Lessons From The Turkish Lira Crisis

A deep dive into the Turkish Lira and the lessons we can take away following President Erdogan's re-election

Hey guys,

May was one heck of a month in markets.

Speeches, debt ceiling, fear, volatility and risk— all at the same time.

A beautiful war.

Anyways, the TRY is a currency I’ve been following from afar as well as the Turkish macroeconomic policy, which happens to be one of the worst I’ve come across.

So I’ll be breakdown the major reasons behind the Lira’s collapse and what lessons you can learn from this:

Turkey’s Macro Climate

From the 1960s to 2022, the average inflation rate in Turkey was 32.6% per year. Meaning that an item that would have cost you 100 liras in 1960 would now cost you 1.06 billion liras by 2023.

Let me put that into content for you, an item that would have cost you £100 in 1960 would only cost you £1,869.39 today in 2023 for the UK. That’s the detrimental power of inflation.

There’s a list long enough to fill the room as to why the TRY has depreciated so much, but I’m going to start with a country that failed to take control of its current account deficit, fiscal and monetary policy.

Over recent years, the Turkish economy has been brought to its knees by bad monetary policy, a weak fiscal policy and running a growing trade deficit. Turkey is a net importer of energy, importing from Russia (43%), Iran (17%) and Iraq (13%), meaning that as energy costs have spiked higher this has worsened the ongoing inflation battle depleting the country’s current account.

Before I break this down let me explain the importance of the balance of trade to an economy, particularly for their currency.

Balance of trade is another term for trade balance. Meaning, the difference in the sum of all imports minus all exports. Pretty explanatory that a trade surplus means that the country is exporting more than it imports and that a trade deficit means the country is importing more than it exports.

Here’s how it affects the exchange rate.

When an economy has a trade deficit, this is what you should think— there’s an increased domestic demand for foreign currencies, which puts downward pressure on the domestic currency since consumers and businesses will have to sell their Lira to purchase Euros. When a country has a trade surplus, that means there’s an increased foreign demand for that country’s currency in order to purchase goods from the country.

So in this case, Turkey’s widening trade deficit makes exporting goods even more expensive for businesses, as it would now take more of the domestic currency (Lira) to buy a unit of the foreign currency.

So, when you see a currency losing value at the rate the Lira has it can boil down to these three points below:

Political instability - If the political environment isn’t ‘market friendly’ then there would be little to no foreign investments into the country resulting in a lower trade balance.

High government debt - With unsustainable levels of debt the Turkish government hasn’t been able to raise debt from abroad in order to finance its existing trade deficit.

Weak monetary policy - Complimentary of the two prior points, the Turkish economy has kept monetary conditions loose in an environment where the central bank should have tightened till conditions were restrictive.

Weak Monetary Policy & FX Intervention

It’s no surprise that the Lira has plummeted off the face of the Earth. However, many traders don’t really understand what key instances have contributed to what may be an irreversible mistake.

CBRT = Central Bank of the Republic of Turkey

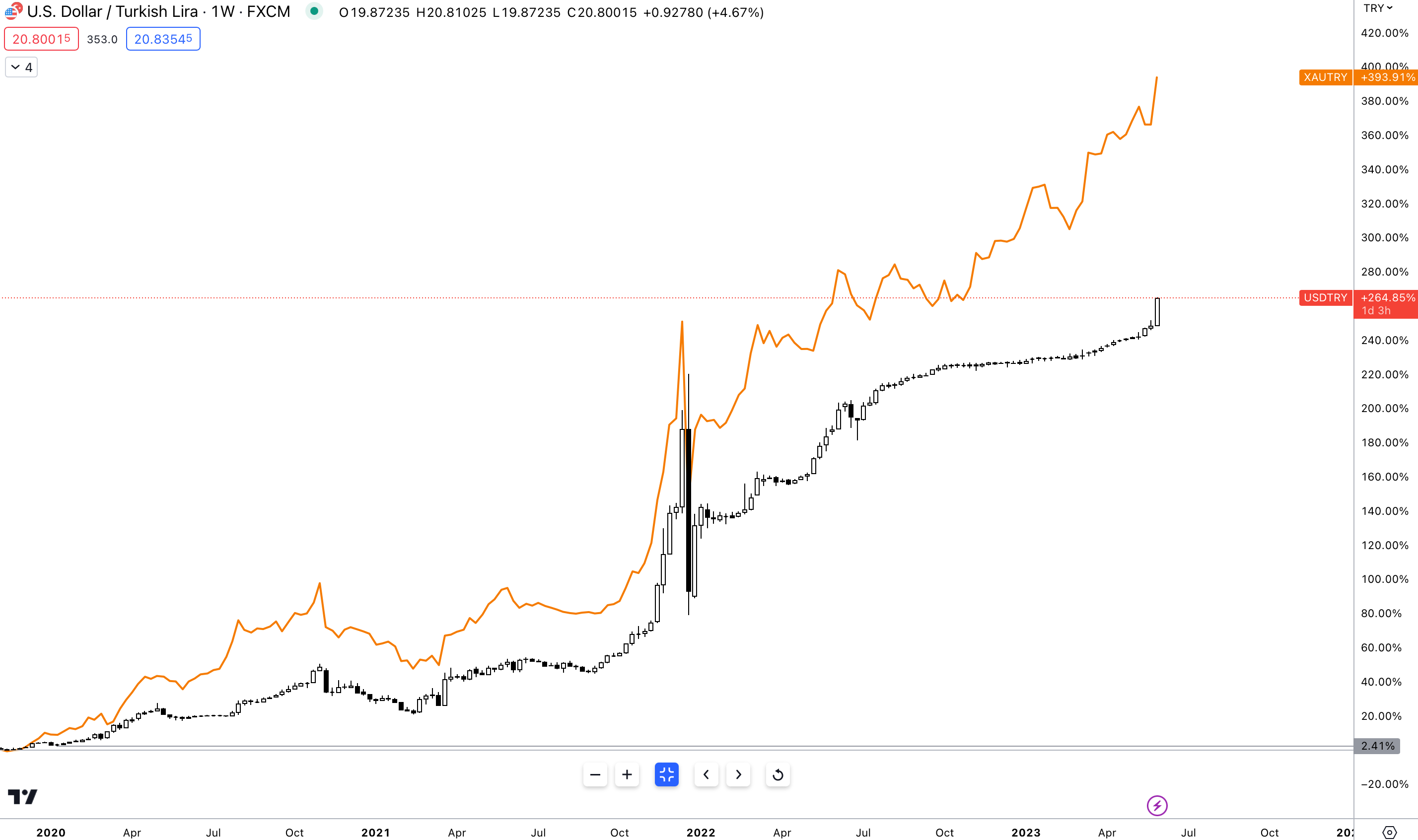

Take a look at the chart below.

USD/TRY

XAU/TRY

The reason I have added gold priced in the Turkish lira is to prove the point that the colossal depreciation in the Lira isn’t because of Dollar strength or any other silly reason there is, but rather because of the CBRT’s weak monetary policy decisions which have caused the price of gold in Lira to soar to over 40,000 Lira/per ounce.

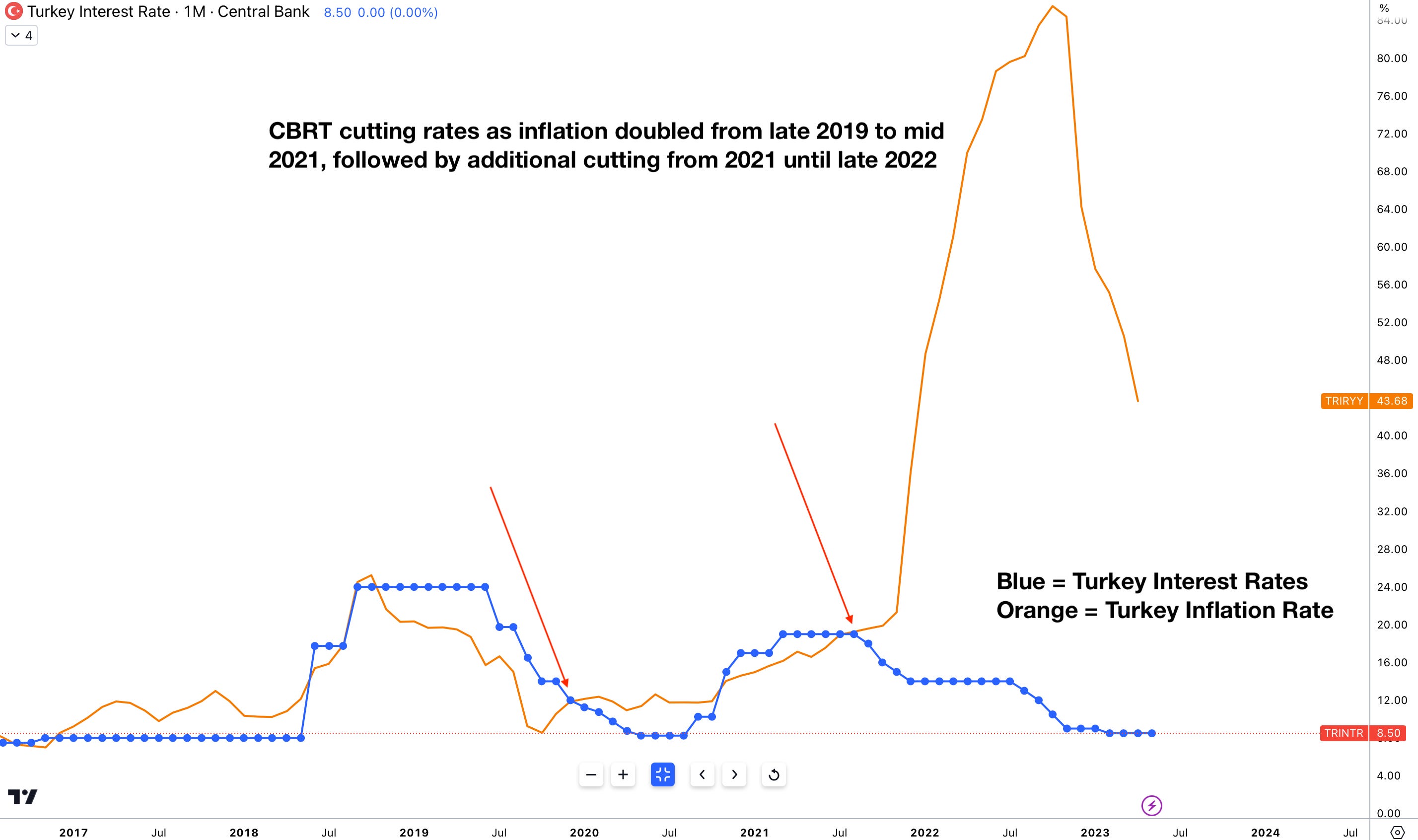

President Erdogan sits at the heart of the Turkish crisis, elected as the President of Turkey in 2014 till date, Erdogan has been the face of monetary policy decisions.

His most notable monetary policy actions are below:

Cutting interest rates during periods of high inflation

FX intervention to prop up the Lira

Dictating all central bank activities

Failing to understand the basic laws of macroeconomics

Since 2020 Erdogan has fired four central bank governors who either raised interest rates during soaring inflation (the right thing to do) or refused to lower interest rates as inflation soared (also the right thing to do).

Ridiculous.

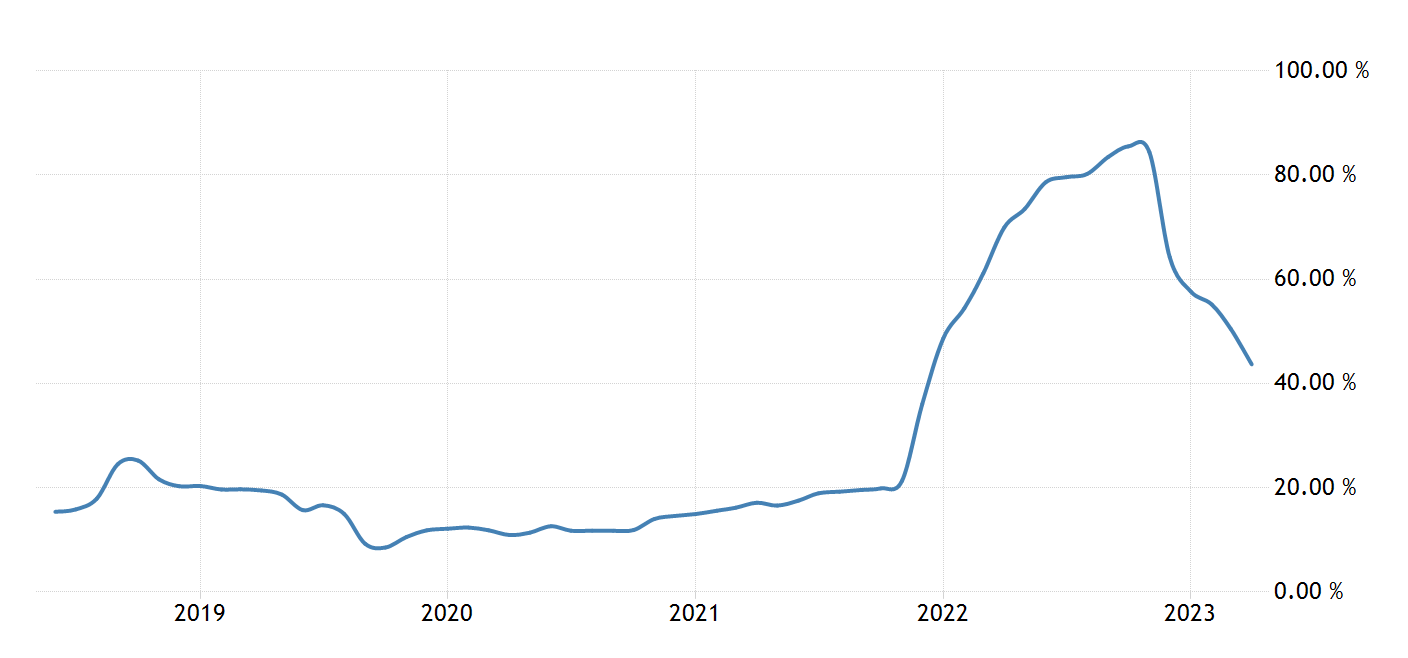

This is the 5y rolling inflation rate in Turkey, the chart below is inflation vs interest rates across the same period.

The President of an economy worth trillions can’t even get his head around the connection between interest rates and the relative strength/weakness of the Turkish Lira.

During both scenarios, Erdogan forced the CBRT to cut interest rates sending the Lira into freefall. In order to try and save the TRY the CBRT has imposed capital restrictions and implemented direct FX intervention, almost depleting their FX reserves to keep the Lira from imploding.

This is how all the macro points listed above intertwine. Due to Turkey’s weak monetary and fiscal policy, the economy experiences unsustainably high inflation and debt. Not only does their economy experience high inflation and government debt but due to heavy reliance on imported goods (mainly energy which accounts for c.74% of total imports), this results in a negative trade balance. From here the story gets worse, a negative trade balance means that the country has fewer FX reserves in its accounts/balance to defend its currency against major FX moves.

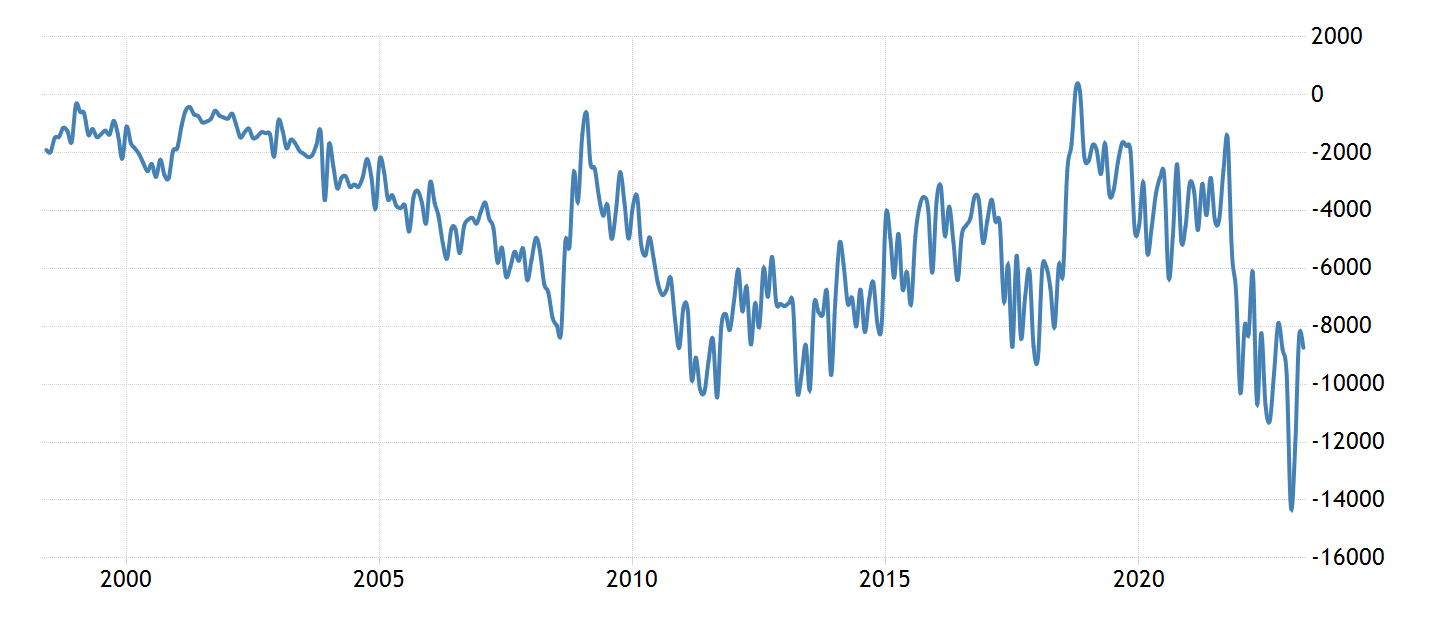

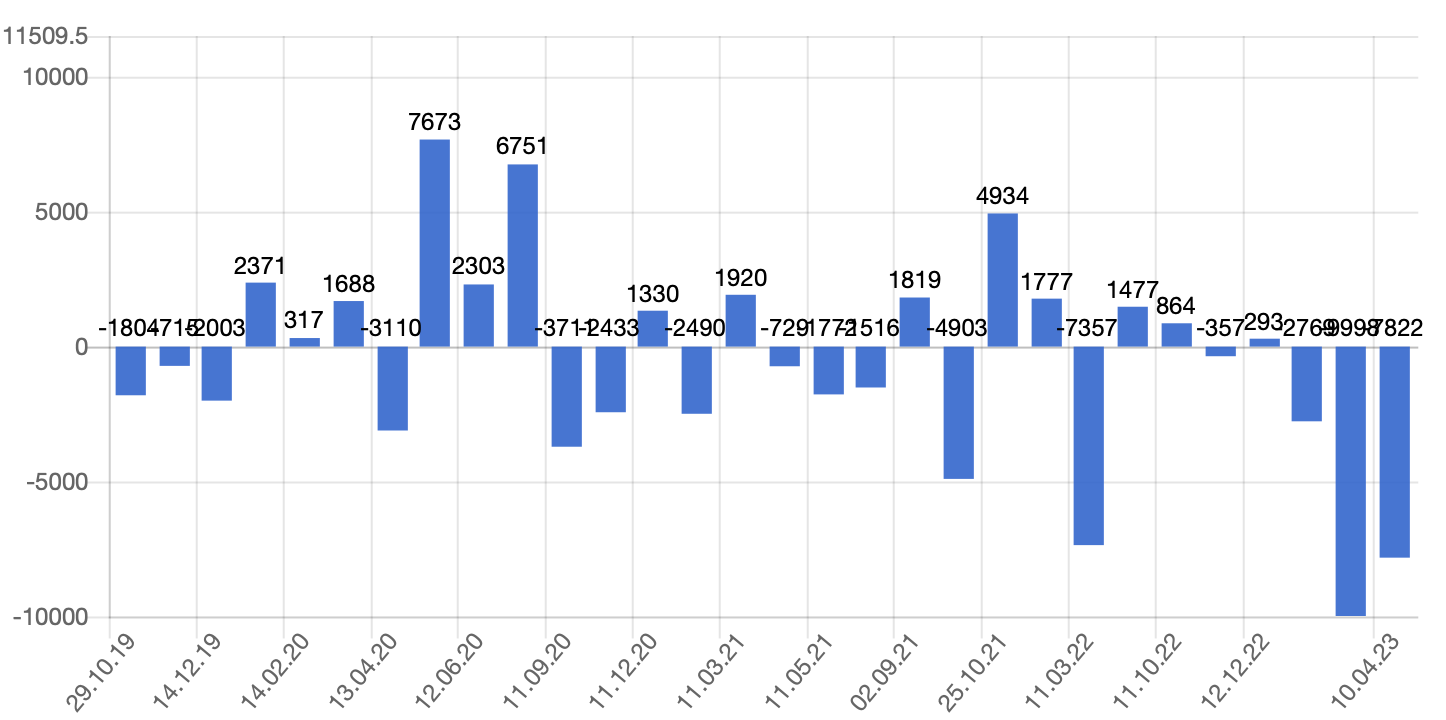

Capital Flight, Rising Private Sector Debt & Lessons

Below are Turkey’s capital flows (USD Millions).

Due to all the reasons listed above it’s a no-brainer to expect capital flows to Turkey to be negative with wealth leaving the country at every opportunity.

Capital flows decreased by $7.8bn USD in February 2023 according to the CBRT.

As inflation has remained elevated, this has forced businesses within Turkey to raise debt financing in foreign currencies with 60% of long-term private debt issued in USD, accounting for c.$149bn as of 2023.

The reason I highlight private sector debt is because debt when issued in a non-domestic currency adds external risks to those companies, everything from interest rate risks to currency appreciation and even political risk.

If a Turkish company has borrowed USD and the U.S raises rates the dollar is bound to appreciate against the lira which makes the total repayable debt higher for the company.

From this report, I hope you’ve been able to gather a deeper understanding of how important monetary and fiscal policy is important in keeping an economy functioning well.

That’s it for today, but I’ll be back next week!