Fear In Risk-Assets Push DXY Higher

Risk-off or equity capitulation?

Dollar surge and G-7 currency performance

BoE warns of recession and sees inflation reaching 10% by Q4

Red across major U.S equities

What seemed to be the cue for risk to re-enter markets proved short-lived after markets wiped out all gains made on Wednesday’s comments. The S&P faired its worst day since March ‘20 alongside the Nasdaq which closed down more than 6% for the day.

Jerome Powell delivered a speech yesterday that temporarily had the bulls bursting out of the cage but that didn’t last very long; traders’ concerns resurfacing about the Fed’s ability to control inflation were not answered by Powell leading to a consensus that this was a communication mistake.

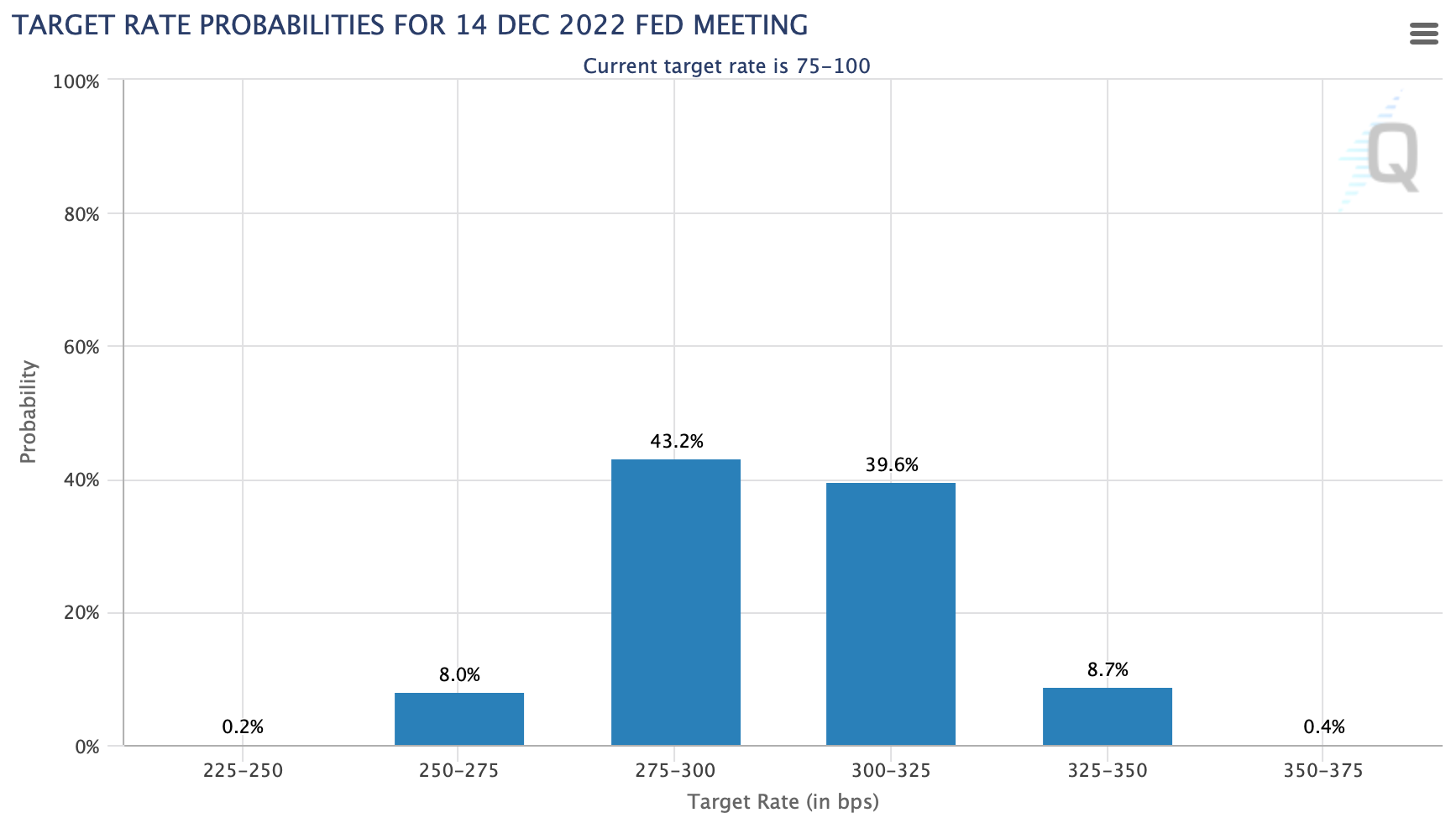

The probability of the Fed Funds rate by December 2022 has shifted towards the 275-300bps range.

Currencies outlook

In the current macro landscape, we’re in it’s hard to find a sector to park your capital when markets are in this phase. When there seems to be no trade there’s only one other option, you guessed it right, go into the dollar.

The dollar managed to close up by 1.2% after investors fled risk assets and moved into cash positions. The BoE delivered another dovish policy meeting after hiking rates to 1.00%. There is a clear division within the central bank as three members opted for an even greater rate hike to curb inflation which Andrew Bailey said is poised to reach 10% by Q4.

An even dimmer outlook for Uk citizens as Bailey stressed the “pain” that would be felt by lower-income households caused by ongoing disruptions in Russia.

It is clear from this chart how the BoE has consistently been behind the actual print of inflation when looking back.

The pound traded to new two year lows of 1.2350

Eurodollar is holding onto the 1.0530 handle as mentioned in yesterday’s article

As rates rise and inflation continues to break records the dollar poses the only “safety” like feeling as commodities such as gold tend to perform best in periods of stagflation (low growth, high inflation) accompanied by low rates.

Gold as we know it is an inflation hedge only up until central banks do exactly what they’re doing now, raise interest rates. This forces investors to realise the opportunity cost of holding onto a non-yielding asset which is what we have seen occur as the Fed has raised rates.