Equities Are Shrugging Off Everything That Should Be Killing Them

Why equities are ignoring dollar strength, rising real rates, and long-end pressure, and what it means when they stop

Both the short-end and long-end are rising (while curves are flattening across the board), yet there has been no drag on equities. The dollar has also been rallying.. so we’ve got the dollar up, rates up and equities up. The quesiton everyone is asking is, why is neither the dollar or rates dragging on equities?

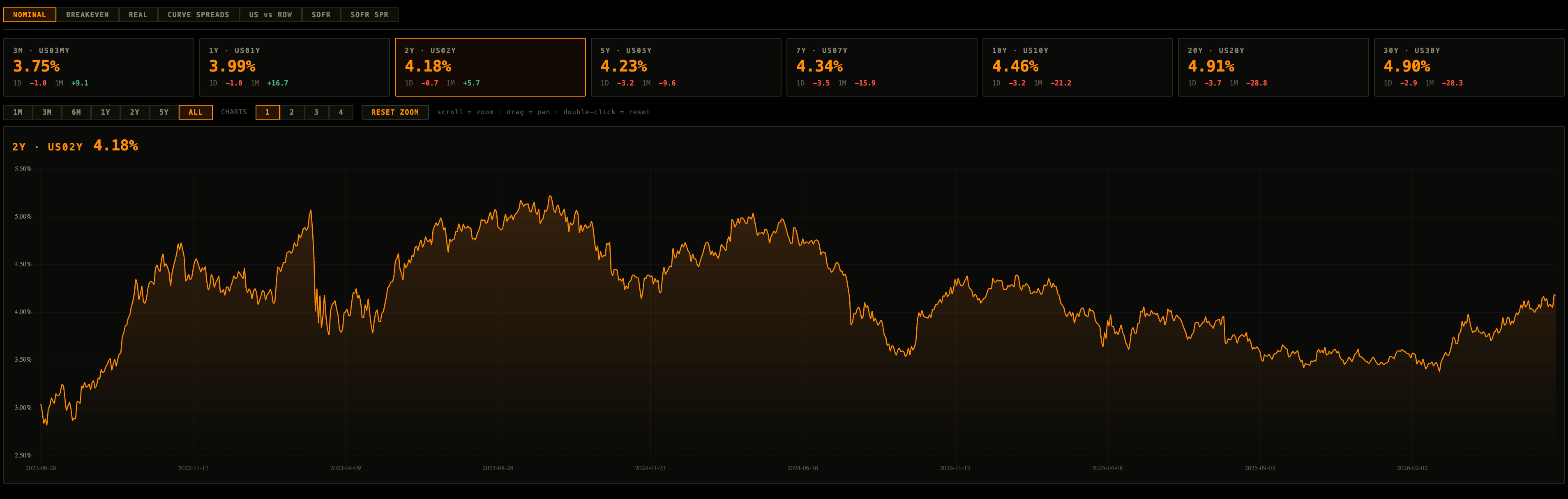

Short-end:

Long-end:

2s10s curve spread:

DXY:

My view on why there hasn’t been a drag on equities is that:

1. Nominal growth running hot enough to overwhelm the discount rate effect

If the driver of higher rates is a genuine upside growth surprise (not just inflation or term premium), then earnings revisions can more than offset multiple compression. The numerator (EPS) grows faster than the denominator (discount rate) rises. This means that rates are up for good reasons. You see this in early-to-mid cycle reflationary phases where nominal GDP is accelerating.

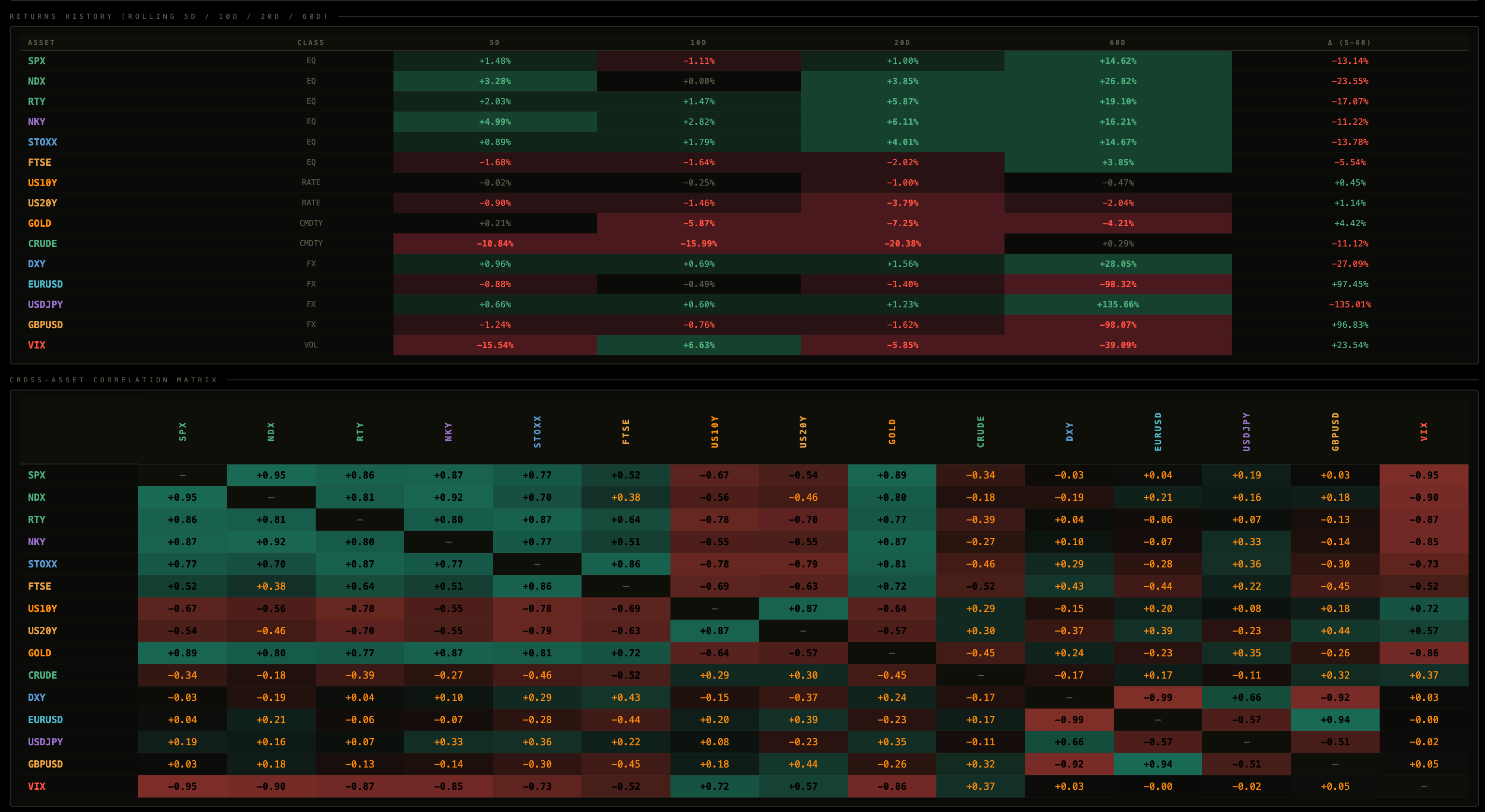

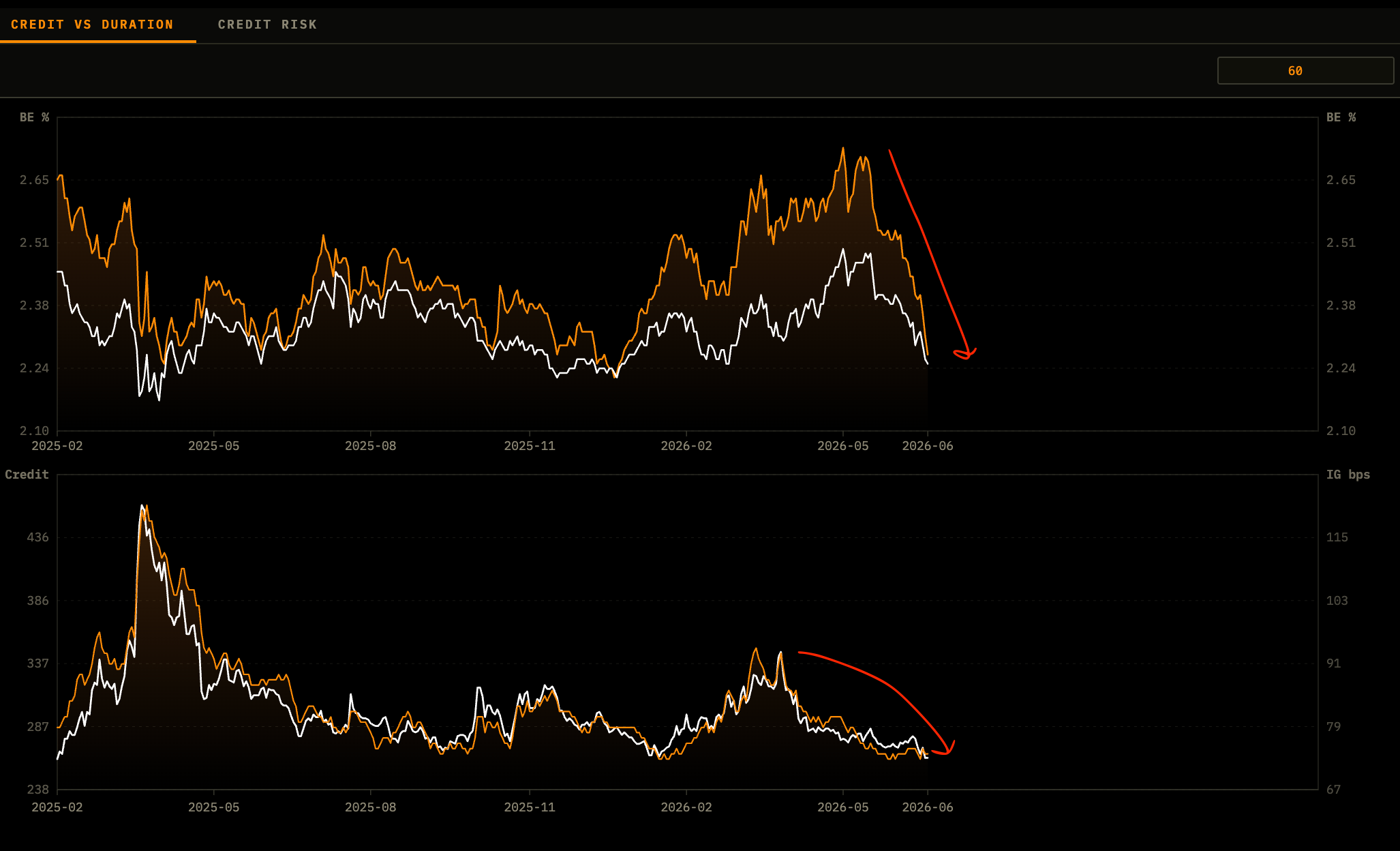

Breakevens down while credit spreads remain at cycles lows is proof that the driver of rates is growth.

2. USD strength driven by US exceptionalism rather than risk-off

There are two common drivers of dollar strength: risk-off (USD as safe haven, equities sold) and US outperformance (capital flowing into the US because the growth differential is widening in America’s favour). In the second case, the same force pulling the dollar up is also pulling capital into US equities. The drag on multinationals’ earnings translation is real but gets swamped by the inflow story. This is where we’re at right now in my view, real rates have directly driven the dollar higher (it hasn’t be some sort of risk-off bid).

3. Credit spreads not widening alongside

The equity drag from higher rates is amplified when credit spreads also widen (growth risk), because it signals financial stress and tightening credit conditions across the system. If long-end nominals are rising but IG/HY spreads are stable or compressing, it suggests the market is pricing a benign growth outcome rather than a liquidity crunch. This setup is where equities can shrug off the rate move (this is where we’re at, so credit spreads matter a lot here).

Nominal growth running hot enough to overwhelm the discount rate effect

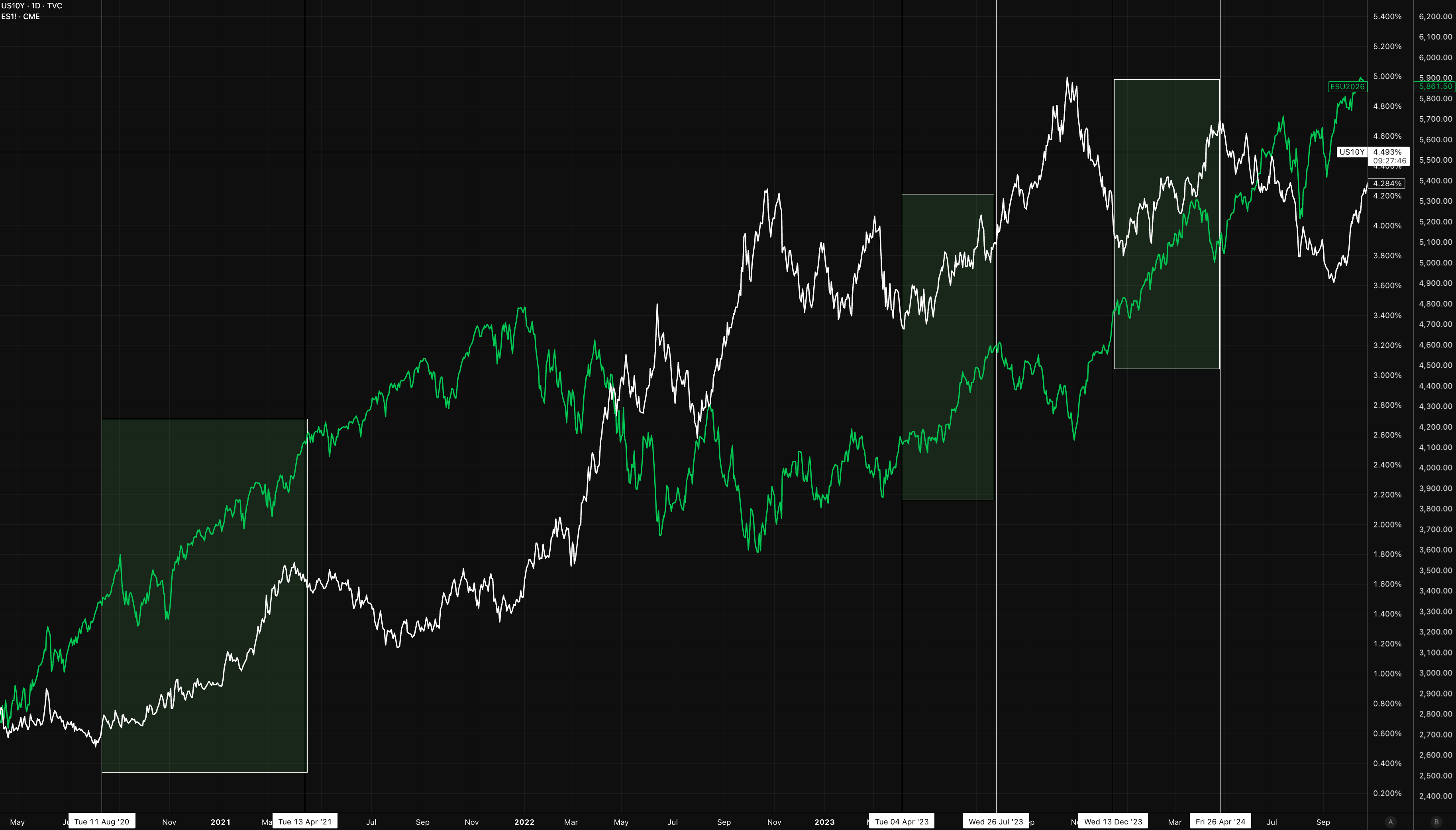

The standard DCF intuition says higher rates compress multiples, but that idea treats the numerator as fixed when it isn’t. When the driver of rising long-end yields is a genuine acceleration in nominal GDP, the earnings revision cycle kicks in hard and fast. Companies are pricing more product at higher prices, volumes are holding, and top-line beats start flowing through to operating leverage. The numerator is growing in real time, not sitting static while the discount rate climbs.

Given the whole AI capex spending and just how much AI is contirbuting to equity performance, it’d wise to focus on earnings from the largest companies in that sector whch are giving evidence of my point above.

Nvidia:

The key is the sequencing and the magnitude. If rates rise 50bps but the forward earnings estimate for the index gets revised up 8-10%, the multiple compression is more than absorbed. This is what the 2021 reflation trade looked like in its early phase before inflation became a supply-shock: cyclicals rerated higher even as the 10y moved because the growth read was dominant. The equity market is discounting a stream of future earnings, and if that stream is being revised upward in nominal terms, the present value can still rise even with a higher discount rate.

There’s many times where this has been the case in recent history:

The regime breaks down when the inflation component of the nominal growth is supply-driven rather than demand-driven (we only see this on the margin recently, it’s already been priced out), because then you get margin compression alongside the rate rise: input costs go up faster than pricing power allows revenues to expand. The softer version of this story requires demand-pull inflation, strong labour markets, and positive operating leverage across the index. When all three are present, the growth overpowers the discount rate effect and equities decouple from the bearish rate narrative.

USD strength driven by US exceptionalism rather than risk-off

Dollar strength has two very different macro signatures and conflating them is one of the most common errors in cross-asset analysis. The risk-off dollar, which you see in acute stress episodes, comes with falling equities, widening spreads, and collapsing commodity prices: capital is fleeing to safety and the dollar is just the destination. The exceptionalism dollar is structurally different: it is driven by a widening growth and rate differential between the US and the rest of the world, and it comes with capital actively seeking US assets, not fleeing everything.

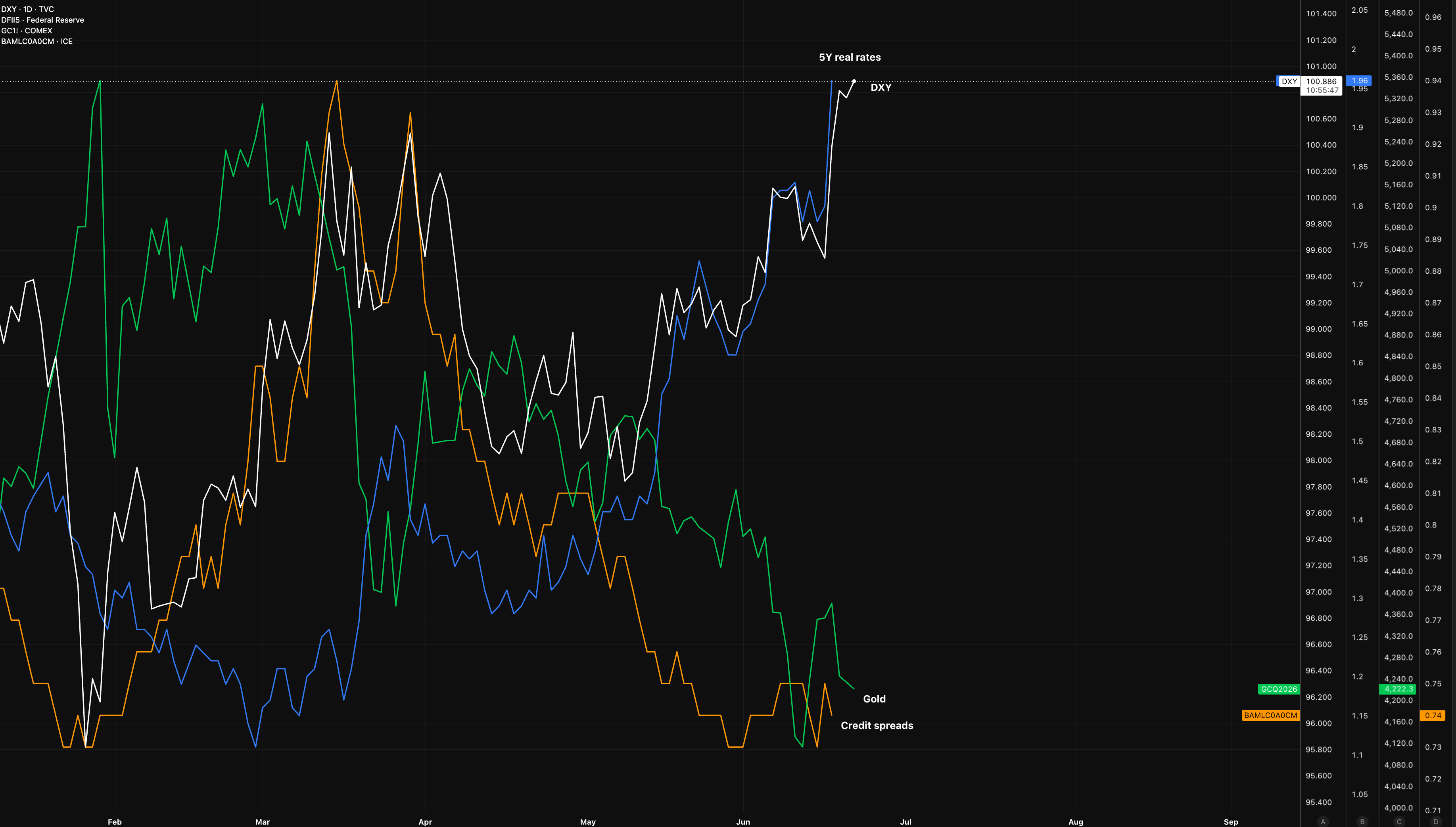

It’s clear that the dollar rally has been a function of higher real rates rather than any type of safe haven bid (where we’d see gold trading higher) or growth scare (where we’d see creidt spreads widening).

The Fed’s stance on inflation (which helps price the forward curve to some degree of accuracy) is the input that is directly giving real rates fuel.

In the exceptionalism regime, the same fundamental that is pulling the dollar up, faster US growth, better corporate earnings, tighter labour markets, is also the fundamental pulling capital into US equities. Foreign investors reweighting toward US assets are simultaneously buying dollars and buying S&P futures. The multinational earnings translation headwind is real and will show up in reported EPS for companies with large foreign revenue bases, but the index-level flow dynamic can more than offset it, particularly for domestically-oriented sectors and companies.

The diagnostic here is to watch what else is moving with the dollar. If USD is rallying and EM equities are getting crushed while credit spreads widen, that is a risk-off move and the equity drag will follow. If USD is rallying while European and Japanese equities are flat-to-down in dollar terms but US equities are making new highs on strong economic data, that is the exceptionalism idea I spoke about above. The capital flow story is the tell: are people buying the US, or are they selling everything else?

I’m watching cross-asset returns closely here, if we start to see credit spreads widen as gold bids, equities pull back, USD trades higher and the long-end remain at these levels, I would not want to be adding risk-on exposure.

Credit spreads not widening alongside

The credit market is the equity market’s leading indicator for financial stress, and the most important cross-asset signal when trying to judge whether higher rates will drag on equities is what IG and HY spreads are doing concurrently. When the 10y is selling off but credit spreads are stable or tightening, the bond market is essentially saying that this is a growth and inflation story rather than a default and liquidity story. Companies can still access capital, refinancing risk is manageable, and the fundamental earnings backdrop is intact. That is an environment where equities can absorb the rate move (which is exactly what’s happening).

Inflation expectations are falling and credit spreads are getting tighter, which mitigates some effects of higher nominals and a stronger dollar because lower inflation (to a degree) and low growth risk (tight credit spreads) are a net-positive for equities.

As I mentioned at the start, inflation expectations dropping as credit spreads remain at cycle lows is the easiest way for me to attribute that the rising long-end is tied to higher nominal GDP vs any type of term premium.

The idea is straightforward: if spreads are tightening while rates are rising, the all-in cost of debt for corporate borrowers is rising less than the Treasury move would suggest, or may not be rising at all. Financial conditions are tightening at the margin but not in a way that chokes off credit availability or triggers forced deleveraging. The credit channel, which is the most direct transmission from higher rates to economic damage, is not under stress. Equity risk premia can stay compressed and multiples can hold because the fundamental risk of recession and earnings downside is not being priced in the credit market.

The breakdown scenario, which is the one that really damages equities, is when rates rise and spreads widen at the same time. That combination signals that the rate move is happening in a context of deteriorating credit quality, tighter financial conditions, and rising systemic stress, rather than a strong growth backdrop.

Spreads widening 100bps while the 10y rises 50bps is far more destructive to equities than either move in isolation because it hits from both the discount rate side and the fundamental outlook side at the same time. Watching the credit market alongside the rates move is the single most important cross-asset check on whether the equity drag story will play out.

Thanks

Alfie

Nice one! To be honest i was expecting equities to re-price lower.

thnk you sir