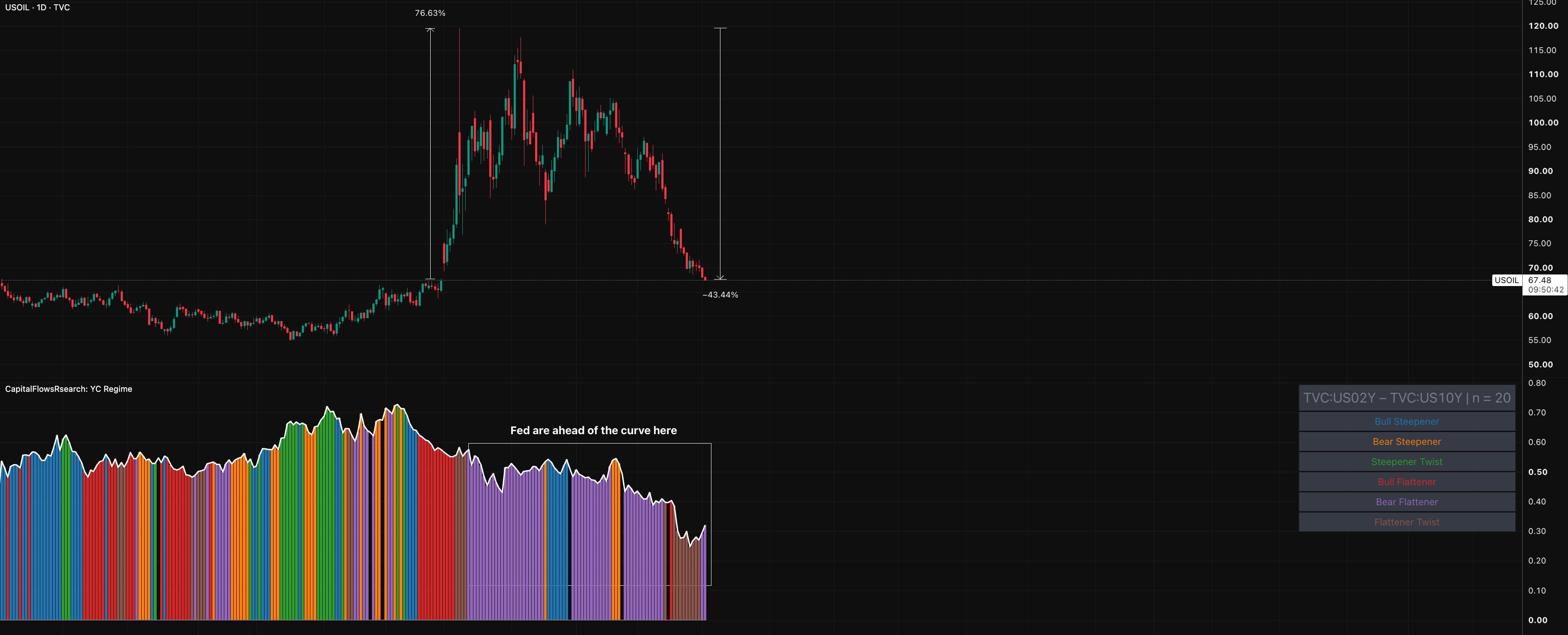

Oil as the Relief Valve

The one genuine relief valve on the inflation side is oil. Crude has fallen over 43% from the Iran war peak and is sitting just below $68, with the yield curve regime shifting toward bull flattener territory as the market starts pricing the Fed ahead of the curve. As oil continues to deflate, it mechanically pulls headline CPI lower and gives the Fed breathing room without requiring any policy action (unless growth crashes fast).

The important nuance is that this relief is coming from the supply side, not demand destruction. Energy deflation with a stable labour market and intact consumer is a clean disinflationary impulse, and it’s the main reason the inflation risk, while still elevated, is gradually becoming more manageable rather than less.

The Forward CPI Path

The forward CPI path reflects exactly this dynamic. The base case trajectory shows headline CPI continuing to drift lower through the second half of 2026 as energy base effects kick in and the war premium fades. The 3-period pace is already decelerating. The risk is that services and shelter keep the floor elevated, which is why the forecast range is wide and skewed to the upside. Inflation coming down is the base case, inflation returning to 2% quickly is not.

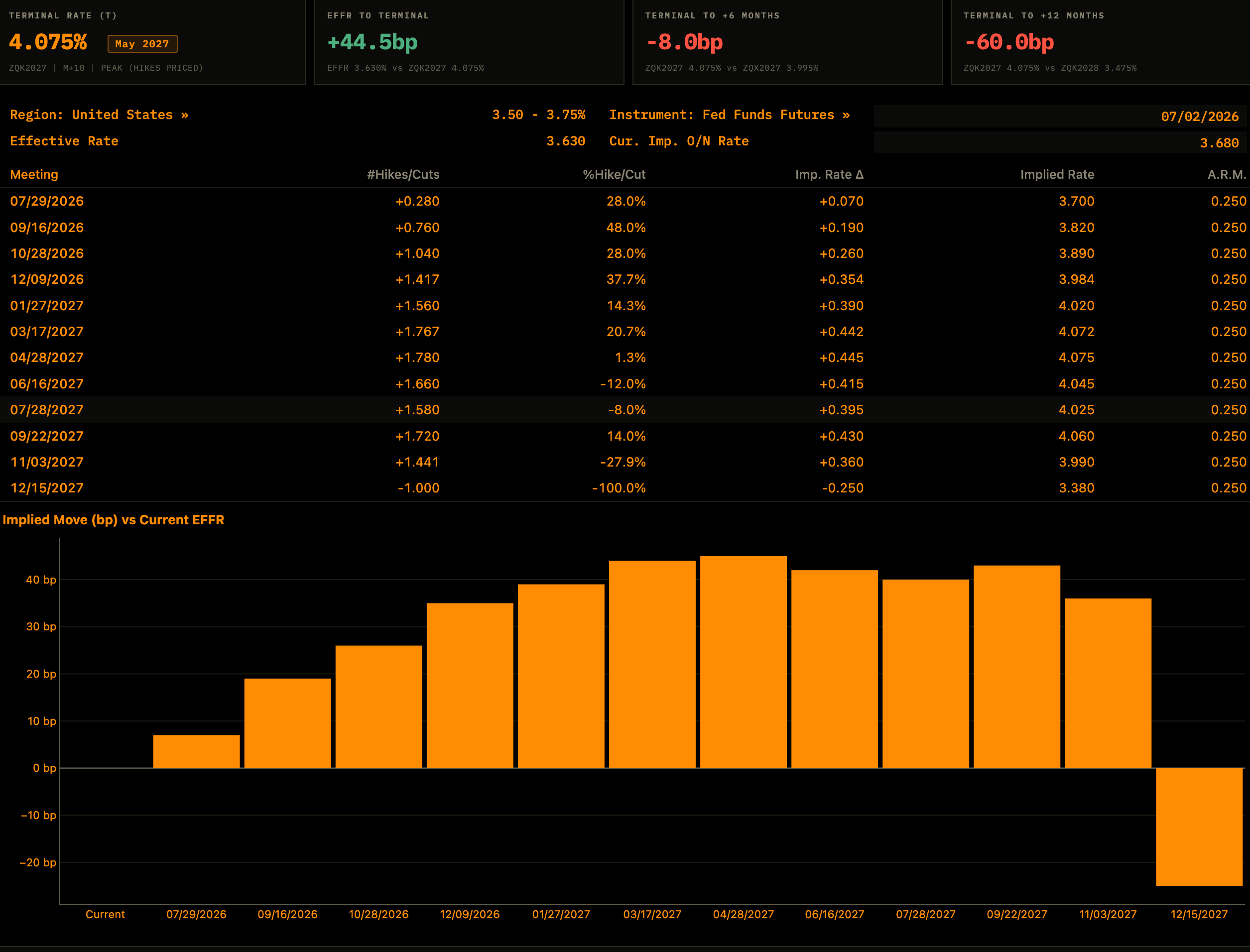

Rates Market Pricing and the H7 Trade

Now when we look at the US forward curve, I think it’s highly unlikely that two hikes are delivered given my explanation above. I see most assymetry in trading the H7 contract because if the market repices this forward curve (which is my view), then I believe that contract will shift most as the terminal rate has been floating aorund that contract for a while.

The rates market is pricing the Fed to hike once more before cutting, with a terminal around 4.075% by May 2027 and then 60bps of cuts in the 12 months following. That's a meaningful repricing from where the market was at the start of the year when cuts were expected imminently. The message from futures is that the Fed is on hold, inflation has to show sustained progress before easing begins, and the first cut is well over a year away. That's consistent with everything the data is showing: a resilient economy, sticky services inflation, and an energy complex that's helping at the margin but not enough to unlock policy. The bar for cuts is high, and the market has finally accepted that

Asset Class Outlook: Equities, Rates, and Dollar

Equities remain tilted to the upsise in this environment, in my view. Compressed credit spreads, a stable labour market and falling energy prices is about as clean a backdrop as you get for risk assets, and the S&P 500 structure reflects that. The inflation risk is real but it’s a slow burn, not an acute earnings threat, and the market is correctly treating it as such.

On rates, the 2Y looks capped from here. The Fed is on hold, the terminal is priced at 4.075% and the market has largely accepted that cuts are a 2027 story. There’s not much juice in fading the front end. The 10Y is more interesting: if oil continues deflating and headline CPI rolls over through H2, real yields stay elevated but nominal yields have room to drift lower, which makes duration selectively attractive as a hedge rather than a core position. On the dollar, the stagflation fear trade that drove USD bids earlier in the year is unwinding alongside the oil premium.

Growth holding and inflation easing is not a strong dollar environment because it removes the rates divergence argument. USD likely grinds softer from here, particularly against currencies where central banks have more room to stay restrictive

Thanks

Alfie