Economic Outlook and Asset Allocation: A Comprehensive Analysis

Executive Summary: This report delves into the economic landscapes of the United States, European Union, and the United Kingdom, offering insightful guidance for investors. By examining key economic indicators and sectoral trends, we aim to equip investors with strategic recommendations to navigate the complexities of the global economy.

United States: A Robust Economic Performance

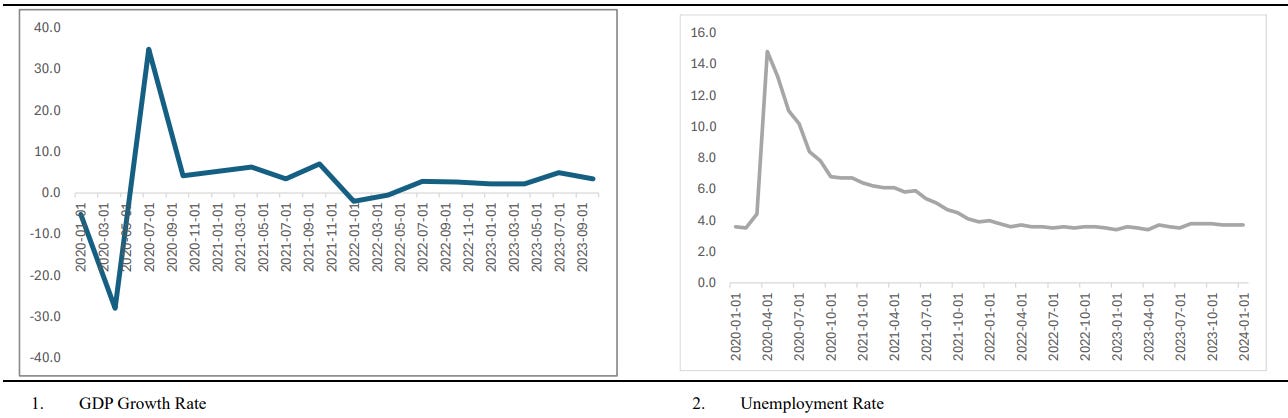

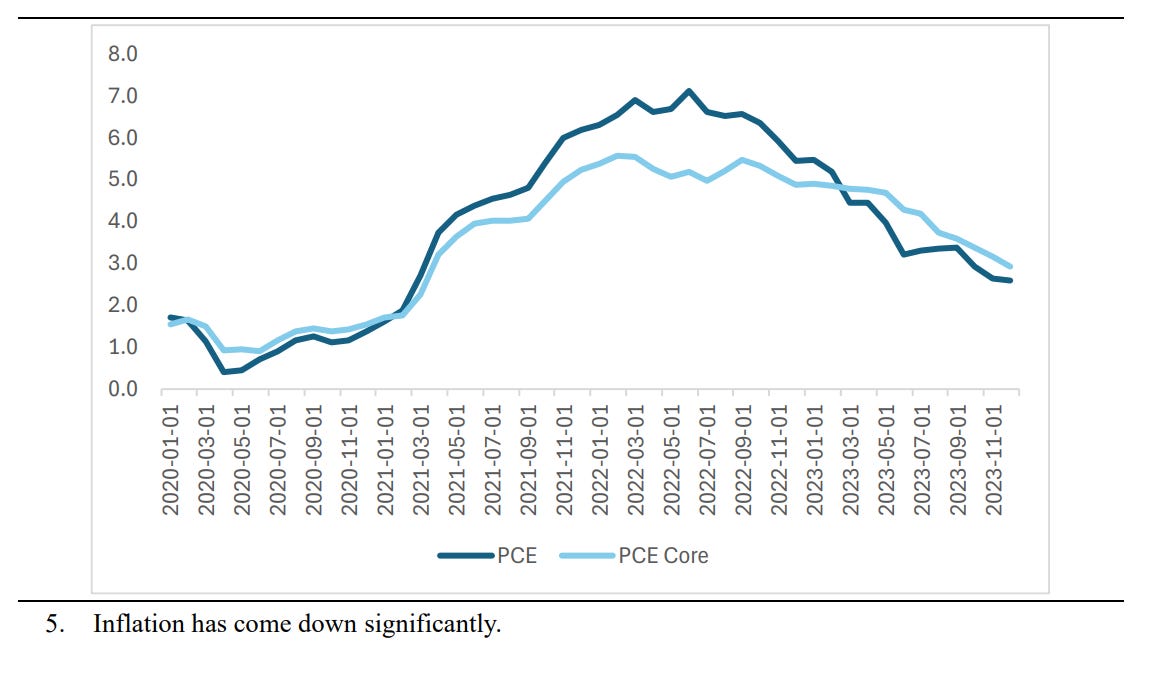

The recent robust performance of the US economy serves as a compelling narrative of resilience, characterised by the interplay between enduring structural tailwinds and transient cyclical headwinds. Key structural dynamics, including the resurgence of onshoring practices, a vibrant recovery in the labour market post-pandemic, and a sustained increase in government expenditure, have effectively counterbalanced the cyclical challenges posed by elevated interest rates. This delicate balance underscores the economy’s current strength, where growth remains vigorous and inflationary pressures are diminishing, aligning with the Federal Reserve’s goals.

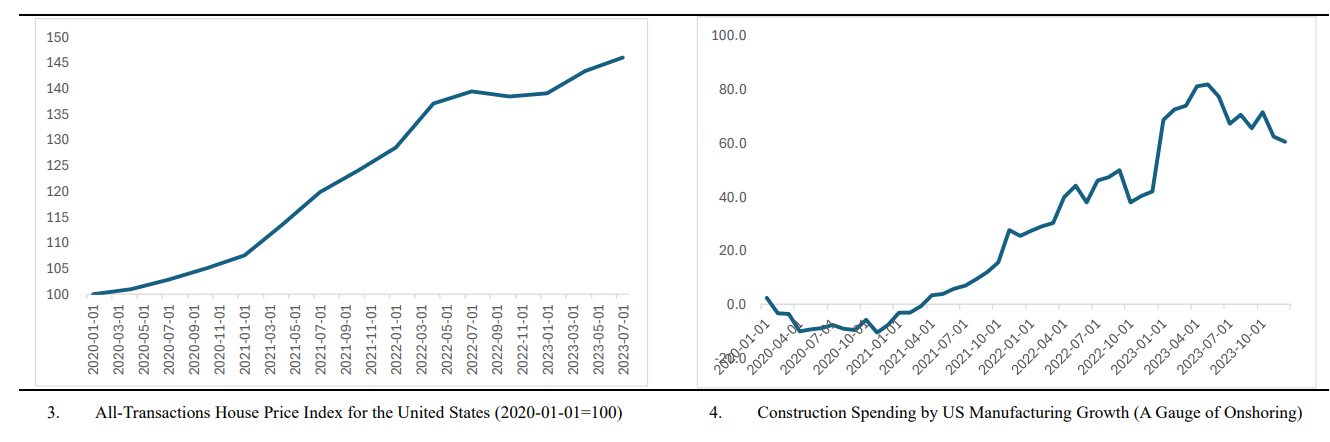

The housing market and manufacturing sector, particularly through onshoring, have emerged as vital engines of economic growth, demonstrating remarkable resilience.

This robust economic backdrop has led to a significant shift in market perceptions, with investors increasingly recognising the Federal Reserve’s commitment to maintaining higher interest rates until inflation is firmly under control. Despite rapid adjustments in market pricing to this newfound realisation, there remains a discrepancy, suggesting that further realignment may ensue as additional data becomes available.

In addition, the commercial real estate sector warrants particular attention, having experienced a paradigm shift due to the pandemic-induced remote work trend. Despite the gradual return to normalcy, a persistent preference for working from home has led to reduced demand for office spaces. This shift poses potential challenges for regional banks heavily invested in commercial real estate, although fears of a systemic crisis akin to the Global Financial Crisis appear unfounded.

Furthermore, the US is witnessing a notable change in the correlation between stocks and bonds, which, after years of positive correlation, is showing signs of reverting to a negative correlation. This trend suggests a decreasing sensitivity of the stock market to interest rate movements. For investors, this implies a more nuanced approach to interpreting strong economic data, rather than how it may impact the Fed’s reaction function.

Investment Implications

Favor long positions in US equities, particularly technology sectors, with caution towards AI advancements. Short Treasury bonds and monitor global risk dynamics, including DXY surges and stock-bond correlation reversals.

Europe: Navigating Economic Headwinds

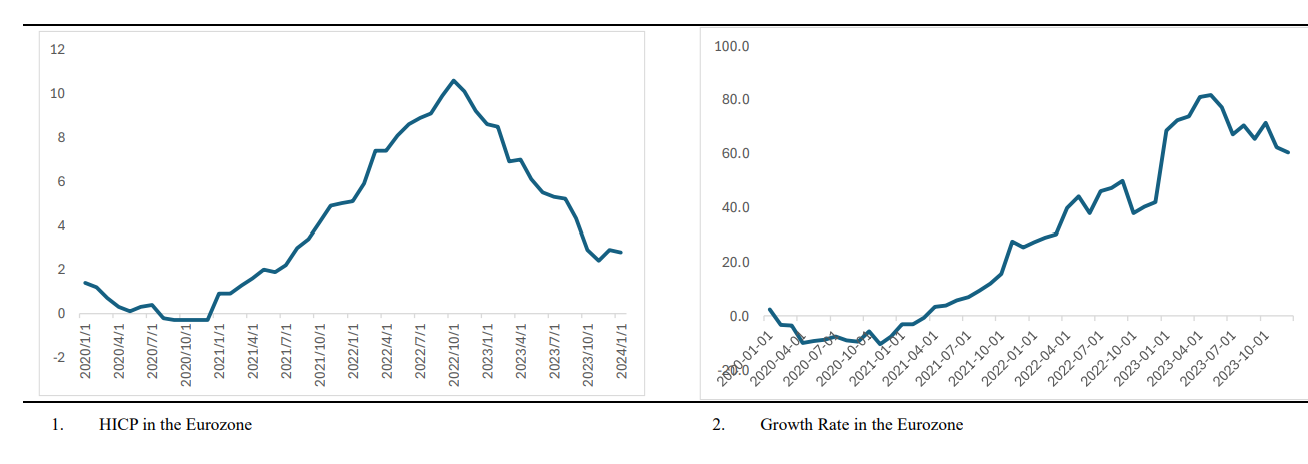

The Eurozone faces economic deceleration, influenced by the ripple effects of rate hikes. Despite a surge in inflation, largely attributed to base effects, inflationary pressures are showing signs of abatement. The economic landscape presents a nuanced picture, with countries like Germany encountering setbacks in constitutional ruling resulting in a loss of government funding, which could dampen economic vigour.

Delving deeper into the economic fabric of Europe reveals a complex and varied landscape across different sectors. Germany’s economy, for instance, experienced a significant setback with a €60 billion shortfall in potential investments in green technology, attributed to a constitutional court decision. This is a stark example of the unique challenges faced by individual European countries. In contrast to the robust and balanced growth observed in the US, the European Union grapples with the prospect of limited growth.

The disparity in growth potential within the EU itself is striking. Countries such as France, Germany, and Italy are particularly vulnerable to energy crises, contrasting with the relatively lesser impact on Greece and Spain. These internal variances are poised to play a critical role in shaping the economic future of the bloc. The overarching threat of weakened global industrial demand, exacerbated by the strength of the US dollar, introduces further complexity. Germany, with its heavy reliance on industrial exports and imported energy, may find itself at a disadvantage. Conversely, nations with economies more focused on the service sector, like Greece and Spain, could potentially benefit as global travel and commerce resume.

The European Central Bank maintains its interest rates at 4.75%, a decision that appears to align with the prevailing market consensus. Although this stance may initially act as a drag on economic momentum, its comprehensive impact remains to be fully realised. In anticipation of potential economic downturns—events that would not catch central bankers off guard—investors are encouraged to prioritise strategic safeguards in their portfolios.

Navigating the investment landscape of this region, a critical risk factor emerges from the geopolitical sphere: the possibility of escalating tensions in the Middle East and the Red Sea, which could significantly elevate energy costs. Such developments underscore the importance of vigilance and adaptability in investment strategies.

Investment Implications

The current environment suggests a cautious stance towards stocks, favouring a shift towards bonds. Investors are advised to focus on defensive stocks and sectors known for their ability to generate consistent cash flows, such as utilities, consumer staples, and pharmaceuticals. The pronounced growth disparity between the United States and the European Union suggests that the EURUSD exchange rate may face downward pressure. Additionally, the growth variances within the Eurozone itself present unique opportunities, particularly in the bond markets. Specifically, investors might find value in favouring Spanish and Greek government bonds over German Bunds, leveraging the differential in economic momentum across these jurisdictions.

UK: Stay Cautious

The economic outlook has presented considerable challenges, with the data from 2023 illustrating a discernible downtrend. This weakening trajectory is projected to persist into 2024, further aggravated by a notable uptick in interest rates. Such monetary policy adjustments are expected to permeate the broader economy more thoroughly, potentially suppressing growth to a greater extent. Yet, amidst these challenges, there emerges a glimmer of optimism: the potential for real wages to experience an uplift, spurred by declining inflation rates. This development could offer some relief to consumers, yet the overarching success of this scenario hinges critically on the labour market's robustness.

A growing concern is the potential for labour market contraction, triggered as higher interest rates start to undermine corporate profit margins. This apprehension has been somewhat validated by the recent uptick in unemployment rates, climbing from 3.7% in January to 4.3%. Reflecting these conditions, the consensus among economists suggests a modest GDP growth forecast of 0.4% for 2024, echoing the growth rate observed in the preceding year.

Investment Implication

In light of the UK's economic scenario, adopting a defensive investment stance appears prudent. Sectors such as consumer staples, utilities, and pharmaceuticals are likely to offer relative stability, benefiting from consistent demand regardless of broader economic fluctuations. These sectors typically provide defensive equity investments that can perform better during times of economic uncertainty or market volatility.

Given the persistence of inflationary pressures, a cautious approach towards UK bonds is advisable. The inflationary environment diminishes the real return on fixed-income investments, making them less attractive in the current context. Additionally, the currency pair EURGBP may face added pressure, not solely from parallel growth trajectories between the UK and the Eurozone but also due to the disparities in inflation rates. This dynamic suggests a potential weakening of the pound against the euro, influenced by differing monetary policy responses and economic recoveries post-pandemic.